The cost and availability of homeowners insurance have worsened through the first half of 2024, according to data published by Matic, a digital insurtech platform, in its mid-year premium trends report. The report also underscores how two-thirds of homes are underinsured largely due to coverage amounts failing to keep pace with rising premiums.

These market disruptions stem in part from the frequency of catastrophic events in 2023, which included 28 billion-dollar U.S. weather disasters, a record. Coupled with a rising population in high-risk areas, these conditions have created volatility, with insurers struggling to cover costs. Structural solutions have been proposed, but would likely take years to approve and implement.

“The combination of climate change, regulatory challenges, and inflation has created a perfect storm, leaving many homeowners without the coverage they need,” said Ben Madick, CEO and co-founder of Matic. “American homes are increasingly underinsured, highlighting the need for the insurance industry and regulators to collaborate on solutions.”

Drawing from a dataset of 36 million quote requests, 10 million properties, and external quoting engines, the report highlights challenges faced by homeowners, mortgage entities, and the broader housing market due to premium increases, new business restrictions, and carrier exits.

The impact of insurance market volatility on the mortgage industry was also highlighted in Matic’s report, with 63% of lenders reporting that at least one borrower they had recently worked with experienced challenges securing home insurance. Those lenders cited issues such as debt-to-income ratios becoming too high once the cost of insurance was factored in and borrowers needing to lower the mortgage they could afford.

Only 16% of lenders indicated that they felt very knowledgeable about the insurance landscape.

“Changing market dynamics are not only affecting homeowners but also continue to put significant strain on the mortgage industry,” Madick added. “Mortgage entities should be aware of the latest trends, as rising premiums are increasingly determining if and when a loan is approved.”

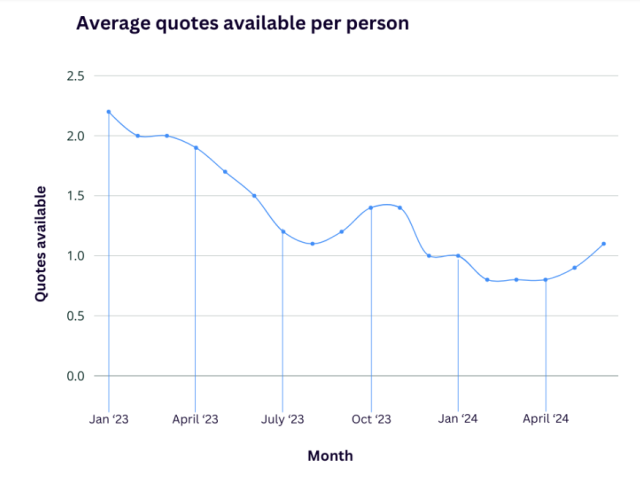

The average number of home insurance quotes available per person nationally fell by 27% from June 2023 to June 2024, Matic’s report shows, a consequence of continued new business restrictions, carrier withdrawals from high-risk markets, and regulatory challenges. Quote availability reached its lowest point in March 2024, before gradually improving in May and June.

For states where rate hikes have been approved, both new business and renewal policies have experienced records for premium increases year to date, Matic’s data shows.

Homeowners faced an average 17.4% premium increase for new policies in the first half of 2024, compared to 11.6% in 2023 and 5.9% in 2022. Homeowners who stayed with the same carrier and policy each year experienced even steeper increases, with those who purchased a policy in 2021 now paying 69% more in 2024.

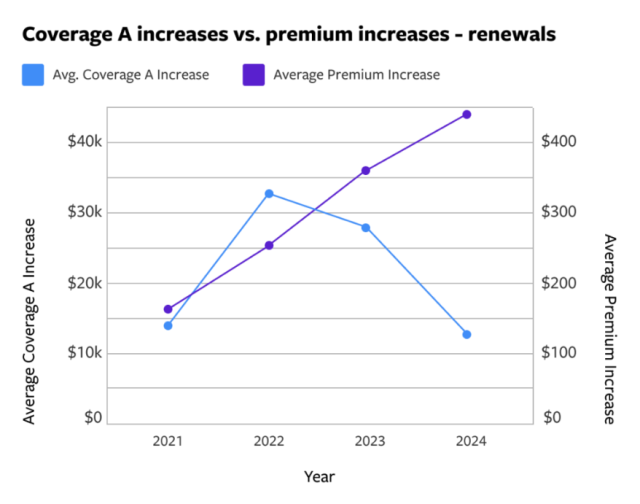

The two-thirds of underinsured U.S. homes Matic identified are covered by policies with coverage amounts failing to keep pace with rising premiums. Dwelling coverage experienced sharp increases from 2021 to 2022, which started slowing in 2023 and continued declining into 2024. New and renewed insurance policies are failing to reflect current reconstruction costs or home improvements.

For example, a homeowner who bought an insurance policy in 2021 saw their premium rise by $253 and dwelling coverage increase by $33,500 at their 2022 renewal. However, at their 2024 renewal, their premium had increased by $445, while their dwelling coverage only rose by $13,700. This leaves a delta the borrower must cover in the case of a catastrophic loss, putting mortgage servicers in a difficult position navigating loss mitigation with borrowers and lenders.

Roughly 6 million U.S. homeowners have no home insurance policy.

The report notes how the government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac have emphasized the importance of adhering to property coverage requirements for mortgages, signaling a shift towards stricter monitoring and enforcement. “Although some rules have been paused to address compliance challenges, there is a clear need for improved tracking systems to ensure homes and mortgage companies are sufficiently protected,” the report reads.

Despite ongoing challenges, the report notes signs of improvement. The projected combined ratios for the Property and Casualty (P&C) insurance industry are expected to improve, with estimates dropping to 98.5% for both 2024 and 2025, indicating a path toward profitability.

Additionally, construction costs have moderated, with lumber prices down by 18.9% since last year. Some carriers have begun to ease restrictions, with the average number of quotes available per person nationally increasing from 0.77 in March to 1.07 in June.