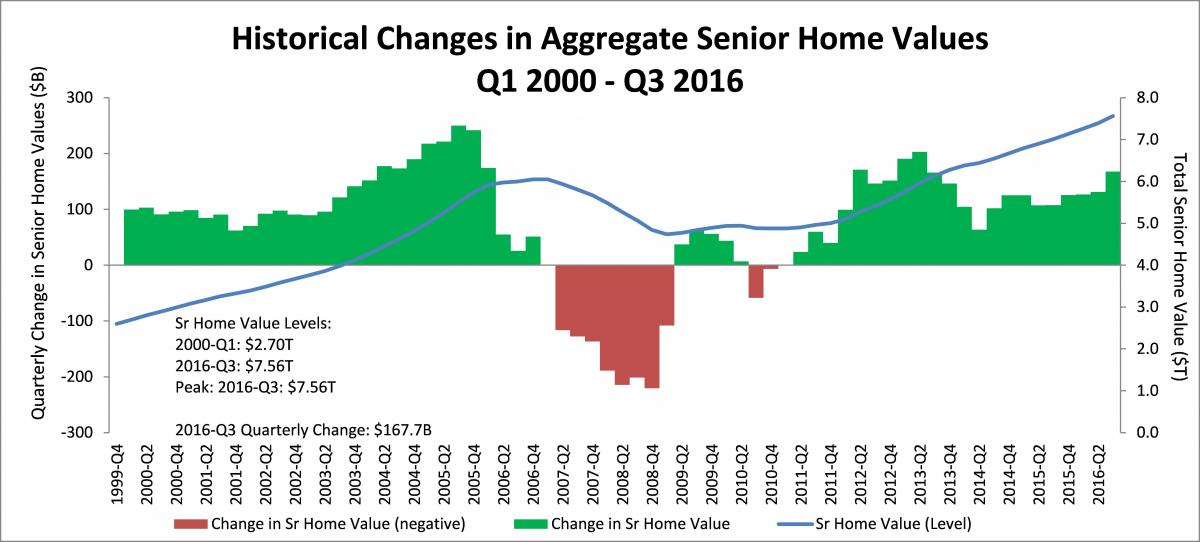

The National Reverse Mortgage Lenders Association (NRMLA) has reported that homeowners aged 62 and older saw an overall 2.6 percent increase of $152 billion in senior home equity in the third quarter of the year, bringing the total to $6.1 trillion. The gains, largely driven by a 2.3 percent increase in senior home values, pushed the NRMLA/RiskSpan Reverse Mortgage Market Index (RMMI) up to 217.34, another all-time high since the quarterly index was first published in 2000.

“The upward trajectory of the RMMI tells us that housing wealth continues to provide senior homeowners with a financial resource they can use to support their needs during their retirement years when income is dependent on Social Security, investment assets, and pensions,” said NRMLA President and CEO Peter Bell. “The positive trend is also reassuring for homeowners nearing retirement age who are less likely than their predecessors to leave the workplace with a defined benefit plan and also more likely to have long-term debt.”

According to a recent report from Harvard’s Joint Center for Housing Studies, only 29 percent of households on the cusp of retirement (aged 50-64) will leave the workforce with a traditional pension, compared to 49 percent of today’s 65-and-older households. The authors also cite a study from the George Washington University School of Business showing 60 percent of pre-retirees (aged 51-61) have at least one source of long-term debt, and 26 percent have more than one source.

The combination of constraints raises serious concerns about the financial stability of future retirees and their ability to manage the costs of aging including long-term care. Among their policy recommendations for addressing the projected challenges, the authors of the JCHS report note that housing wealth can provide a valuable safety net for older households in need of additional financial resources.