Mortgage rates are not likely to dip below 6% next year, and could roll back up to 6.5%, the Mortgage Bankers Association (MBA) says in its latest forecast for 2026.

The less-than-scintillating prediction is not far different from the one offered by MBA economists at the group’s annual convention in October in Las Vegas, except that the group of economists seem more certain now.

“This forecast becomes more likely as the Federal Reserve Board reaches the end of their cutting cycle next year,” they noted in their end-of-the-year forecast.

The Federal Open Market Committee (FOMC) announced the end to quantitative tightening at its last meeting, which took effect on Dec. 1. At the meeting, the FOMC announced that it will begin to add to their Treasury bill holdings, as needed, to sustain market liquidity.

Economists Mike Fratantoni, Joel Kan, and Judie Ricks also maintained their projection that U.S. home prices will effectively stagnate at the national level over the forecast horizon. Growth will slow, they said, to the 1% range by the end of 2025 and “dip slightly into negative territory” by late 2026.

They attribute slow price growth to the combination of high levels of inventory and weaker demand.

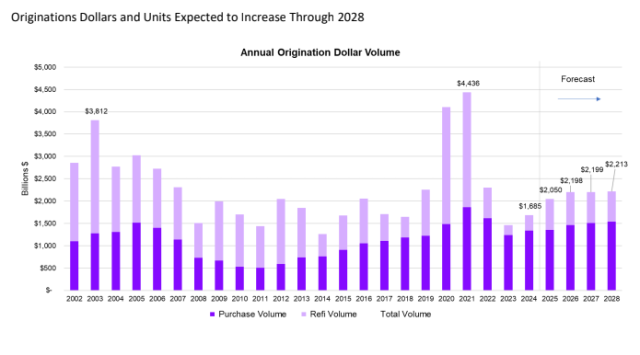

The MBA expects total single-family origination volume to total $2.2 trillion in 2026, up from $2.05 trillion in this year. Of that, purchase originations are expected to total $1.46 trillion compared to $1.36 trillion in 2025, as home sales gradually increase. Existing home sales will be supported by gradual growth in for-sale inventory and improving affordability, the three economists projected.

Refinance originations are expected to increase to $737 billion from $694 billion as brief spells of refi activity emerge during a year mortgage rate volatility.

New home construction will fall slightly next year, the MBA believes, and even further into 2027 before starting to move upward again in 2028. That means there will be no relief from the shortage in the number of houses to go around, which should keep prices high, even if they are not increasing.

Single-family production, after dipping next year from 947,000 units to 926,000, will spring back in 2027 with 967,000 units and again in 2028 with 976,000, the economists predict. Multifamily starts will slide in each of the next three years, they believe, from 409,000 units this year to only 320,000 in 2028.

On the commercial side, the MBA expects total originations to finish this year at $637 billion and continue strengthening into 2026, when the trade group expects production to hit $784 billion. For multi-family, it estimates $338 billion of originations in 2025 and $393 billion in 2026.

The growth in originations will be driven by increased refinances, as more loans mature, and by financing for acquisitions, the economists said.

Commercial market fundamentals have softened, they pointed out, with net operating income declining for commercial space – and especially for the multifamily sector. Vacancies have also increased in 2025, driven by office and multifamily. Property values have stabilized for most sectors except for industrial, which has seen more rapid price growth.