And unlike the legacy CRMs that flood consumers with identical messages, Lendware’s strength is customization. Gutierrez said he’s seen real estate partners receive the same stock template email from four different loan originators. “When I go to that customizable point, I want my CRM to sound like Brian Gutierrez,” he said. “To this day there are still emails going out that look identical across mortgage platforms because they're all utilizing the same CRM.”

This is where the Lone Ranger gains leverage: the ability to operate like a modern, data-driven retail shop without abandoning independence. “If you don't go with one of those platforms … you can be the Lone Ranger working for ABC Brokerage … and have an even better, less archaic approach in your business,” Gutierrez said. “If you're a Lone Ranger, this will level you up.”

Glantz frames the moment more broadly. Consolidation, he said, doesn’t eliminate opportunity — it creates it. “In every other industry, consolidation also frees opportunities for additional disruption,” he said. “Teams, or even entire companies that were rolled up, will then break off and start something new again.”

In a refinance cycle defined by speed, data, and automation, the battleground is no longer just who can call the borrower first — it’s who can build the fastest, smartest tech without surrendering their independence. Lendware’s bet is that brokers don’t need to join a giant platform to win. They just need the right weapons.

Is AI The Only True Winner?

If UWM represents the industrial-scale future and Lendware the precision weaponry for independents, the next question is harder, and far more uncomfortable: what if AI eventually replaces loan officers altogether?

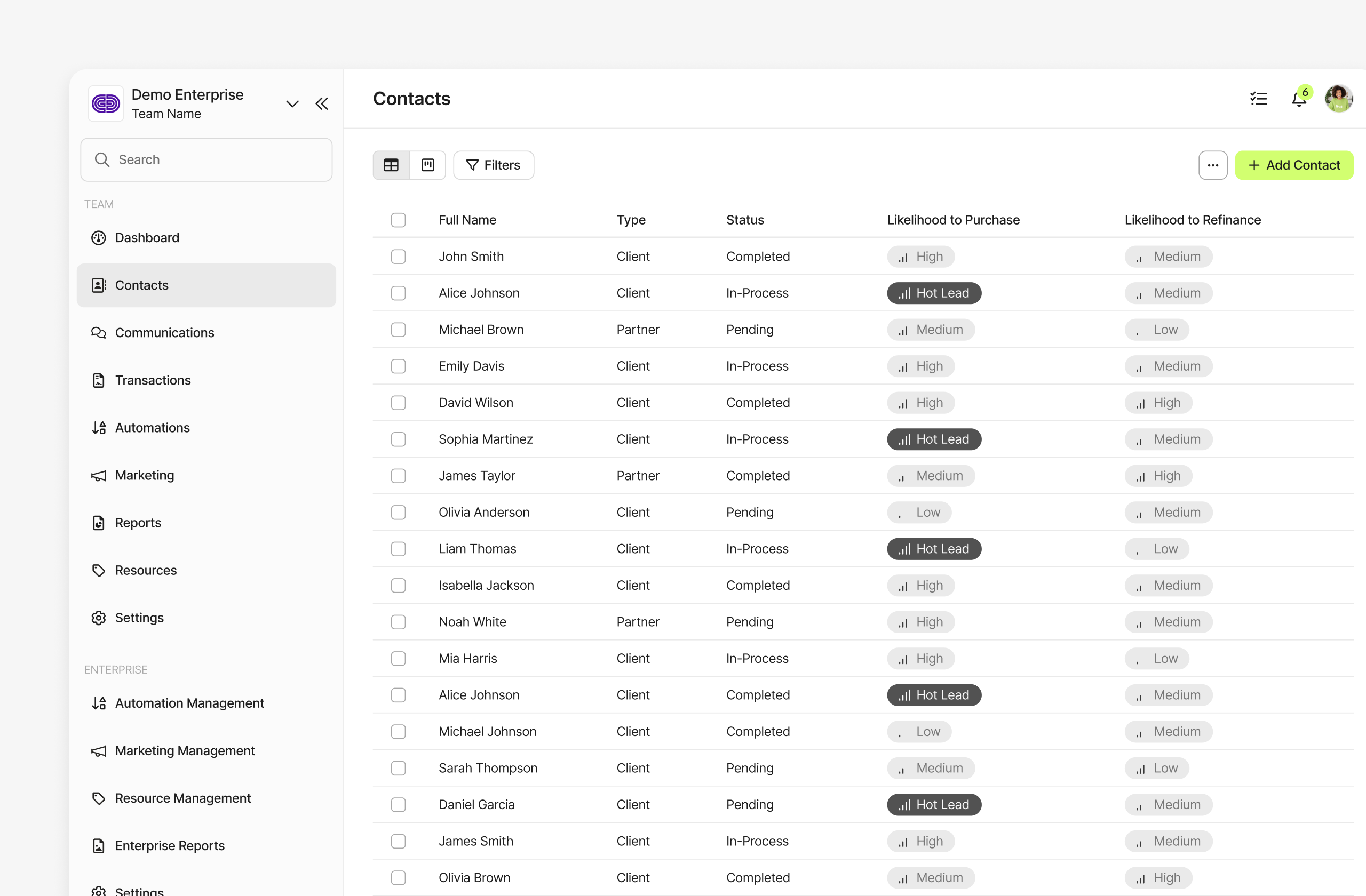

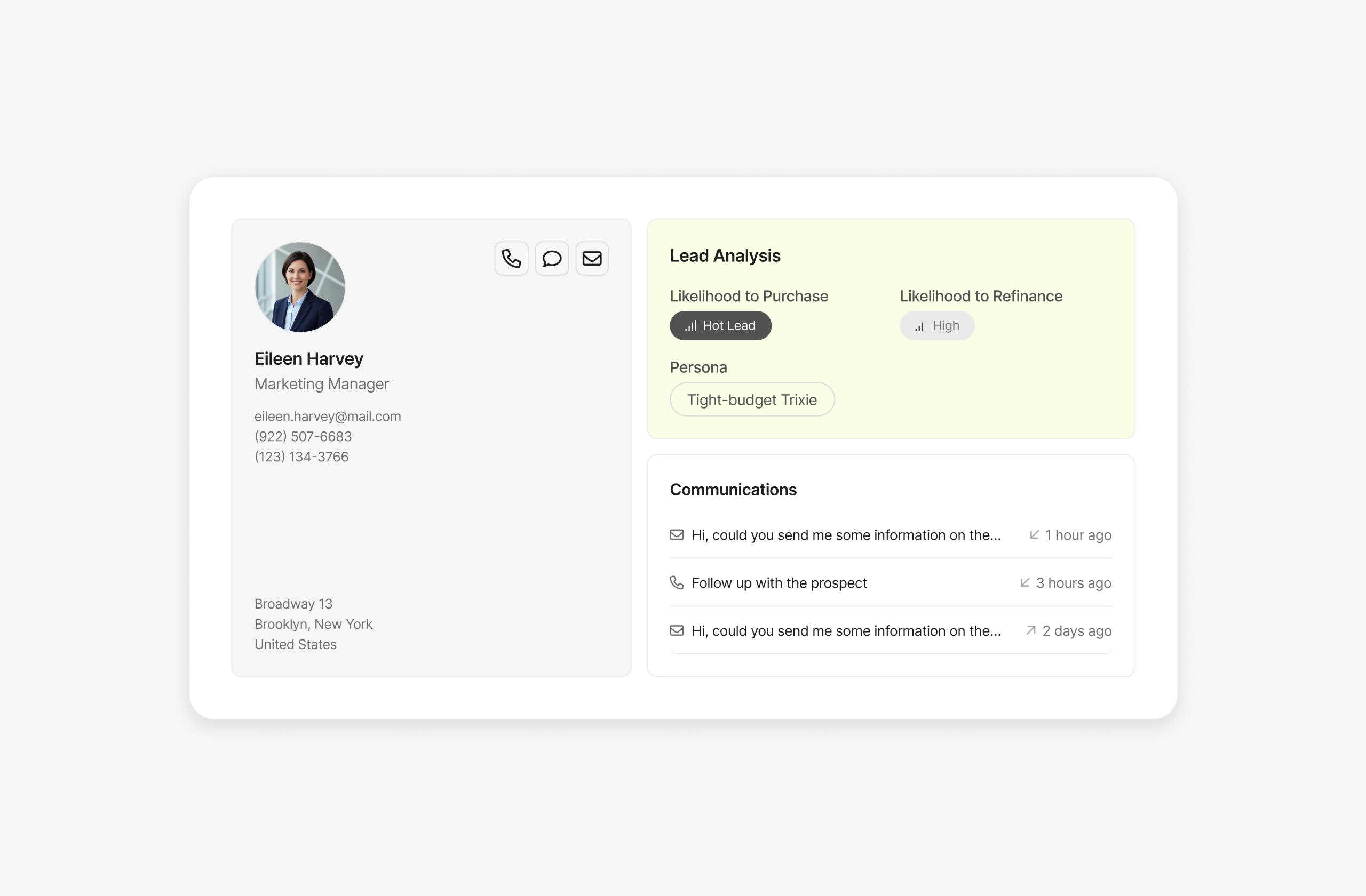

Researchers at MIT have already begun sketching the outlines of that possibility. In Project Iceberg 2025, a study that reads like a blueprint for the next phase of mortgage automation, the findings are blunt. Current AI tools are technically capable of performing tasks worth 11.7% of total U.S. wage value or about $1.2 trillion a year across an economy of 151 million workers and more than 32,000 distinct skills. Loan officers weren’t singled out, but much of the work MIT classifies as highly automatable, like document reading, data extraction, rule-based decision-making, templated writing, matches the workflows that define originators. And researchers say that's only the tip of the iceberg.

Below the waterline sits a far deeper layer of invisible, cognitive tasks — the scanning, sorting, calculating, checking, logging, and assembling — that determine how a loan file is actually built. It is that submerged mass of labor that AI is already beginning to devour.

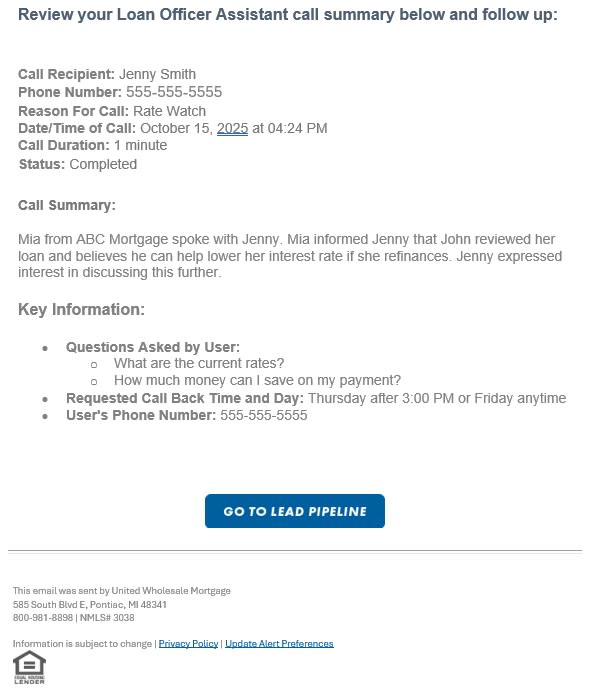

Fairway Home Mortgage COO Len Krupinski confronted that tension directly when discussing tech tools for non-delegated correspondent bankers. Even as he emphasizes Fairway’s culture of personal service, he’s candid about what agentic systems can do. “There's only so many loan officers that could be available at any given time, and the thing is, with agentic AI, it can make several calls at one time,” he said. “It’s the ultimate multitasker.”

Inside Fairway’s own tests, the shift is already material. Krupinski described “agentic sales assistants” as so convincing that “it’s hard to tell that you’re not talking to a human.” Borrowers rarely disengage, he said. “Most people don't even hang up because the conversation is going so well … they had to turn it off because they were getting so much business. There were too many leads coming in so fast.”

It’s a dramatic revelation to not only Fairway, but any lender that’s built on a relationship-first model. “It's like the cold caller's almost being eliminated with this agentic assistant, and it's having better results than the cold callers — that's what I've heard.”

As a distributed retail lender, Krupinski insists that AI cannot replace the emotional bond between borrowers and Fairway’s originators. “If you do a good job for a customer, I don't think there's any technology that replaces that,” he said.