Fannie Mae lowered its 2025 originations forecast by 2.5%, and total home sales forecast by 2.25%, this week.

Economists, analysts, and researchers at the government-sponsored enterprise (GSE), Fannie Mae, reinforced their beliefs that affordability and lock-in effects remain the titular challenges for the mortgage industry in 2025, with any hope of housing recovery hampered by long-term rates expected to remain elevated due to broader economic momentum and rising Treasury yields.

"With a higher expected outlook for mortgage rates, both the lock-in effect and affordability constraints are expected to be more persistent than predicted in our December forecast," Fannie Mae's economists wrote in a revised forecast for mortgage market activity in 2025 and 2026.

The yields investors are demanding on government-backed debt have risen to 52-week highs, and those returns are a reflection of “real yields,” the revised forecast reads, not expectations that inflation may rapidly reaccelerate, as measured by the spread between 10-year Treasury yields and the 10-year Treasury Inflation-Protected Securities (TIPS) spread.

The implication, they explain, is that “bond markets still expect the Fed’s 2-percent inflation target to be achieved, and on a similar timeframe as before. However, the expected path for the fed funds rate going forward, required to achieve that goal, is now higher than previously expected after observing economic activity not slowing by as much as previously expected.”

The insights, along with updated projections for mortgage rates, home sales, and housing inventory, were published in the Fannie Mae Economic & Strategic Research (ESR) Group’s January 2025 commentary, released Wednesday.

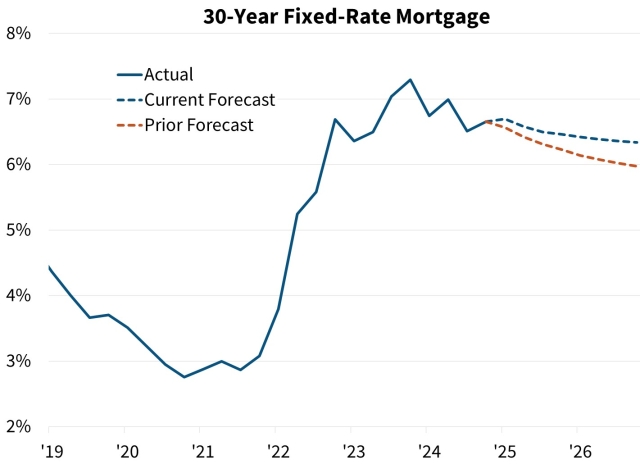

Fannie Mae's ESR Group raised its 2025 mortgage rate forecast.

Source: Fannie Mae

Accordingly, the ESR Group trimmed its 2025 total home sales forecast to 4.89 million (down 2.2% from 5 million) — “the continuation of a sales pace close to the 30-year low” — and its 2026 total home sales forecast to 5.25 million (down 4% from 5.47 million). The group calls their downward revisions for total home sales “comparatively modest due to our view that a large share of transactions is currently being executed by less interest rate-sensitive parties, such as cash buyers or those driven by major life events.”

The group reaffirmed its prior forecast of decelerating home price growth over 2025 and 2026. The combination of higher-for-longer financing costs and lower sales volumes led the ESR Group to lower its single-family mortgage originations forecast to $1.92 trillion in 2025 (down 2.5% from $1.97 trillion), and $2.27 trillion in 2026 (down 4.2% from $2.37 trillion).

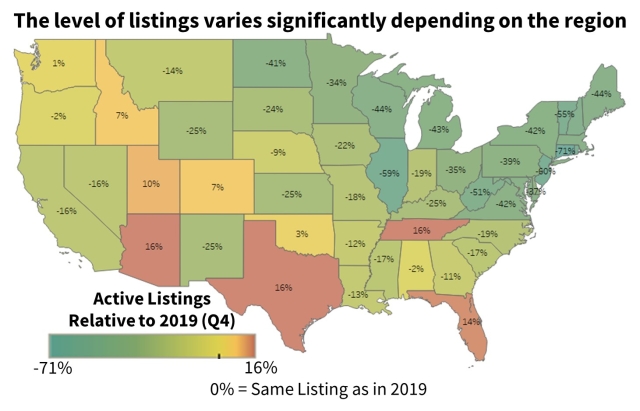

Where the majority of those originations will occur is highly dependent on regional inventory increases that occurred over the course of 2024. Available inventory rose roughly 30% since the end of 2023, according to Realtor.com, but remains 19% below 2019 levels. Where inventory has increased the most, home price gains have slowed most rapidly.

Source: Fannie Mae

Multiple reports published recently indicate that substantial, regional gains in for-sale listings is being driven by homes taking longer to sell, with particularly slow sales paces in southern states like Florida and Texas where new-home construction has accelerated in recent years.

“We interpret this to mean that in some regions, the pool of potential buyers on the sidelines has shrunk and there is not sufficient purchase demand from first-time buyers, in particular, at current prices and mortgage rates,” the ESR Group wrote. “Most regions in the Northeast and Midwest have experienced little improvement in the number of homes available for sale, in part due to a lower infusion of new homes into the housing stock.”

In regions where inventory has increased disproportionately, sales volumes are expected to rise disproportionately and “likely disproportionately contribute to the deceleration in home price appreciation,” the group added.

Affordability pressures may ease as median households incomes grow more rapidly than home prices in 2025 and 2026, though myriad factors are contributing to ongoing pressures on borrowers and prospective buyers. Reaching the highest levels since 2014, Intercontinental Exchange, Inc. (ICE) reported recently that taxes and insurance now comprise one-third of the typical mortgage payment on a single-family property.

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro