Aaron Clark on process, perseverance, and partnerships

By Andy Baker, Special to National Mortgage Professional

When Aaron Clark explains his success in the mortgage business, he doesn’t talk about luck, timing, or even products. He talks about process. As a veteran firefighter, Clark is used to walking into chaos with calm confidence, knowing that survival depends on everyone following the playbook. “Like fighting a fire, you know who’s driving, who’s catching the hydrant, who’s on the hose,” he explained. “Everybody has their role, and you move step by step by step.”

Firehouse Mortgage co-owner Aaron Clark blends his emergency-response training with a structured, client-focused approach to origination.

Firehouse Mortgage co-owner Aaron Clark blends his emergency-response training with a structured, client-focused approach to origination.

That same discipline — process-driven, team-oriented, and unshakable under pressure — has carried over into his second career as a mortgage broker and co-owner of Firehouse Mortgage. Whether he’s on shift at the firehouse or managing a full pipeline of loans, Clark relies on structure and accountability to guide clients through one of the most stressful financial decisions of their lives. For him, mortgages are another kind of emergency response: clients may not face flames, but the uncertainty feels just as real, and they need someone who knows how to lead them through.

Why Firefighters And Police Excel In Mortgages

Clark is quick to point out that his success didn’t come because he had more hours in the day than other loan officers. It came because he treated mortgages the same way he treated emergencies: with structure, focus, and follow-through. Firefighters and police officers share traits that translate directly into origination. They are trained to operate within a system of clear processes. They know how to stay calm under pressure, even when those around them are panicking. They thrive on teamwork, understanding that no one person can carry the load alone. And above all, they bring a service-first mindset, always putting the needs of others before their own.

That combination, Clark believes, is what makes former firefighters, police officers, and other first responders such a natural fit for the mortgage business. Their ability to follow a playbook, perform under stress, and work collaboratively gives them an advantage in an industry where deadlines are tight, compliance rules are strict, and client emotions often run high. It also helps that the uniform automatically fosters trust among his target audience of middle-market borrowers. Aaron shares that his clients and referral partners assume they can trust him since his job is focused on serving others, often in great danger. This echoes the experience of other originators from service professions. In a recent National MortgageProfessional cover story, Anthony Marone, a police sergeant in the Township of Aberdeen, described how his law enforcement background gave him the discipline and empathy to succeed in mortgages. Clark’s journey adds to that story, showing how public service builds the skills brokers need most today, and why those who have worn uniforms often find new purpose in helping families secure homes.

Clark on duty as a Houston-area firefighter, where he learned discipline, teamwork, and the essential skills that now shape his mortgage career.

Clark on duty as a Houston-area firefighter, where he learned discipline, teamwork, and the essential skills that now shape his mortgage career.

Why His Story Matters

Clark’s journey underscores why service-minded professionals thrive in mortgages. Like Marone’s police background, Clark’s firehouse experience instilled discipline, empathy, and teamwork. Those same qualities now fuel his success as a broker. In an industry that demands adaptability, his story is proof that mindset often matters more than market cycles. For mortgage professionals, the lesson is clear: focus on process, lean on your team, and put the client first.

Problem-Solving Under Pressure

During the frenzied days of COVID lending, Clark faced the same bottlenecks as everyone else: appraisals dragging on for weeks and threatening to derail closings. Instead of waiting helplessly, he hunted for a workaround. He found a little-known AMC willing to return appraisals within 72 hours for a $100 rush fee. While others were stuck waiting 30 to 45 days, Clark was delivering results in three. “That was a worthy investment,” he recalled. “Even when it was bad, I still found a way to get it done. That won people over — they knew I’d figure it out.” This helped Aaron write 162 loans in 2021 according to Modex.

That resourcefulness became part of his professional identity. Clients, agents, and even other mortgage professionals recognized that if Clark was on the loan, delays would not derail the deal. His problem-solving reflected the same instincts he relied on in the firehouse: quickly sizing up the situation, identifying the right tool, and executing with confidence.

Choosing Wholesale Partners

That same pragmatism extends to Clark’s relationships with wholesale lenders. He doesn’t get distracted by flashy conference booths or aggressive sign-up campaigns. “I want to see how personable they are,” he said. “Not just, ‘sign up, sign up, sign up.’ What do you have that can help me and my borrowers?” He evaluates partners not by promises, but by how well they fit the real needs of his business and his clients.

Supporting the industry also matters. Clark and his wife Rachel, who co-leads Firehouse Mortgage, are passionate advocates for the broker channel. Rachel serves as executive director of the Broker Action Coalition (BAC), and together they make frequent trips to Washington, D.C., to promote pro-broker and pro-consumer initiatives, like the trigger lead ban. For Aaron, lenders that stand behind these causes send a powerful signal: they’re invested not just in transactions, but in the long-term health of the industry.

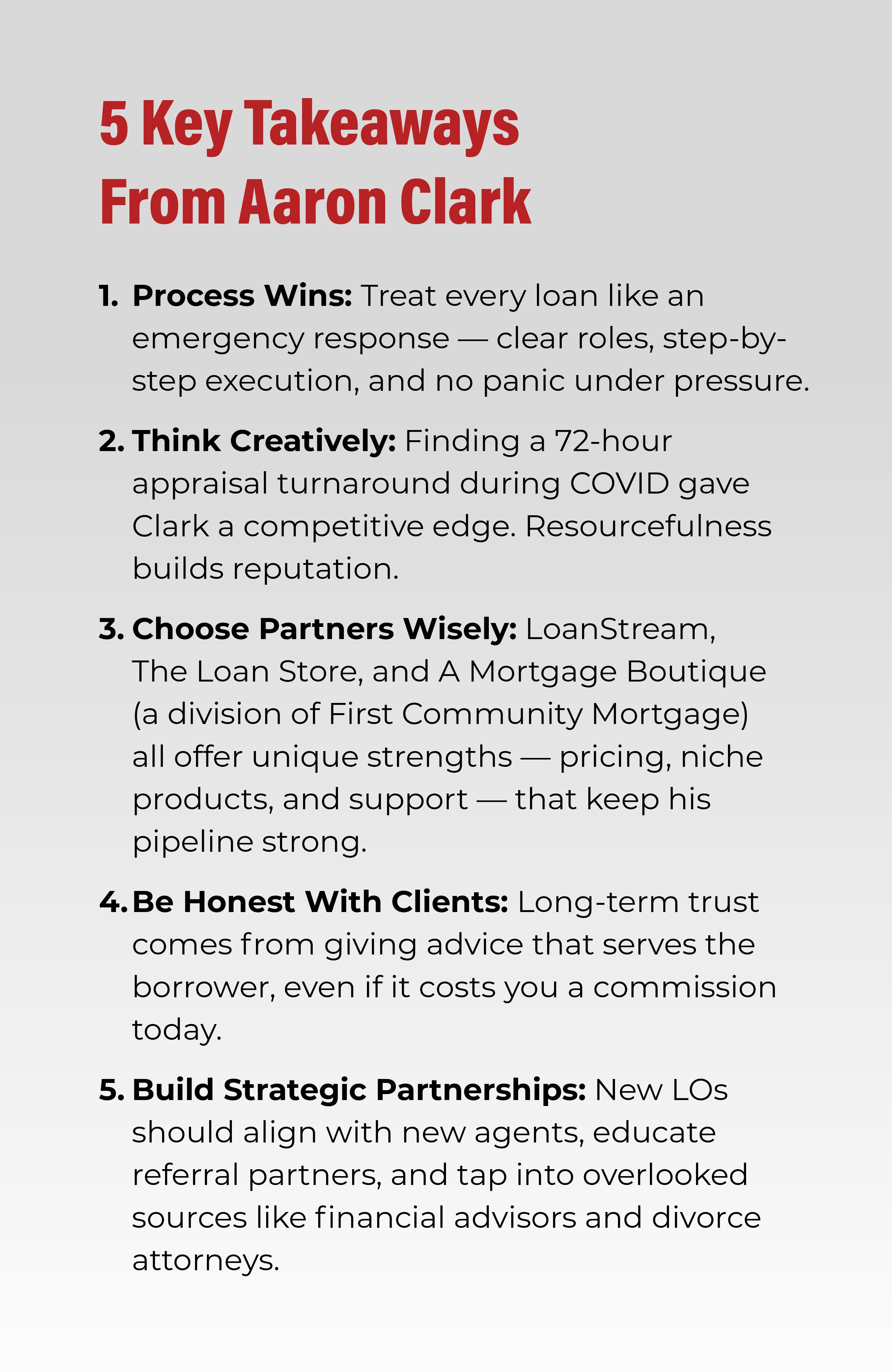

Recently, LoanStream stood out with a DSCR program that went beyond the industry standard. “Everybody has DSCR, but they had a layer that worked better for my kind of investors,” Clark explained. That edge made a measurable difference for his clients, and it convinced him to sign on. He also praised The Loan Store for consistently sharp pricing on investor-focused products. In a market where reliability and value matter more than ever, The Loan Store proved to be a partner he could trust. And for his junior loan officers, Clark relies on A Mortgage Boutique, a division of First Community Mortgage, which takes a more personal approach. “They’ll coach and hand-hold my newer LOs so they can build confidence,” he said. “That kind of support is huge when you’re starting out.”

Together, these relationships illustrate Clark’s philosophy: surround yourself with partners who make you stronger in front of clients, reinforce your team behind the scenes, and stand up for the industry that allows brokers to thrive.

A Schedule That Defies Labels

From the outside, some people assume that because Clark splits time between firefighting and mortgages, the latter must be a side hustle. Clark laughs at the notion. “I tell people I’m part-time, but I put in full-time hours,” he said. When he’s at the firehouse, his primary responsibility is to his crew: daily training, truck checks, emergency calls. In between, he manages borrower emails and responds to the most urgent needs. On his mortgage days, the rhythm is different, but no less demanding. He starts with a workout, spends hours at the office monitoring files, fielding calls, and answering client questions, and then remains available well into the evening. “If I’m not on shift, I’ll take a call up to 10 p.m. and on weekends,” he said.

In 2024, that “part-time/full-time” rhythm added up to more than $20 million in production across 74 loans, according to Modex, with the vast majority in purchase transactions. His mix leaned heavily toward conventional and VA loans, with FHA filling the gap, and his average loan size landed just under $280,000. Most of that business came from Houston and surrounding communities, where Clark’s local relationships helped him serve middle-market borrowers.

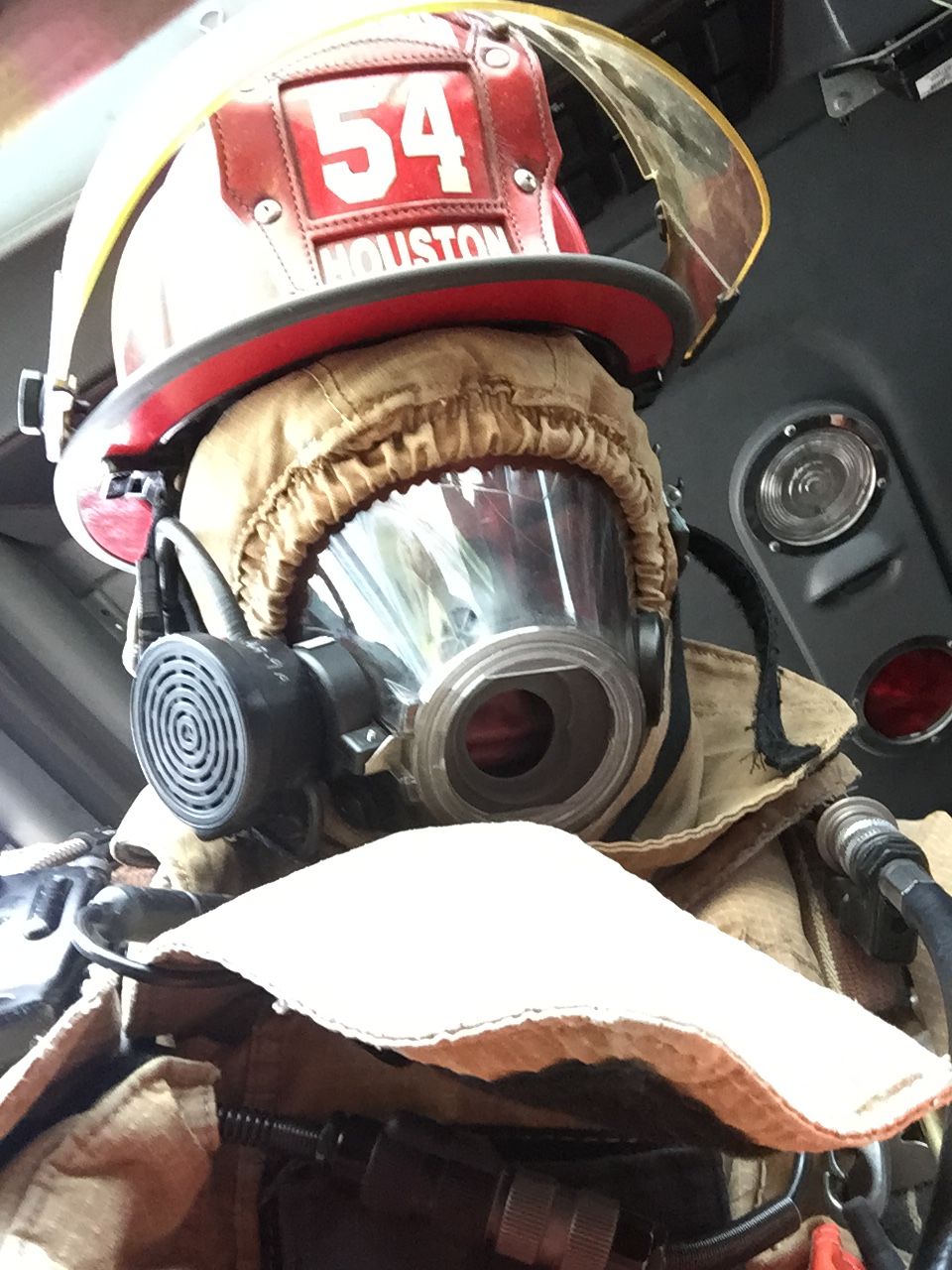

Fully masked and mission-ready, Clark embodies the readiness and precision that later defined his workflow at Firehouse Mortgage.

Fully masked and mission-ready, Clark embodies the readiness and precision that later defined his workflow at Firehouse Mortgage.

This transparency about his availability has become part of his appeal. He doesn’t pretend to be chained to a desk from nine to five, but he makes it clear to borrowers that he will be there when it counts. “I tell them, I’m a fireman — if I’m at the station, I’ll get back to you, but it might not be immediate. They appreciate the honesty.” In a business where communication breakdowns often frustrate clients, Clark has turned clear expectations into a competitive advantage.

As a veteran firefighter, Clark is used to walking into chaos with calm confidence, knowing that survival depends on everyone following the playbook. “Like fighting a fire, you know who’s driving, who’s catching the hydrant, who’s on the hose. Everybody has their role, and you move step by step by step.”

Technology As A Firefighter’s Equipment Belt

Clark compares his mortgage technology to a firefighter’s gear — every tool has a purpose, and each one makes the job safer, faster, or more efficient. He uses Arrive to intake applications and ensure compliance, supported by a loan portal that communicates directly with the system. Monday.com had been part of his process for collaboration with processors, but he is now transitioning out of it as the portal expands, allowing seamless note-sharing and updates between him and his team.

This integrated tech stack saves time and cuts down on errors. It is the equivalent of walking into a fire with reliable hoses, sharpened axes, and a breathing apparatus that won’t fail. Each tool matters, and the way they work together determines whether the mission succeeds. Yet Clark is candid about his weak spots. Just as a firefighter might forget to sharpen a saw or check a hose, he admits his biggest blind spot is follow-up with past clients. “If I were better at that, I’d be even busier,” he said. Acknowledging the gap reflects his commitment to improvement, and it’s a reminder to other originators that even the strongest setups need regular checks and upgrades.

Aaron Clark stands beside his wife (second to the left) Rachel Clark and their two children (far left and far right). Together, the couple co-leads Firehouse Mortgage and regularly advocates in Washington, D.C., on pro-broker and pro-consumer issues.

Aaron Clark stands beside his wife (second to the left) Rachel Clark and their two children (far left and far right). Together, the couple co-leads Firehouse Mortgage and regularly advocates in Washington, D.C., on pro-broker and pro-consumer issues.

Straight Talk With Borrowers

What sets Clark apart even further is his straightforwardness with borrowers. He is not afraid to tell a client that a refinance doesn’t make sense. “You might save $50 to $100 a month, but if the risks outweigh the benefits, it’s not worth locking yourself in,” he explained. “If it’s best for your family, I’ll do it — but I’ll always give you the full picture.” That honesty sometimes means passing on an immediate commission, but it builds loyalty and referrals that are far more valuable in the long run.

Mentorship and Partnerships

Clark also sees himself as a mentor. At a recent industry event, a 19-year-old, newly licensed loan officer asked him where to begin. Clark’s advice was to align with peers. “Find new real estate agents who are hungry to grow. They’re not tied to veterans yet. Grow together, split marketing costs, and show up together,” he said. He encouraged the rookie to teach classes for agents, such as how to read loan estimates — something many agents still misunderstand. “If you educate them, they’re more willing to use you,” he said.

He also reminds new brokers to leverage the depth of their wholesale partners. “Even if you’re new, your wholesale partners bring years of experience you can lean on,” he said. Selling yourself as part of a broader team — including account executives, underwriters, and wholesalers — instantly increases credibility. Beyond real estate agents, Clark encourages tapping underutilized referral sources such as financial advisors and divorce attorneys. Both, he explained, often encounter clients who must make immediate, life-changing housing decisions. Aligning with them can open valuable new pipelines.

The Value Of Flexibility

For Clark, flexibility remains the greatest reward of being a mortgage broker. He has considered banking but prefers the independence of the broker model. “If I want more play money, I hustle. If I’m good, I can ease off. That flexibility means a lot,” he said. That freedom allows him to blend two demanding careers, continue serving his community as a firefighter, and still carve out time for family. It is also a philosophy he shares with other brokers: success is about balancing effort and priorities, not about working endlessly without boundaries.

Technology As A Firefighter’s Equipment Belt

Clark compares his mortgage technology to a firefighter’s gear — every tool has a purpose, and each one makes the job safer, faster, or more efficient. He uses Arrive to intake applications and ensure compliance, supported by a loan portal that communicates directly with the system. Monday.com had been part of his process for collaboration with processors, but he is now transitioning out of it as the portal expands, allowing seamless note-sharing and updates between him and his team.

This integrated tech stack saves time and cuts down on errors. It is the equivalent of walking into a fire with reliable hoses, sharpened axes, and a breathing apparatus that won’t fail. Each tool matters, and the way they work together determines whether the mission succeeds. Yet Clark is candid about his weak spots. Just as a firefighter might forget to sharpen a saw or check a hose, he admits his biggest blind spot is follow-up with past clients. “If I were better at that, I’d be even busier,” he said. Acknowledging the gap reflects his commitment to improvement, and it’s a reminder to other originators that even the strongest setups need regular checks and upgrades.

Aaron Clark stands beside his wife (second to the left) Rachel Clark and their two children (far left and far right). Together, the couple co-leads Firehouse Mortgage and regularly advocates in Washington, D.C., on pro-broker and pro-consumer issues.

Aaron Clark stands beside his wife (second to the left) Rachel Clark and their two children (far left and far right). Together, the couple co-leads Firehouse Mortgage and regularly advocates in Washington, D.C., on pro-broker and pro-consumer issues.

Straight Talk With Borrowers

What sets Clark apart even further is his straightforwardness with borrowers. He is not afraid to tell a client that a refinance doesn’t make sense. “You might save $50 to $100 a month, but if the risks outweigh the benefits, it’s not worth locking yourself in,” he explained. “If it’s best for your family, I’ll do it — but I’ll always give you the full picture.” That honesty sometimes means passing on an immediate commission, but it builds loyalty and referrals that are far more valuable in the long run.

Mentorship And Partnerships

Clark also sees himself as a mentor. At a recent industry event, a 19-year-old, newly licensed loan officer asked him where to begin. Clark’s advice was to align with peers. “Find new real estate agents who are hungry to grow. They’re not tied to veterans yet. Grow together, split marketing costs, and show up together,” he said. He encouraged the rookie to teach classes for agents, such as how to read loan estimates — something many agents still misunderstand. “If you educate them, they’re more willing to use you,” he said.

He also reminds new brokers to leverage the depth of their wholesale partners. “Even if you’re new, your wholesale partners bring years of experience you can lean on,” he said. Selling yourself as part of a broader team — including account executives, underwriters, and wholesalers — instantly increases credibility. Beyond real estate agents, Clark encourages tapping underutilized referral sources such as financial advisors and divorce attorneys. Both, he explained, often encounter clients who must make immediate, life-changing housing decisions. Aligning with them can open valuable new pipelines.

The Value Of Flexibility

For Clark, flexibility remains the greatest reward of being a mortgage broker. He has considered banking but prefers the independence of the broker model. “If I want more play money, I hustle. If I’m good, I can ease off. That flexibility means a lot,” he said. That freedom allows him to blend two demanding careers, continue serving his community as a firefighter, and still carve out time for family. It is also a philosophy he shares with other brokers: success is about balancing effort and priorities, not about working endlessly without boundaries.

ndustry’s biggest bottleneck is not underwriting itself — it is the uncertainty that reaches underwriting too late in the process. When validation happens upstream, speed follows naturally.

The long tail of loss mitigation is now coming into view as FHA’s post-pandemic relief tools give way to repeat defaults, exhausted options, and a swelling foreclosure pipeline

Katie Jensen

Connect with your local mortgage community.

Meet your your colleagues, both national and local, by attending an event in your area.