Realtor.com reports that the steep jump between current low mortgage payments and the much higher costs of buying a home today has created a nationwide “lock-in effect” that is suppressing mobility, constraining inventory, and hitting high-priced markets

Realtor.com has found that the sizable gap between existing mortgage payments and the cost of buying a home in today's market has created a powerful "lock-in effect" across the nation. The report finds that today's typical U.S. mortgage holder pays approximately $1,300 in principal and interest per month, however, to purchase a typical home in today's market, it would require a monthly payment of nearly $2,236, or a 73.2% increase in mortgage payments. This financial jump is the foundation of the lock-in effect, contributing to historically low mobility and a shortage of for-sale inventory.

Danielle Hale, Chief Economist, Realtor.com

"The lock-in effect isn't just theoretical; it's a significant factor weighing on the decisions of American homeowners," said Realtor.com Chief Economist Danielle Hale. "When the average mortgage holder is staring down a $1,000-a-month cost increase just to move, that requires incredible budget flexibility that many households simply cannot manage and others choose not to take on. The ultra-low rates of 2020–2021 have become golden handcuffs, starving many local housing markets of much needed supply."

Realtor.com attributes this “lock-in” phenomenon to the recent history of mortgage rates. Record-low mortgage rates in 2020 and 2021 ignited a boom in purchase and refi activity, resulting in more than one in four current mortgages dating to those two years alone. Once rates began rising in 2022, origination activity collapsed, with only 22.1% of outstanding mortgages originated from 2022 through August 2025. As rates and home prices rose, the total cost of financing a home purchase increased sharply, meaning current homeowners who secured low rates pay far less each month than new buyers, thus widening the gap that forms the lock-in effect.

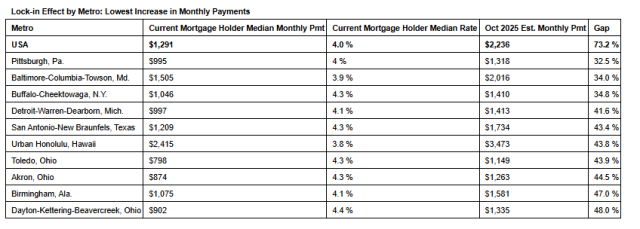

Measuring The Lock-In Effect

Even in more affordable markets, housing costs have risen, but the required increase in monthly payments to buy a typical home is smaller than the national average, making mobility more feasible.

Markets reporting the smallest lock-in effects include:

Get the NMP Daily

Essential stories, every weekday.

Pittsburgh, Pennsylvania: Homeowners face a 32.5% increase in monthly payments

Baltimore, Maryland: The increase is 34.0%

Buffalo, New York: The gap stands at 34.8%

"While low-cost markets offer the smallest penalty for moving, they weren't spared by rising rates, they simply started from a less locked-in position," added Hannah Jones, senior economic research analyst at Realtor.com. "Crucially, many owners in these areas hold higher-rate mortgages, meaning fewer are clinging to those extremely low rates. Their penalty for selling is smaller, but the cost of mobility is still high everywhere."

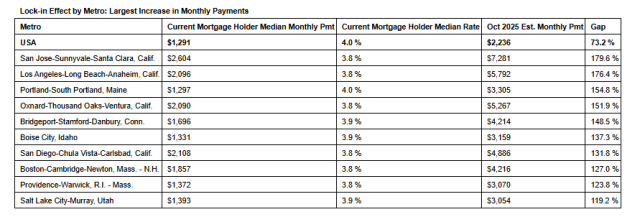

High-Priced Metros Are Most Locked-In

In high-priced metros, the financial jump is especially burdensome. Because homes are already expensive, buyers typically rely on larger mortgage balances, which amplifies the impact of rising rates. This has led to dramatic lock-in in markets like:

San Jose, California: A gap of 179.6% in estimated monthly payments

Los Angeles, California: A gap of 176.4%

Portland, Maine: A gap of 154.8%

And with home prices still well above pre-pandemic levels and mortgage rates high, options for locked-in homeowners to move often involve financial strategy, such as renting their current home out, downsizing, or relocating to a lower cost of living area. Unlocking the housing market will require a combination of easing affordability constraints, such as a sustained decline in mortgage rates, stronger income growth, or slower home-price appreciation, and perhaps most importantly, time.

Fannie Mae and Freddie Mac will eliminate abbreviated project reviews for condo applications dated on or after Aug. 3

Mortgage lenders have just over a week before Fannie Mae and Freddie Mac retire the abbreviated project-review pathways that have helped qualifying condominium loans avoid the cost and documentation demands of a Full Review.For loan applications dated on or after Aug. 3, Fan...

The retail lender is pairing Spanish-language operations with an ITIN program offering financing up to 85% LTV

Movement Mortgage has launched a centralized bilingual support team designed to help its retail loan officers serve Spanish-speaking borrowers, including originators who do not speak Spanish themselves.The Diverse Lending Support Team will provide bilingual LO assistants and...

J.D. Power finds better digital service, fee transparency, and issue resolution are strengthening trust while homeowners face mounting financial pressure

Contract signings fell 5.4% from May as elevated borrowing costs and record home prices continued to pressure affordability, particularly for first-time buyers