Hillary Clinton’s “It Takes a Village,” published almost 30 years ago, was about raising children. But it also could just as well be the title of J.D. Power’s latest mortgage origination satisfaction survey, especially in today’s housing market where rising loan rates and ever higher prices are befuddling many would-be buyers.

Released today, the study finds that it takes more than just fancy, fast electronics to please borrowers. Not that artificial intelligence in and of itself doesn’t suffice. But today’s borrowers often need a little hand holding, too.

Those lenders which recognize that fact are doing better than those who don’t.

“Consistently, we’re seeing that lenders that play an active advisory role in helping their clients navigate the current market are earning significantly higher customer satisfaction, loyalty and advocacy scores that those who are treating mortgage lending as a transactional process,” said Bruce Gehrke, director of wealth and lending intelligence at the Power firm.

Mortgage rate volatility, particularly when they shoot up after being told costs are going to fall, is playing hell with potential buyers. Or, as the survey says, “put(s) a strain on mortgage customers.”

But, lenders who used those challenges to their benefit by playing a more hands-on, advisory role are earning the highest marks for customer satisfaction, according to the survey. “Other lenders have struggled,” the report says.

The study measures satisfaction in six factors: communication, digital channels, level of trust, loan offering meets my needs, made it easy to do business with, and people. The findings are an affirmation of sorts of what the advisory company found in the 2023 survey – that some borrowers require more personal service.

“It’s something we started to see last year,” Gehrke told NMP. “This year solidified it. Borrowers expect more and the lenders who are going that way are getting the benefit.”

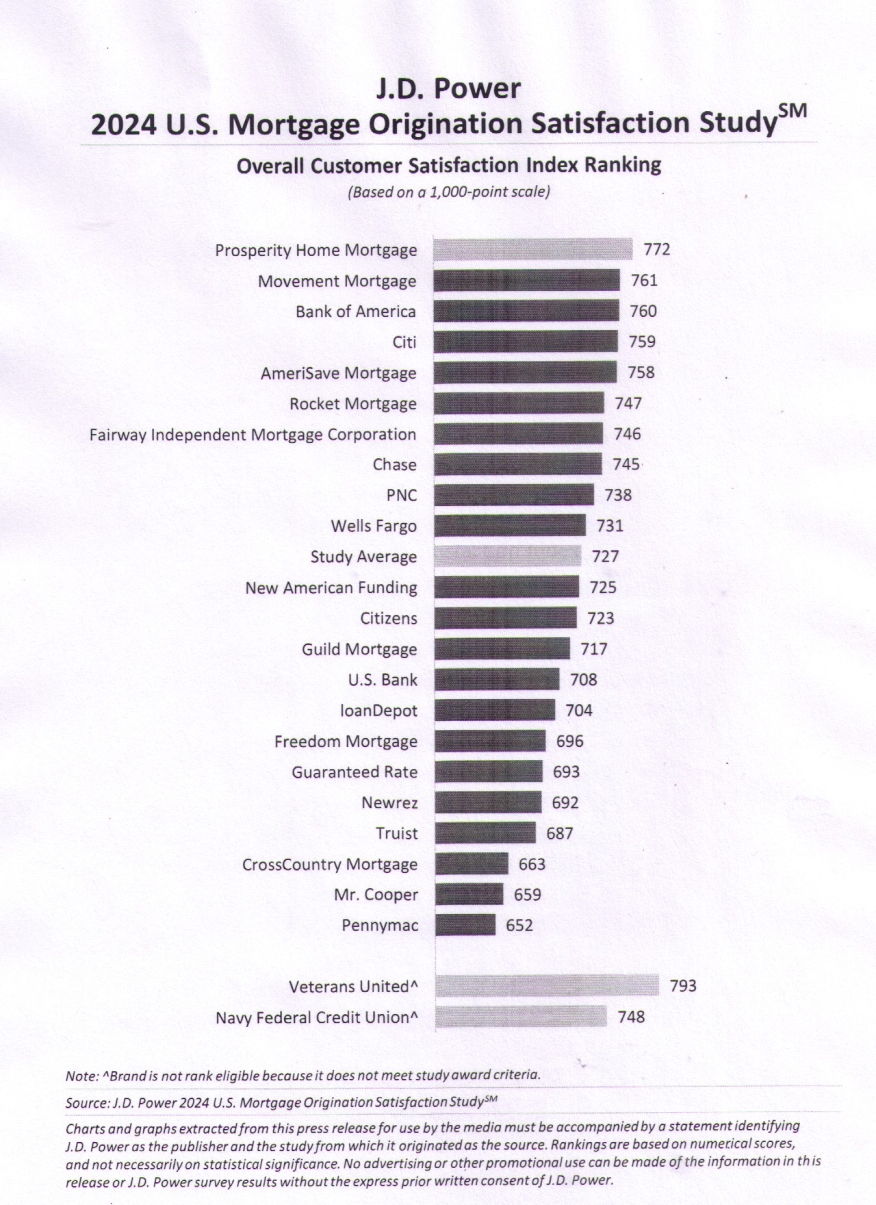

Prosperity Home Mortgage, a subsidiary of Long & Foster, a large Mid-Atlantic real estate firm, ranks highest in this year’s survey, followed by Movement Mortgage, a South Carolina-based lender founded during the Great Recession, and Bank of America. But a dozen lenders fell below the average score for all companies, with Pennymac at the bottom of the list. Only 10 were above average.

The survey is based on 7,500 responses from people who took out a new mortgage during the 12-month period ended in September or refinanced an old loan.

Power doesn’t release the entire study, which it says is proprietary. But Gehrke said in a telephone interview that lenders who are “more personal in their approach,” particularly earlier in the lending process, are reaping rewards in terms of loan volumes.

Borrowers “want to talk even before they start the application process because the market is shifting so much, so fast,” he said.

Indeed, timing seems to be everything. Overall satisfaction was 41 points higher (on a 1,000-point scale) when lenders engage customers early, connecting when they are first start thinking about buying a house, as opposed to when lenders get involved once people begin actively shopping.

Worse, it was 107 points lower when lenders come into the picture when buyers are ready to apply for financing.

Lenders who act as advisors through the entire process also score significantly higher. When borrowers strongly rely on their lenders, their satisfaction jumps 133 points higher than those who don’t call on the lender for advice or rely on lender expertise.

The only one of the six factors that showed gains in the latest study is people, but only by a single point. At the same time, when a lender’s local representative is directly involved in the origination process, the overall satisfaction score rises by 40 points.

Overall, though, customer delight fell by 3 points from a year ago, when the satisfaction level lurched higher by 14 points year over year.