A growing share of U.S. home purchase agreements are collapsing before closing, highlighting persistent strain in the housing market as elevated mortgage rates and affordability challenges continue to weigh on buyers and sellers.

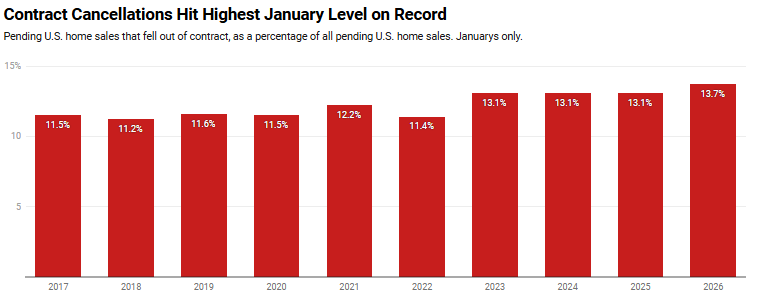

Redfin found that 14.3% of homes that went under contract in January ultimately fell out of escrow — the highest share ever recorded for that month and equivalent to roughly one in seven transactions. The figure represents a notable increase from both pre-pandemic norms and recent years, underscoring mounting friction in the homebuying process.

The rise in canceled deals reflects ongoing affordability constraints driven by mortgage rates that remain significantly higher than pandemic-era lows. Even modest rate fluctuations can materially impact monthly payments, prompting some buyers to reconsider purchases or fail to secure financing under revised terms. Additionally, buyers are increasingly cautious about overpaying in a market where prices remain elevated despite slower sales activity.

“More buyers are backing out,” said Alin Glogovicean, a Redfin Premier agent in Los Angeles, where 16.7% of home purchase agreements were cancelled in January, up from 15% a year earlier. “They’re second-guessing the wisdom of making a huge purchase when there’s a fear in the back of their mind about the state of the economy and the uncertainty of their finances. That’s particularly true when they’re first-time buyers who don’t have equity from a previous home sale, and they’re using most or all of their savings on a down payment.”

Economic Uncertainty Swaying Buyers

Concerns about inflation, employment stability, and broader financial conditions are causing some prospective buyers to pause major financial commitments. At the same time, some sellers are rejecting renegotiation requests tied to inspection findings or appraisal gaps, leading to more terminated contracts.

While rising cancellation rates can signal market stress, they may also reflect shifting leverage dynamics. During the pandemic housing boom, competition was intense and cancellations were relatively rare as buyers rushed to secure limited inventory. Today’s environment offers buyers more negotiating power, allowing them to exit deals if terms become unfavorable or financial conditions change.

A Dip in Demand

The increase in failed transactions aligns with broader signs of cooling housing demand, including slower sales pace and longer time on market. However, limited housing supply and homeowner reluctance to sell — often due to the “lock-in effect” of low existing mortgage rates — continue to prevent significant price declines.

Measuring a Metro Impact

In San Antonio, 21.2% of home-purchase agreements were canceled in January, the highest share of the 47 major U.S. metros Redfin analyzed. The Texas market was followed by Atlanta (18.5%), Cleveland (17.9%), Riverside, Calif. (17.5%), and Orlando, Fla. (17.3%) rounding out the top five.

Cancellations were especially common in those places largely because they’re mostly buyer’s markets, with many more home sellers than buyers, giving buyers the option to back out of deals and move on to the next house. In San Antonio, for instance, there are twice as many sellers as buyers, and in Atlanta, there are 80% more.

On the other end of the spectrum, just 3.5% of home-purchase agreements in San Francisco were canceled in January, the lowest share of the metros Redfin analyzed. The Bay Area was followed by Nassau County, N.Y. (4.8%); San Jose (5.3%); Milwaukee (7.6%); and Oakland, Calif. (8.4%).