Americans are slowly but surely adapting to higher mortgage rates. But whether it’s the “new normal,” as Redfin suggests, is anybody’s guess.

Right now, the real estate brokerage firm found in new research, the share of home owners with rates above 6% is at an all-time high.

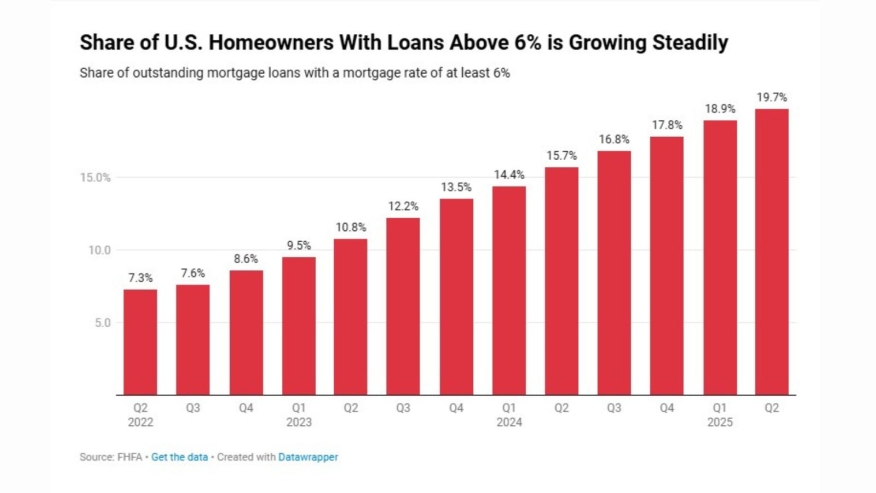

“With the weekly average mortgage rate fluctuating above 6% since September 2022,” the company says, the share of mortgages above 6% “is growing steadily—rising between 0.8 ppts and 1.4 ppts each quarter for the past two years.”

The total share now stands at 19.7%, or just about one in every five outstanding mortgages. Three years ago, it was just 7.3%.

Figures from the Federal Housing Finance Agency’s National Mortgage Database show that borrowers are slowly growing accustomed to elevated mortgage rates. At the same time, the share of sub-3% mortgages fell to 20.4% in the second quarter, down from a peak of 24.6% in the first quarter of 2021.

Chen Zhao, Redfin’s head of economics research, said the slight easing of the lock-in effect this year has been highlighted by an increase in inventory, with the number of homes for sale returning to pre-pandemic levels in many areas of the country.

“Life doesn’t stand still,” said Zhao. “People get new jobs, grow their families, downsize after retirement, or simply want to live in a different neighborhood. Those needs are starting to outweigh the financial benefit of clinging to a rock-bottom mortgage rate.”

The result: More houses are hitting the market than has been the case. Unfortunately, the increase in places for sale and recent dip in rates has yet to lead a major uptick in sales.

“Buyers need to see a bigger difference in their potential monthly payment before things are going to change,” commented Mariah O’Keefe, a Redfin agent in Seattle. “If rates tick down below 6%, that will bring a lot of people back into the market.”

Here’s the full breakdown of where today’s home owners fall on the mortgage-rate spectrum:

- Below 6%: 80.3%, down from a record 92.7% in the second quarter of 2022.

- Below 5%: 70.4%, down from a record 85.6% in Q12022.

- Below 4%: 52.5%, down from a record 65.1% in Q1 2022.

- Below 3%: 20.4%, down from a record 24.6% in Q1 2022.

And here’s another way to look at the data:

- Greater than or equal to 6%: 19.7%, the highest share since the fourth quarter of 2015.

- 5%-5.99%: 9.5%, the lowest share since Q3 2024

- 4%-4.99%: 17.9%, the lowest share in records dating back to 2013

- 3%-3.99%: 32.1%, the lowest share since Q3 2019

- Below 3%: 20.4%, the lowest share since Q2 2021