Cotality, a provider of property information and analytics, has released its Homeowner Equity Report (HER) for Q3 2025, revealing a mixed picture for U.S. homeowners.

Nationally, borrower equity declined by $373.8 billion, or 2.1%, bringing total net equity for mortgaged homes to $17.1 trillion — down from a peak of $17.7 trillion in Q2 2024.

Dr. Selma Hepp, Cotality’s chief economist, noted, “As home price growth moderates, negative equity is on the rise. Many first-time and lower-income buyers who used minimal down payments or piggyback loans are now facing the risk of negative equity.”

Recent homeowners lost an average of $13,400 in equity year over year, following gains of $25,000 in 2023 and $4,900 in 2024. Rising loan-to-value (LTV) ratios, particularly in the 85%-94% range, highlight the growing vulnerability of leveraged buyers.

Negative equity ticked up in Q3 to 2.2% of homeowners — roughly 1.2 million properties — a 21% increase from the prior year. The number of mortgaged homes in negative equity rose 6.7% from Q2, reflecting seasonal market cycles and softening home price gains.

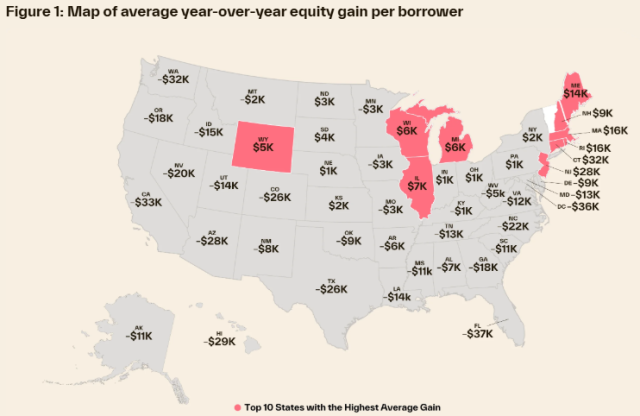

Regionally, the Northeast continues to see gains, led by:

- Connecticut ($31,500)

- New Jersey ($27,500)

- Rhode Island ($16,200)

Conversely, 32 states posted annual equity losses, led by three of the hardest hit states, including:

- Florida ($-37,400)

- District of Columbia ($-35,500)

- California ($-32,500)

At the metropolitan level, Las Vegas, Nevada; Los Angeles, California; and San Francisco, California remain relatively stable, while Austin, Texas; Baton Rouge, Louisiana; New Orleans, Louisiana; and Lafayette, Louisiana reported significant increases in negative equity due to price drops or natural disasters.

Looking ahead, the Cotality Home Price Index projects modest growth of just over 4% by October 2026. Dr. Hepp emphasized that the performance of highly leveraged loans will depend on broader economic and labor market conditions, making close monitoring critical.