Consumer credit remained on solid footing in May, with borrowers continuing to keep delinquency rates below pre-pandemic levels even as higher interest rates and affordability pressures persist, according to the latest CreditGauge report from VantageScore.

The report found that the average VantageScore 4.0 credit score held steady at 701 in May, while delinquency rates improved across every major credit tier. The data suggests consumers have largely adapted to a prolonged higher-rate environment despite rising household expenses and the return of student loan payments.

"While consumer sentiment has softened in recent months, the underlying credit data tells a more stable story," said Atif Mirza, executive vice president and chief digital and insights officer at VantageScore. "Delinquency rates remain below pre-pandemic levels across all delinquency stages, reflecting the continued resilience of consumers despite elevated interest rates and rising household expenses. Coupled with a rebound in new credit originations, these credit trends point to a credit market that remains healthy and accessible."

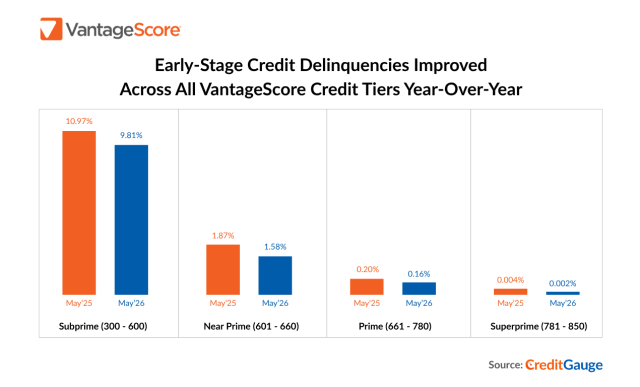

Year over year, early-stage (30-59 days past due) delinquency rates declined across all VantageScore credit tiers. Prime borrower delinquencies fell from 0.20% to 0.16%, while Nearprime borrower delinquencies fell from 1.87% to 1.58%. Among Subprime borrowers, delinquencies declined from 11.0% to 9.8%, while Superprime borrowers maintained an exceptionally low delinquency rate of 0.0020%, down from 0.0040% a year earlier.

The report says those improvements came despite ongoing affordability challenges, elevated borrowing costs, and resumed student loan payments.

One of the report's more notable findings was renewed growth in unsecured lending. Originations across most credit products remained above year-earlier levels, led by personal loans. Personal loan originations reached a nine-month high, rising from 2.88% in October 2025 to 3.41% in May 2026, a trend VantageScore said will be worth monitoring in the months ahead.

The combination of stable credit scores, improving payment performance, and increased borrowing activity points to a consumer credit market that has remained resilient despite continued economic headwinds.

The findings come as the mortgage industry continues preparing for broader adoption of VantageScore 4.0 following the Federal Housing Finance Agency's approval of the model for use by Fannie Mae and Freddie Mac. The monthly CreditGauge report provides one of the industry's regular snapshots of consumer credit conditions as lenders monitor borrower performance in a higher-rate environment.