Independent mortgage banks (IMBs) and mortgage subsidiaries of chartered banks saw a recovery in production profits during the third quarter of 2024.

According to the Mortgage Bankers Association’s (MBA) latest Quarterly Mortgage Bankers Performance Report, lenders achieved a pre-tax net profit of $701 on each loan they originated in the third quarter, an increase from $693 per loan in the previous quarter.

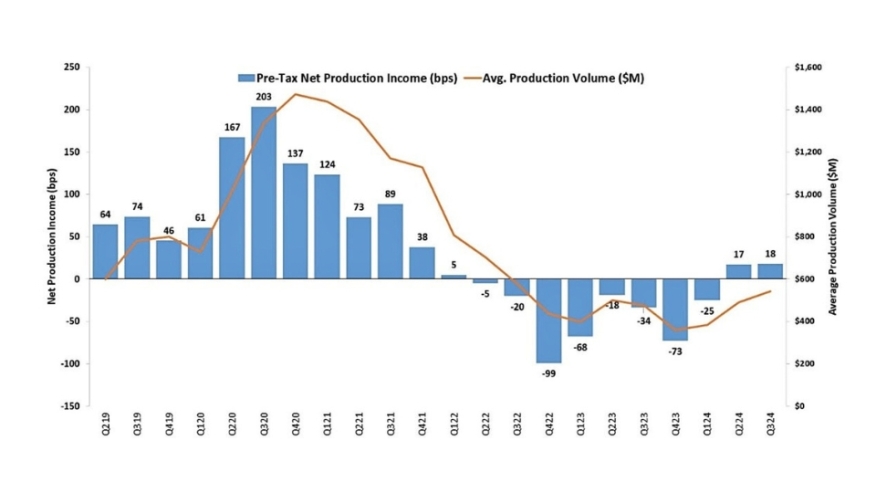

“Mortgage companies reported net production profits for the second consecutive quarter after an unprecedented period of net production losses that spanned two years,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “Net production profits increased to 18 basis points last quarter – far improved from the average loss of 43 basis points the past two years – with a drop in secondary marketing income offset by a decrease in production expenses.”

In the mortgage servicing sector, Walsh explained that higher prepayment expectations in the third quarter led to mortgage servicing right (MSR) impairments, impacting profitability. Net servicing financial income declined to a loss of $25 per loan serviced in the third quarter, down from a gain of $69 per loan in the second quarter.

“Overall, independent mortgage banks performed decently, with 71 percent reporting profitability across production and servicing, compared to 78 percent in the previous quarter,” Walsh added.

The average pre-tax production profit for the third quarter of 2024 was 18 basis points (bps), an increase from 17 bps in the second quarter of 2024 and an improvement from a loss of 34 basis points in the same quarter last year.

Average production volume per company rose to $542 million in the third quarter, up from $492 million in the previous quarter. By count, companies averaged 1,642 loans in the third quarter, up from 1,503 loans in the second quarter.

Total production revenue, which includes fee income, net secondary marketing income, and warehouse spread, dropped slightly to 341 bps in the third quarter, compared to 347 bps in the second quarter. Production revenue per loan decreased to $11,417 in the third quarter, down from $11,499 in the previous quarter.

Total loan production expenses — including commissions, compensation, occupancy, equipment, and corporate allocations — fell to 323 basis points in the third quarter of 2024, down from 330 basis points in the second quarter. On a per-loan basis, production costs decreased to $10,716 per loan, down from $10,806 in the second quarter.

From the third quarter of 2008 to last quarter, average loan production expenses have been $7,573 per loan.

The purchase share of total originations by dollar volume was 84%, while MBA estimates the purchase share for the broader mortgage industry stood at 75% in the third quarter. The average loan balance for first mortgages rose to $361,518 in the third quarter, up from $356,993 in the prior quarter.

Net financial income for servicing, excluding annualization, saw a decrease, reporting a loss of $25 per loan in the third quarter, down from $69 per loan in the second quarter. However, servicing operating income, which excludes MSR amortization and valuation changes, increased to $93 per loan in the third quarter from $88 per loan in the second quarter.

Across both production and servicing business lines, 71% of firms in the report achieved pre-tax net financial profits in the third quarter of 2024, a slight decline from 78% in the second quarter.