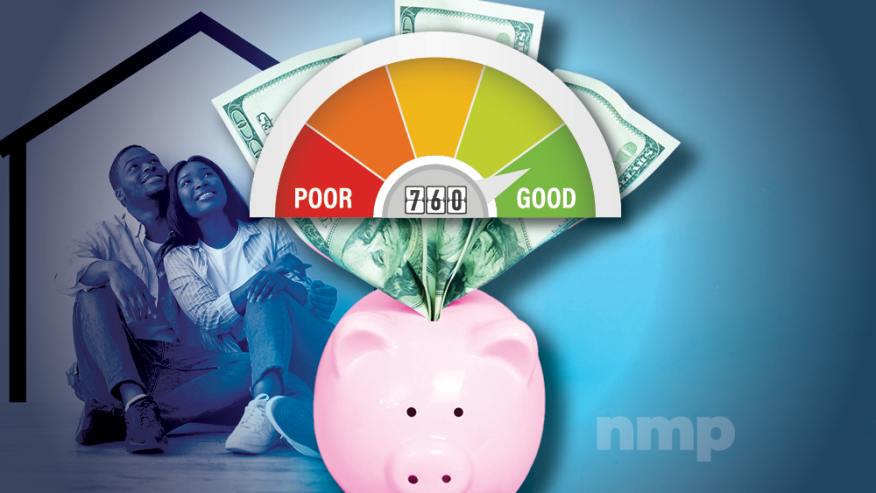

A new nationwide analysis from AD Mortgage shows that homebuyers who raise their FICO credit scores to 760 — a level often tied to the most competitive mortgage rates — can save tens of thousands of dollars in interest over the life of a 30-year loan, with savings varying widely by state.

The study, Credit Score vs. Mortgage Cost: How Long It Takes to Improve and How Much It Can Save, State by State, models the impact of raising credit scores on mortgage costs and regional affordability.

In California, borrowers who reach a 760 score could save approximately $42,753 in mortgage interest compared with average-score borrowers in the state, driven by higher home prices and the pronounced premium for top-tier credit. By contrast, in Texas, while improving to a 760 score can still yield significant savings — roughly $26,881 — the analysis also highlights one of the steepest proportional rate penalties for sub-760 scores, costing borrowers more than 10.7% of the total loan amount in additional interest.

“This new data underscores just how critical credit education and early financial preparation are for today’s homebuyers,” said Max Slyusarchuk, CEO of AD Mortgage. “A difference of 20 or 30 FICO points may seem small, but over the life of a mortgage, it can determine whether a borrower pays an extra $20,000 in unnecessary interest. Our goal with this report is to give lenders, brokers, and consumers actionable insight into how credit impacts true buying power.”

A Regional Overview

Across the country, the total lifetime interest savings from achieving a 760 score ranged from about $10,000 to $46,000, with the highest absolute dollar figures found in high-cost states such as Hawaii, California, and Massachusetts. States with lower median home values saw more modest savings totals, though even smaller amounts can materially affect long-term affordability.

Most U.S. borrowers would need 1.5 to 3 years to raise their credit scores to 760 — the benchmark for prime mortgage rates — assuming steady 20-point annual gains. Mississippi and Louisiana face the longest timelines at 3.5 to 4 years, while Minnesota is fastest at under one year.