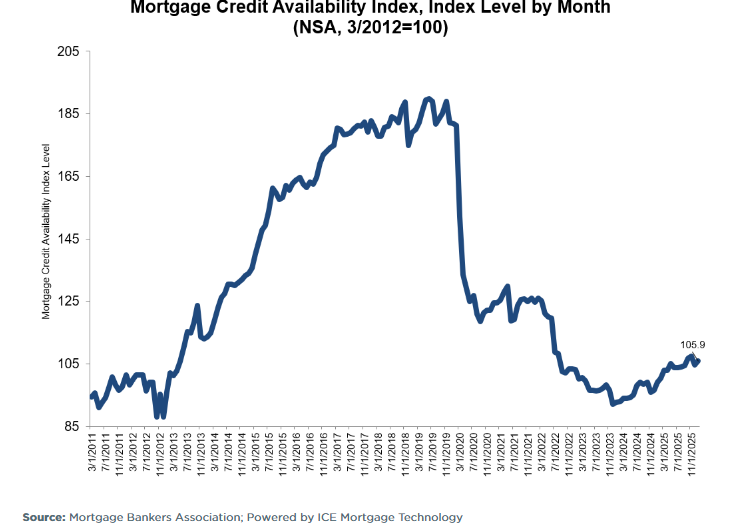

Mortgage credit availability in the U.S. expanded in January, according to the Mortgage Bankers Association’s (MBA) latest Mortgage Credit Availability Index (MCAI), signaling a loosening of lending standards as the housing market begins 2026.

The MCAI, which tracks the ease of obtaining mortgage credit using data from ICE Mortgage Technology, increased in January, with broader loan program offerings contributing to the gain. An upward movement in the index indicates credit conditions are loosening, potentially improving access to financing for homebuyers and refinancers.

Key components of the index showed notable increases. Conventional mortgage credit availability rose, supported by more jumbo and conforming loan programs, while government loan credit also saw growth. The uptick reflects lenders’ willingness to offer a wider array of products, particularly for borrowers with stronger credit profiles, as the year begins.

MBA analysts noted that expanded offerings for jumbo and Non-QM loans, as well as cash-out refinance options, underpinned the January improvement. These expanded product lines could benefit well-qualified borrowers looking to tap equity or access larger loan amounts.

“Mortgage credit availability increased in January, as lenders broadened their offerings of ARM loans, cash out refinances, and loans on second homes. Most of these require lower LTV and higher credit scores,” said Joel Kan, MBA’s VP and deputy chief economist. “The beginning of the year is typically when lenders start to position themselves for the spring homebuying pick up, and recent dips in mortgage rates have provided windows of refinance opportunities, including refinances into ARM loans. Jumbo credit availability expanded almost 3% over the month, with the growth in supply of both jumbo and Non-QM loan programs.”

The January increase follows a December 2025 contraction in credit availability, when the MCAI dipped as lenders pulled back on some conventional and government loan programs. That tighter environment reversed in the new year, with broader credit supply suggesting lenders are adjusting to market conditions marked by relatively stable interest rates and ongoing demand for mortgage financing.

Looser credit availability early in the year may help support spring homebuying activity if sustained, though industry observers continue to watch broader economic factors that influence mortgage demand and underwriting.