As lock-in effects persist, an era of concentrated demand among first-time homebuyers overlaps with an era of increasing unaffordability.

As pent-up purchase demand continues to grow on the sidelines of the nation’s grid-locked housing market, a bottleneck of first-time homebuyers (FTHBs) is swelling.

However, a lack of affordable entry-level homes and exceptionally difficult economic conditions for this cohort of shoppers will likely present persistent barriers to lenders accessing this demand — even as FTHBs comprise an ever-larger slice of the home-purchase pie.

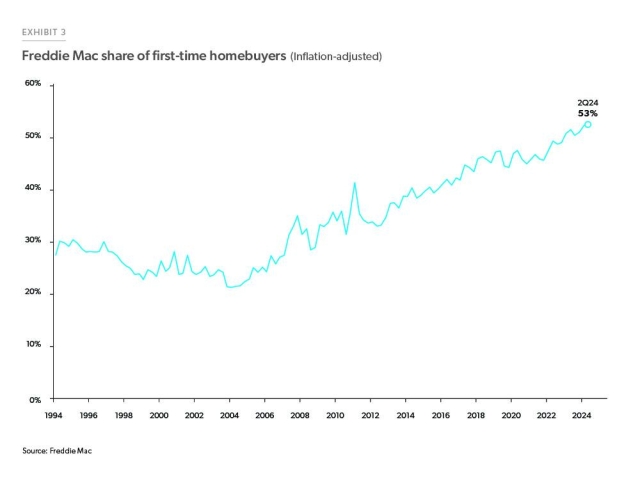

In 2004, FTHBs accounted for roughly one-fifth of Freddie Mac-funded home purchases. In the second quarter of 2024, they accounted for more than half (53%), according to the government-sponsored enterprise’s (GSE) Economic, Housing, and Mortgage Market Outlook for Oct. 2024. Authored by the agency’s Economic & Housing Research group, the report spotlights how FTHBs comprised 40% or more of the quarterly share of home purchases since 2016.

An era of concentrated demand among first-time homebuyers overlaps with an era of increasingly unaffordable homeownership costs.

The role of FTHBs in the purchase market matters to industry stakeholders because they represent “one of the few sources of growing housing demand in the current environment,” the report reads. A recent survey conducted by Maxwell, a business intelligence and technology provider for small and mid-size mortgage lenders, revealed that more than half (54%) of sidelined homebuyers have been searching for a house to buy for more than a year, with almost 18% looking for at least two years.

Luckily for lenders and originators, of these sidelined homebuyers, 40% have not connected with a mortgage lender, presenting an opportunity to connect with these hopeful buyers.

Get the NMP Daily

Essential stories, every weekday.

One explanation for FTHBs’ increased share over the past few years is that repeat buyers are less active in the market due to the mortgage lock-in effect. With Federal Housing Finance Agency (FHFA) researchers warning that home sales lost to lock-in effects will compound for years, the affordability challenges preventing many FTHBs from entering the market present an outsized challenge for mortgage lenders who have little power to change those market factors.

“If rates begin to decline pretty substantially even, we’re still going to see it around for another five to 10 years at minimum,” says Will Doerner, a supervisory economist in the FHFA’s Division of Research and Statistics. Michael Seiler, a professor at the College of William and Mary and a visiting scholar at the FHFA, adds, “It’s not like this rate delta, the difference between the rate on your mortgage and current rates, occurred 20 years ago. This occurred very recently.”

The Mortgage Bankers Association (MBA) has forecasted a $2.3 trillion market for all residential mortgage originations in 2025, with $1.5 trillion of purchase volume. Evidently, Fannie Mae peered into the same crystal ball, forecasting $2.2 trillion in 2025 originations, also with $1.5 trillion in purchase volume. This year is projected to end with roughly $1.3 trillion in purchases.

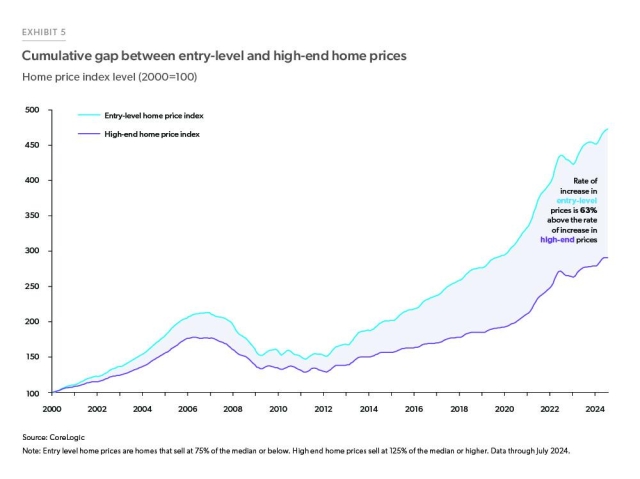

From January 2000 to July 2024, cumulative entry-level prices grew 63% more than high-end home prices.

With millennials now of prime home-buying age and Gen Z’s oldest members entering the workforce, this era of concentrated and growing demand among FTHBs overlaps with an era of increasingly unaffordable prices for entry-level homes. From January 2000 to July 2024, cumulative entry-level prices grew 63% more than high-end home prices, per Freddie Mac.

Meanwhile, mortgage rate relief proving more elusive than many would like, coupled with rising insurance costs makes qualifying FTHBs a significant challenge — even though young-adult renters are earning more money now than in prior years and even after adjusting for inflation. Since 2012, the pool of potential FTHBs has risen substantially, and as of 2023, there were more than three million of such renter households.

However, significant rent increases since the outset of the COVID-19 pandemic, compounded by increased cost of living expenses and higher unemployment rates among renters, have hindered their flexibility to squirrel away savings for a down payment and closing costs. In response, the number of down payment assistance (DPA) programs that exist to help bridge that affordability gap has continued to grow, hitting 2,444 programs across the U.S. in the third quarter of 2024.

These generally more difficult economic conditions for FTHBs are a headwind facing the entire industry, with a survey of 1,818 U.S. adults by Mphasis Digital Risk, a mortgage and financial services company, revealing that half of prospective homebuyers cannot afford basic home costs.

Of course, FTHB demand is not pooling equally, everywhere. Overall, Freddie Mac shows that from 2019-2024, the FTHB share of Freddie Mac-funded loans has increased consistently across the U.S., with higher rates of FTHB share in the Midwest and Northeast.

Fannie Mae and Freddie Mac will eliminate abbreviated project reviews for condo applications dated on or after Aug. 3

Mortgage lenders have just over a week before Fannie Mae and Freddie Mac retire the abbreviated project-review pathways that have helped qualifying condominium loans avoid the cost and documentation demands of a Full Review.For loan applications dated on or after Aug. 3, Fan...

The retail lender is pairing Spanish-language operations with an ITIN program offering financing up to 85% LTV

Movement Mortgage has launched a centralized bilingual support team designed to help its retail loan officers serve Spanish-speaking borrowers, including originators who do not speak Spanish themselves.The Diverse Lending Support Team will provide bilingual LO assistants and...

J.D. Power finds better digital service, fee transparency, and issue resolution are strengthening trust while homeowners face mounting financial pressure

Contract signings fell 5.4% from May as elevated borrowing costs and record home prices continued to pressure affordability, particularly for first-time buyers