The next generation of LOs strive to ‘reset the tone’ of the industry

By Katie Jensen, Associate Editor, National Mortgage Professional

Building Trust With Borrowers:

Streetfighter vs. Digital Dreammaker

The next generation of LOs strive to ‘reset the tone’ of the industry

By Katie Jensen, Associate Editor, National Mortgage Professional

It’s a Thursday afternoon in New Orleans, and Jonathan Fry is suited up like he’s running for mayor. He’s not — he’s out to sell mortgages. In his local market, where handshakes still matter and happy hours double as networking events, Fry’s reputation precedes him.

At 22 years old, the My Community Mortgage loan officer has a simple philosophy: “If all these older folks are bitching and complaining about why the real estate market’s tough,” he says, “I’m going to reset the tone.”

He did it by going everywhere — rooftop mixers, open houses, lunch-and-learns — in a full suit and tie, making himself omnipresent and unmistakably professional. “For one entire year, I wore a suit and tie to every event. My business skyrocketed.”

Meanwhile, 500 miles away and in 35 states at once, Daryl Lionnet, vice president of West Capital Lending, sits in front of a CRM, headset on, running a very different game. He’s built a national pipeline with digital ads, call center efficiency, and finely tuned scripts. His leads come cold and fast. His follow-up is relentless.

“We’re basically doing what the big direct-to-consumer shops are doing,” Lionnet explains, “but with less layers and more hustle.”

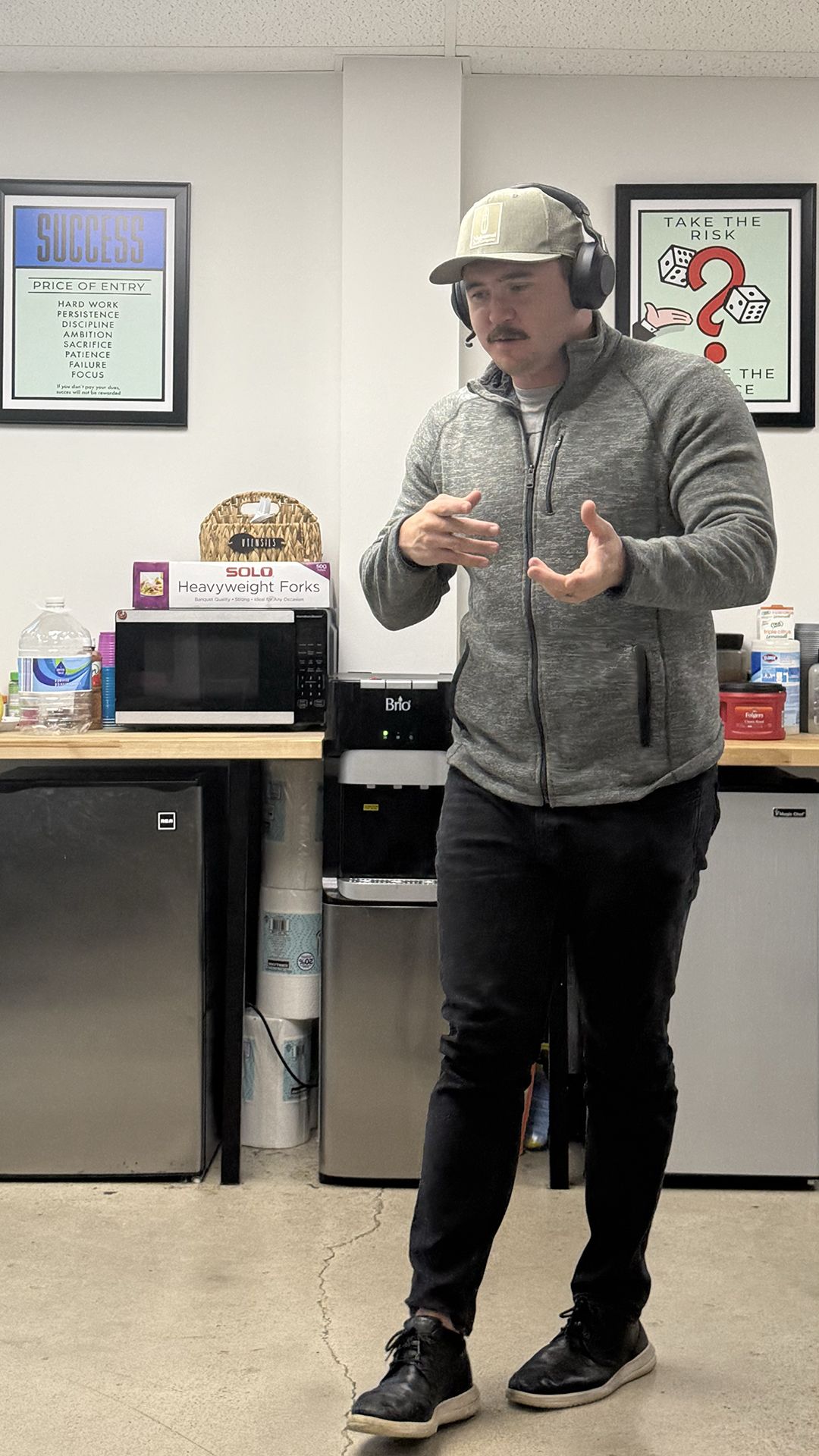

A group of loan officers participate in a training session at West Capital Lending, where Daryl Lionnet (standing, left) leads a discussion on digital lead conversion and CRM strategy — the same systems that power his high-volume, multi-state pipeline.

A group of loan officers participate in a training session at West Capital Lending, where Daryl Lionnet (standing, left) leads a discussion on digital lead conversion and CRM strategy — the same systems that power his high-volume, multi-state pipeline.

Fry and Lionnet represent the two dominant avatars of the modern mortgage originator: one built on boots and suits, the other on systems and scale. Yet, both have managed to close about 100 loans annually, proving there’s more than one way to build a thriving business in today’s market.

Moreover, they’re resetting the tone of an industry that’s been defined by burnout, ego, and old-school hierarchies, moving it towards a model that rewards authenticity, accountability, and modern hustle. One does it through face-to-face connection; the other, through digital precision. Together, they signal what the next generation of loan officers looks like: confident, adaptive, and unapologetically self-made.

“Month one, I wrote a $30,000 check for leads. That’s what it took. And I believed in it.”

> Daryl Lionnet, Vice President, West Capital Lending

The Generational Divide

They’ve seen rate cycles come and go. They’ve weathered Dodd-Frank and danced through refinance booms. But once the average age of loan originators began to push 50, the industry’s most trusted faces became its most seasoned.

According to MGIC’s October 2024 Loan Originators Survey, nearly two-thirds of loan officers (64%) were aged 50 or older with at least two decades of experience under their belt. The share of age 50+ originators ticked down from 66% in 2023. However, that’s likely due to older originators leaving the industry rather than younger originators entering, since the 2024 NMLS Mortgage Call Report shows how the overall MLO workforce has been shrinking every year since 2022.

More recently, the 2025 Top Producers Survey from National Mortgage News found that nearly 80% of respondents were over age 40, while only 18% were between the ages 31 and 40, and only 2% were under the age of 30.

At the same time, homebuyer and seller demographics are gradually shifting towards younger generations. The National Association of Realtors 2025 Homebuyers and Sellers Generational Trends report shows that millennials between ages 26 and 44 make up the largest share of homebuyers, followed by younger baby boomers (ages 60 to 69) and Gen Xers (ages 49 to 59).

“One of my biggest referral sources is my title reps. Their whole job is to market to Realtors. Why wouldn’t I want to be their best friend?”

> Jonathan Fry, Loan Officer, My Community Mortgage

Jonathan Fry (right) attends a professional networking event with his peers— dressed in his typical uniform, a suit and tie. Fry credits his style and years of showing up at gatherings like these for helping him become a recognizable and trusted presence in the New Orleans market.

Jonathan Fry (right) attends a professional networking event with his peers— dressed in his typical uniform, a suit and tie. Fry credits his style and years of showing up at gatherings like these for helping him become a recognizable and trusted presence in the New Orleans market.

The data indicates a stark generational gap in an industry grappling with both talent attrition and changing borrower demographics. As more seasoned professionals near retirement, questions remain about how effectively the next generation of originators will be recruited and trained — especially in a business long dependent on mentorship, relationship-building, and deep institutional knowledge.

New Kid On The Block

Fry’s path started not with a CRM or national lead platform, but with a T-shirt his aunt made with a Cricut machine. “I was 21, wearing three gold chains, slacks that didn’t make sense, and teaching a lunch-and-learn,’” he laughs. “But I got business.”

It wasn’t long before mentors — like industry veteran Jordan Gerard — told him he needed to dress the part. “You’re 22 years old. You’ve got to act more professional. People need to believe you’re the guy who can handle their half-million-dollar loan.”

Fry took it seriously. He made a New Year’s resolution: every event, every outing — suit and tie. After That one simple change he says his business finally started to take off..

What also took off was his visibility. “I went to every event I could find for three or four years,” he says. “My entire goal was to be omnipresent.”

It worked. Nearly 100% of his business now comes from Realtor referrals. He immediately loops agents into group chats with clients after the first call, reinforcing the idea that they’re all on the same team. His job, he says, is to prove to the Realtor “why I’m the person they need to trust.”

But it’s not just appearances. Fry closes loans by creating real relationships — with agents, with title reps, with insurance providers, and even with other loan officers. “One of my biggest referral sources is my title reps,” he says. “Their whole job is to market to Realtors. Why wouldn’t I want to be their best friend?”

The Digital Deal-Maker

Lionnet’s strategy is a world apart. Where Fry shakes hands, Lionnet builds funnels. His phone only rings when the CRM warms up the lead. His clients rarely know his face, but they do know his process — and it works.

“I can say with 100% confidence that nobody can work that lead like I can,” Lionnet says. “When I get a client on the phone, they’re ready to talk. We go straight into the application.”

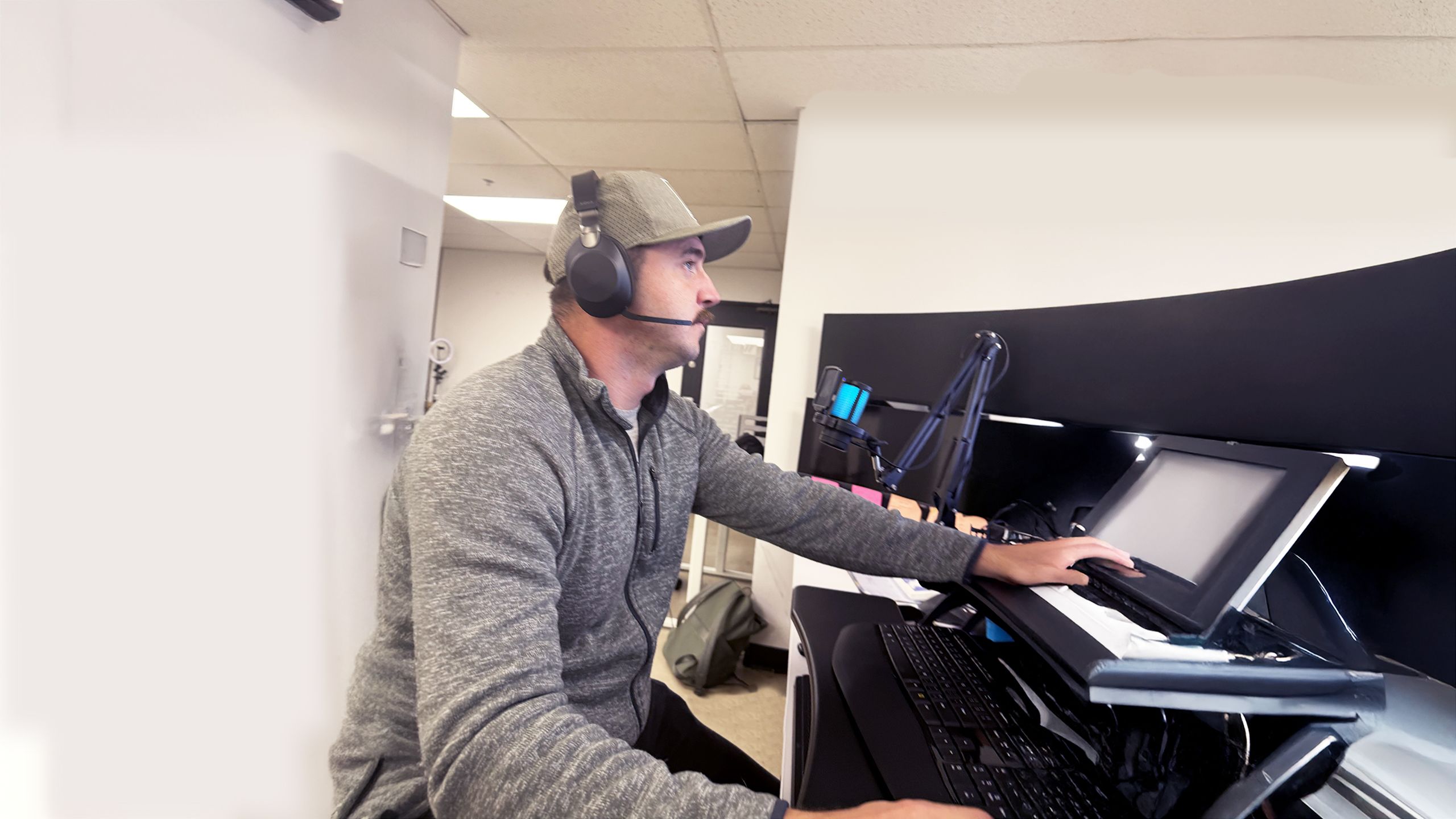

Lionnet pacing the office break room while speaking to one of his clients.

Lionnet pacing the office break room while speaking to one of his clients.

Lionnet’s team runs on automation, texting, and filtering leads before he ever picks up the phone. Every three to four calls, he’s submitting a 1003. It’s all high-efficiency, high-volume, and high-conviction.

From the jump, he bought in. “Month one, I wrote a $30,000 check for leads,” he says. “That’s what it took. And I believed in it.”

That belief came from mentors, from data, and from results. Lionnet now manages a team, tracks metrics obsessively, and closes deals nationwide. “I market in 35 states,” he says. “If I don’t know the market, I just make the extra phone calls. Call the title company. Ask the questions. You figure it out.”

Most of the work Lionnet does is about building trust with the borrower. “In the beginning and end of the deal, they need to love you,” he says “In the middle, your processor handles the grind. But you’ve got to sell the hell out of it on the way in — and show up again before the close.”

> Jonathan Fry

His secret weapons aren’t suits — they’re systems: CRMs, dashboards, Excel spreadsheets, and call scripts honed to the millisecond. He even charges clients for hard credit pulls — after he’s already built enough rapport to make it a no-brainer.

But even for Lionnet, it still comes down to connection. “In the beginning and end of the deal, they need to love you,” he says. “In the middle, your processor handles the grind. But you’ve got to sell the hell out of it on the way in — and show up again before the close.”

‘Reset The Tone’

Jonathan Fry’s rapid rise in the mortgage industry is fueled not just by his social savvy, but by his ability to tap into often-overlooked referral sources — especially title reps and insurance agents — to build a self-sustaining pipeline.

“I don’t know anything better than a hard market,” Fry said. “So I was like, alright, I’m going to go hustle, I’m going to grind.”

While many loan officers focus solely on chasing real estate agents, Fry recognized early on that title marketing reps are some of the most underutilized allies in the industry. “Their entire job is literally just to market to realtors,” he explained. “They don’t have to worry about closing deals. They’re just out there building relationships — the same relationships we need.” By forging genuine friendships with title reps, Fry expanded his reach into networks he wouldn’t have accessed on his own. One of his closest connections, a title rep named Carmen, not only referred business to him — she invited him to events, co-sponsored open houses, and even coordinated introductions with new agents.

“I can’t even explain how many people my title reps have introduced me to,” Fry said. “They’re meeting people that are outside of my sphere. They’re vouching for me when I’m not there.”

Jonathan Fry (second from left) meets with partners at a title company — the type of relationship he says has become one of his strongest and most overlooked referral sources.

Jonathan Fry (second from left) meets with partners at a title company — the type of relationship he says has become one of his strongest and most overlooked referral sources.

Fry applies the same mindset to insurance agents and even other loan officers, many of whom send him deals that fall outside their guidelines. These secondary channels became essential to his business model — especially in the early years, when building a realtor network from scratch felt like an uphill climb.

His other key strategy? Be everywhere, all the time. From hosting lunch-and-learns to attending every local industry event, Fry spent years saturating the New Orleans real estate scene. That visibility paid off — not just in recognition, but in trust. “People started realizing, ‘You’re everywhere,’” he said. “Well, I spent four years doing that nonstop.”

Perhaps his most creative strategy came from an unplanned brunch that snowballed into a movement. After one networking event, Fry and a group of industry peers went out for mimosas — and “The Brunch Munch” was born. What began as a social outing evolved into a 60-person monthly meetup that blended fun with professional connection. “We actually did a once-a-month event with the Brunch Munch,” Fry said. “And that group introduced me to so many new people. It wasn’t just marketing — it was building real relationships.”

By leaning into authenticity, leveraging overlooked partnerships, and staying relentlessly visible, Fry built a business that thrives on community. His advice to other originators is simple but powerful: don’t just chase the obvious leads — build a tribe of allies who will sell your name when you’re not in the room.

Rejecting Unnecessary Grind

Despite the fact that Lionnet conducts most of his business over the phone, he doesn’t consider himself a “call center LO” — at least not in the traditional sense. Nor would he describe West Capital Lending, the direct-to-consumer brokerage where he works, as anything like the high-pressure call center environment of his former employer, loanDepot.

The workplace environment at West Capital Lending is uniquely aligned with the expectations and values of the younger generation of MLOs. A 2025 Deloitte generational survey found that Gen Zers, who are projected to make up 74% of the global workforce by 2030, ranked mental health as one of their top societal concerns, second only to cost of living. Millennials reported similarly, placing mental health higher on their list of priorities than any previous generation.

In that context, Lionnet’s approach feels like a generational shift. Younger MLOs aren’t looking to grind through 400 calls a day for a 2% conversion rate and Lionnet’s model proves they don’t have to. By leveraging a CRM system and automated tools, he filters out unqualified leads and focuses his time and energy on high-value conversations that are more likely to convert.

“The CRM does a lot of that for me,” he said. “I’m not being told, ‘Bob, screw you,’ which happens a lot if you’ve ever worked in a call center.”

Previously, Nick Grobnagger, co-owner of Green Home Loans, shed some light on the call center environment during his nine years working for Quicken Loans, now known as Rocket Mortgage, where “Ninety-five percent of the time you’re either not going to get someone or, if you do get someone on the phone, they’re going to be upset,” he said.

Nick Grobnagger

Nick Grobnagger

Many call center originators refer to it as their “Boiler Room” experience, which might have been a great movie in the 1990s, but it’s not an experience that younger generations are looking to replicate.

While West Capital Lending may source leads from the same digital publishers that power Rocket Mortgage, the key difference is how those leads are handled. Lionnet’s leads are filtered and nurtured through a CRM before they ever reach his desk, creating a warmer pipeline and cutting down on wasted calls.

Instead of making his sales pitch to hundreds of people per day, some who aren’t even ready to pull the trigger, Lionnet devotes his time to productive conversations with borrowers who are already primed to talk. He further streamlines his workload by relying on his assistant and processor to handle most tasks once the loan is in motion.

“I sell them really well,” he said. “Because I want to make sure in the beginning they love me, and at the end they remember why they love me.”

He’s also taken steps to reduce overhead on the backend — including the rising cost of pulling credit. Lionnet used to absorb that expense himself, but as prices climbed to a total of $3,000 per month, he changed tactics. Now, he positions the credit pull as part of the borrower’s investment in the loan process.

“I’m coming in to save the day, change someone’s life by turning their bills from $6,000 to $3,000 on a mortgage,” he said. “So we run it … and we’ll say, ‘Hey, look, you don’t have anything to do annually,’ or ‘Hey, we've got a 50 percent chance there and have to run the approval. Gonna be 80 bucks. What’s the card you want to use?’ And I charge the line. But at that point they’re already invested.”

Two Models, One Message

Fry and Lionnet couldn’t operate more differently, but they agree on one thing: this business is about relationships, whether you build them on rooftops or RingCentral.

“There are a hundred ways to get rich in mortgages,” Fry says. “I want to know all of them.”

For the new generation of LOs, the lesson is clear: pick your playbook, play to your strengths, and don’t be afraid to pivot. Whether you’re wearing a suit to brunch or a headset to a Zoom call, the deal goes to the one who shows up ready.

ndustry’s biggest bottleneck is not underwriting itself — it is the uncertainty that reaches underwriting too late in the process. When validation happens upstream, speed follows naturally.

The long tail of loss mitigation is now coming into view as FHA’s post-pandemic relief tools give way to repeat defaults, exhausted options, and a swelling foreclosure pipeline

Katie Jensen

Connect with your local mortgage community.

Meet your your colleagues, both national and local, by attending an event in your area.