Credit-scoring company, VantageScore, released its CreditGauge for September 2024, which found that credit delinquencies are rising across products while the days past due (DPD) continue to mount and the percentage of consumers with newly opened credit accounts declines.

CreditGauge, a monthly analysis highlighting the overall health of U.S. consumer credit, shows the average VantageScore 4.0 credit score increased slightly but held at 702 for the seventh month in a row. Overall, the lowest VantageScore 4.0 credit score is 300, while the highest score is 850.

“September's CreditGauge provides the final snapshot of consumer credit health before the U.S. elections, revealing that many consumers are putting their new borrowing on pause,” said Susan Fahy, executive vice president and chief digital officer at VantageScore. “The slow down in new lending and borrowing is notable given that the Federal Reserve cut interest rates in September in an effort to stimulate access to new credit for consumers and corporations.”

The main finding from the September 2024 report was that credit delinquencies increased broadly with late payments across all days past due (DPD) categories rising over last year, except for those who are 90 to 119 DPD compared to August 2024. Early-stage (30 to 59 DPD) credit delinquencies increased sharply by 0.13% from last month, the second largest monthly gain in 2024. Late-stage payments for mortgages rose the most from last year by 0.05%, followed by credit cards, which increased by 0.04%. Credit delinquency rates also rose across all VantageScore credit tiers year-over-year.

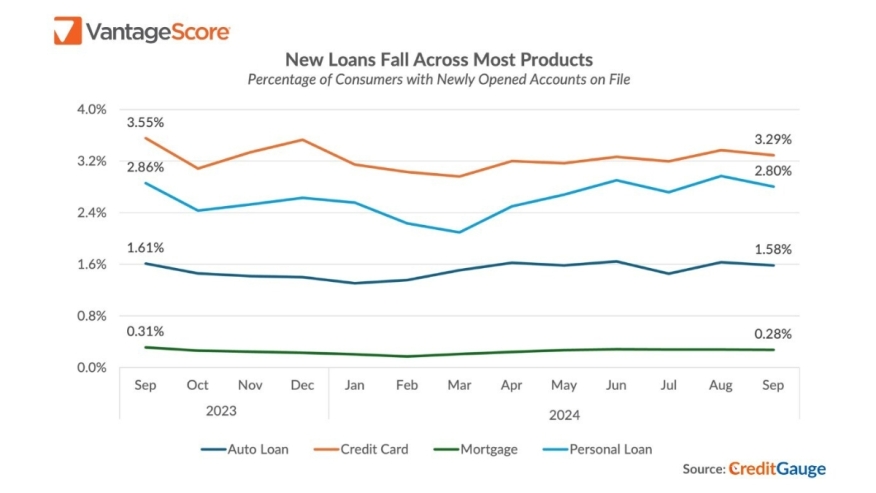

The percentage of consumers with a new loan declined from last year, as newly opened credit accounts fell across all products. Compared to last month, new accounts slowed for all credit products, except for mortgages. New credit card accounts fell the most among all products, down 0.26% from September 2023, reflecting lower demand for loans among consumers and an increased perception of risk among lenders.

Additionally, overall balances hit a CreditGauge record-high for the third consecutive month this past September. Overall average credit balances rose by $2,206 (+2.1%) from last year and by $163 (+0.16%) from the month prior. The amount of available credit that borrowers used (the credit utilization rate) fell slightly, showing consumers maintained steady credit usage relative to their loan amounts as historically high interest rates increased loan balances.