New First Street Foundation analysis finds 57 banks with a total of $627 billion in real estate loans exposed to “material financial risk” from climate impacts.

The picture of climate change-related risks embedded in banks’ mortgage lending portfolios gains color and clarity as the accelerating impacts of extreme weather disrupt nation-wide property markets, the affordability and availability of insurance, and regulators’ ability to price it.

A new analysis published by the First Street Foundation, a climate change intelligence and modeling firm, titled the “11th National Risk Assessment: Portfolio Pressures,” shows that 57 banks with a total of $627 billion in real estate loans (10.9% of all loans in the country) could face “material financial risk” on account of their portfolios' climate exposure.

Of those banks modeled as surpassing federal regulators’ “material risk” threshold, which the U.S. Security Exchange Commission (SEC) set as a 1% annual likelihood of experiencing losses large enough to impact financial performance, operations, reputation, and legal standing, 95% (54 banks) were small regional or community banks.

The report serves as yet another warning of “hidden risks” associated with climate change that threaten the broader banking system, note First Street's researchers, besides hidden spill-over effects to emergency services, community institutions, and labor markets.

Mortgage Lending's Climate Blind Spot

Small and community banks, given their “limited service areas and presumed local mortgage holdings,” emerge as potential weak points in the broader banking system, the report highlights. “Their vulnerability is twofold: a higher percentage of properties at risk in any given scenario year, and a larger proportion of total asset value composed of uninsured net damages.”

Get the NMP Daily

Essential stories, every weekday.

Twenty-five percent (25%) of large banks, 22% of regional banks, 29% of small banks, and 32% of community banks had net damage ratios that surpassed the materiality threshold. Variable reporting and oversight requirements for large and small banks contribute to the opacity surrounding these risk-laced portfolios.

“Many smaller banks lack the financial and technical resources necessary to conduct comprehensive climate scenario analyses," the researchers continue, "which are historically complex and data-intensive processes. Simultaneously, current regulatory frameworks do not mandate such assessments for these institutions, creating a significant gap in climate risk oversight.”

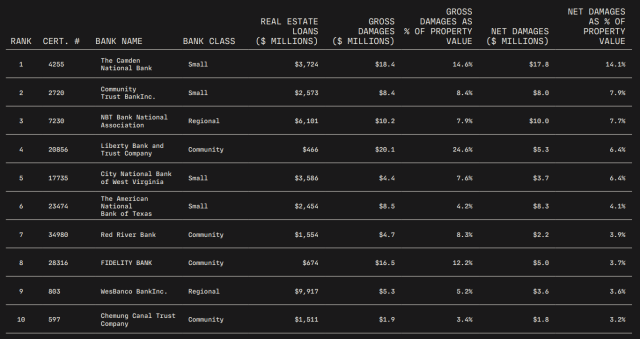

The table below shows the top-10 banks by net damage ratio in the 1% annual likelihood scenario; 80% are small or community banks, highlighting the disproportionate vulnerability of smaller banks.

Source: First Street Foundation

At the 5% annual likelihood — a threshold five times higher than federal regulators' — about 20% of community and small bank branches are exposed to damaging climate events. This share rises to around 35% at the 0.05% annual likelihood, and tops out at over 50% at the 0.2% annual likelihood.

Regional banks show a similar degree of vulnerability, with roughly 20% of branches having risk at the 5% annual likelihood, “but their exposure levels off and tops out at just above 40% of branches with exposure to damage at the 0.2% annual likelihood.” The most distributed portfolio includes branches of large banks, with about 15% of branches with risk at the 5% annual likelihood, topping out at around 30% in the 0.2% annual likelihood.

The Expanding Reach Of Climate Exposure

First Street’s report details how the geographic reach of climate exposure has expanded across the U.S., causing more states to have increased annual exposure to multiple billion-dollar events. This trend illustrates how the compounding impacts of climate change have not only worsened in high-risk localities, but across the entire U.S.

The increasing frequency and severity of disasters have outpaced historical trends, making past data less reliable for predicting future losses. Whatever climate-related financial risks have lain dormant in banks’ portfolios, accumulated when extreme weather occurred less frequently and ferociously, now poses material and systemic risks to these institutions.

An average of 12 states experienced three or more billion-dollar disasters per year from 2009 to 2013. That average expanded to roughly 30 states from 2019 to 2023. The number of states with more than one billion-dollar disaster per year has grown from less than half to nearly all 50 states from 1980 to 2023. Related insurance impacts have been widely experienced in the U.S.

Not surprisingly, while the portfolios of large banks ($100 billion or more in total assets) benefit from scale and geographic diversification, mid-size banks and smaller with less than $100 billion in total assets “may be most vulnerable in terms of their relative climate risk due to their concentrated nature,” the report reads.

Banked Portfolio Climate Risk: $627 Billion

To quantify the risk held by various-sized banks, First Street analysts assumed that the branch locations of a sample of 356 unique banks across the country were representative of their mortgage lending footprint, thus allowing the banks to stand for their distinct “bank portfolios.”

For inclusion, each bank in the sample needed at least 20 branches, and had a majority of its lending footprint in the U.S., resulting in a total sample size of nearly 20,000 branches. Within First Street’s sample, climate exposure accounts for $2.4 billion in gross damages, or nearly 1.5% of the total portfolio value of the nearly 20,000 bank branches.

Of that $2.4 billion in gross damages, $1.1 billion was estimated to be uninsured, accounting for an average of 0.7% of the total portfolio value. Those banks facing the greatest concentration of risk relative to their portfolio size were regional and community banks, not larger institutions.

“Alarmingly,” the researchers write, “30% of the 191 banks (57) had risk that would approach the federal government’s definition of ‘material’ with damages being over 1% of the property value of the bank portfolios. These 57 banks represented a total of $627.4 [billion] in outstanding real estate loans across both commercial real estate (CRE) and residential real estate (RRE).”

Fannie Mae and Freddie Mac will eliminate abbreviated project reviews for condo applications dated on or after Aug. 3

Mortgage lenders have just over a week before Fannie Mae and Freddie Mac retire the abbreviated project-review pathways that have helped qualifying condominium loans avoid the cost and documentation demands of a Full Review.For loan applications dated on or after Aug. 3, Fan...

The retail lender is pairing Spanish-language operations with an ITIN program offering financing up to 85% LTV

Movement Mortgage has launched a centralized bilingual support team designed to help its retail loan officers serve Spanish-speaking borrowers, including originators who do not speak Spanish themselves.The Diverse Lending Support Team will provide bilingual LO assistants and...

J.D. Power finds better digital service, fee transparency, and issue resolution are strengthening trust while homeowners face mounting financial pressure

Contract signings fell 5.4% from May as elevated borrowing costs and record home prices continued to pressure affordability, particularly for first-time buyers