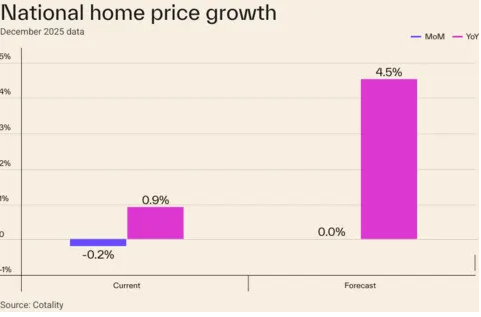

National home price inflation decelerated sharply at the end of 2025, with year‑over‑year gains slowing to approximately 0.9% in December — one of the softest annual increases observed since the post‑Great Recession housing rebound. This cooling marks a significant shift from the rapid appreciation seen during much of the last decade.

The latest Home Price Index data from Cotality shows that the housing market’s upward momentum has moderated considerably amid affordability pressures and wider supply.

Cotality Chief Economist Dr. Selma Hepp noted that the slowdown suggests the market is stabilizing and rebalancing toward more sustainable conditions.

"We are seeing a significant departure from the rapid surges of recent years; while the upward pressure on prices remains, the momentum has moderated enough to suggest that the market is finally becoming more navigable for prospective buyers," said Dr. Hepp.

Regional Disparities Remain Noteworthy

While national growth has weakened, markets in the Midwest and parts of the Northeast — including states like New Jersey, Illinois, Nebraska, and Connecticut — continue to post stronger year‑over‑year gains. Cities such as Newark, Allentown, and Chicago are examples where price increases have outpaced the national trend.

In contrast, several Southern and Western markets are witnessing price stagnation or declines, reflecting higher inventory levels and softer demand relative to past years. These dynamics underscore the uneven nature of the current housing landscape.

Economists tracking broader housing data see this shift as part of a larger narrative of normalization after extraordinary pandemic‑era price surges.

Although prices continue to rise modestly in many areas, the pace of growth is far below historical peaks, raising questions about affordability and buyer leverage as mortgage rates remain above long‑term norms.

Looking ahead, some forecasts suggest that modest gains may resume if economic conditions — including wage growth and borrowing costs — improve in 2026.