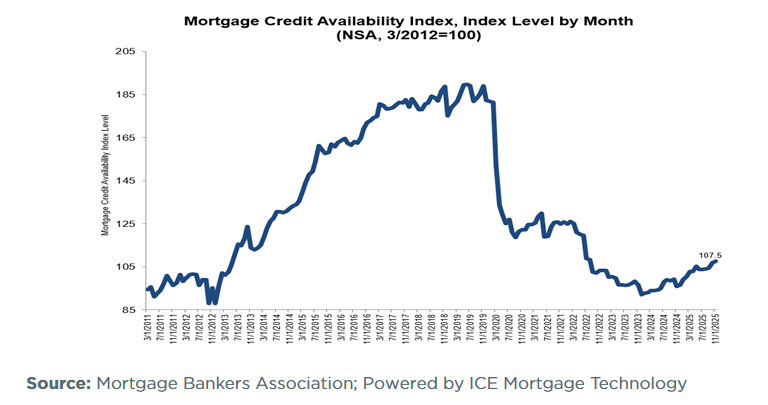

Mortgage credit availability in the U.S. contracted in December as lending standards tightened across major loan categories, according to the Mortgage Credit Availability Index (MCAI) released by the Mortgage Bankers Association (MBA).

The MCAI, which measures the ease of obtaining mortgage credit using data from ICE Mortgage Technology, fell 2.6% to 104.7 last month. A declining index indicates a reduction in credit supply.

The overall decline in the MCAI reflected a broad pullback in lending, with both conventional and government-backed mortgage products tightening. The Conventional MCAI dropped 3.6%, while the Government MCAI — which includes FHA, VA, and USDA loan programs — decreased 1.4%. Within conventional loans, both Jumbo and Conforming segments slid, with the Conforming index falling 3.8% — its lowest level since the survey’s inception in 2011.

“Mortgage credit availability increased on an annual basis in December due to increased loan program offerings and industry capacity compared to the end of 2024. However, on a monthly basis, credit supply declined to its lowest level in three months, with tightening in both conventional and government loan offerings,” said Joel Kan, MBA’s vice president and deputy chief economist. “The December decrease reversed gains from the prior two months, driven by a reduction in loan programs, including ARM loans and cash-out refinances, along with a tightening in documentation requirements. Additionally, the conforming and jumbo indexes both saw declines in December, with the conforming index hitting its lowest level since the survey’s inception in 2011.”

Analysts view the MCAI as a leading indicator of lending conditions, with pullbacks potentially signaling more cautious underwriting and risk management by lenders. The movement in credit availability comes amid broader mortgage market adjustments, including shifts in application activity and interest rate trends that have weighed on borrowing demand late in 2025 and into early 2026.

The MCAI is benchmarked to a base value of 100 in March 2012, and remains above that level despite the recent decline, indicating that credit is still more accessible than in earlier periods, even as relative tightening occurs.