The U.S. housing market is beginning to show modest signs of life at the start of 2026, yet experts say the sector remains significantly below long-term norms, according to a new analysis by First American’s Deputy Chief Economist Odeta Kushi. While existing-home sales are edging higher, activity remains subdued when adjusted for demographic growth, underscoring persistent market constraints.

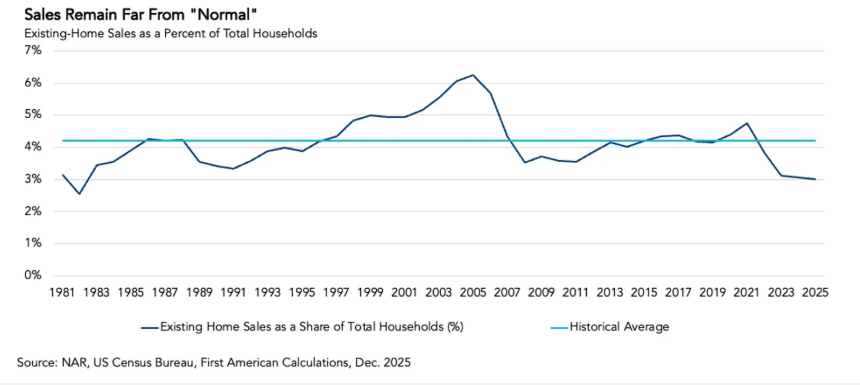

In December 2025, existing-home sales equated to just 3.3 percent of U.S. households, compared with a pre-pandemic average of 4.2 percent — a gap that would require more than one million additional sales annually to close. The discrepancy highlights how the market continues to lag, even with recent monthly increases.

“When existing-home sales are measured as a share of total households, the depth of the recent slowdown becomes clearer,” said Kushi. “In December 2025, the pace of existing-home sales was 3.3% of U.S. households, or roughly three sales per 100 households. While that is the highest pace since early 2024, it’s well below the pre-pandemic average of 4.2%. If existing-home sales were tracking that long-run average today, the seasonally adjusted annual pace would be approximately 5.6 million annualized sales. Instead, annualized sales are 4.4 million, a 1.25 million gap in existing-home sales that helps explain why the market still feels constrained, even as monthly data show improvement.”

First American cautions that raw sales counts can be misleading without considering the growth in total households. Over the past 15 years, the number of U.S. households has increased by roughly 15%, meaning similar sales volumes reflect weaker relative activity today than in prior periods.

Persistent low turnover can be attributed to a mix of factors. Many existing homeowners are reluctant to sell due to being “rate-locked” into lower mortgage rates from earlier years, while first-time buyers continue to face affordability headwinds and economic uncertainty.

Despite these constraints, First American’s Existing-Home Sales Outlook projects that January sales will rise modestly, with a 0.7% month-over-month increase and a 7.1% year-over-year gain, supported by a resilient economy, easing rate-lock effects, looser credit conditions, and rising buying power.

Economists say a more durable recovery is likely to unfold slowly as life events — such as job changes, family formation, and relocations — may eventually outweigh financial inertia and bring more homes to the market.

“A more durable recovery in sales activity is likely to come gradually, as time and life events begin to outweigh financial inertia,” added Kushi. “Job changes, family transitions, downsizing, retirement, and relocation will continue to bring homes to market, even if mortgage rates remain elevated. Indeed, 47 million Americans are in their 30s, and many still rent, representing a large pool of potential first-time buyers that may trickle into the market as life stages slowly line up with housing needs.”