CoreLogic determines how many loans would be ripe for a refi if rates drop again

KEY TAKEAWAYS

46.2% of the loans in the servicing sample are “refinance burnouts”

Nearly half (46.1%) of the loans in this sample are "locked-in" to ultra-low rates

Only 7.7% of loans in the sample are candidates for a lower rate refinance if rates drop to or below 6%

As mortgage rates tick down and expectations rise for multiple rate cuts by the end of 2024, lenders and originators have begun preparing for another refinance wave. After reviewing 15.7 million first-lien mortgages currently in servicing, CoreLogic discovered an overwhelming majority of U.S. household mortgages are either locked into a low-rate mortgage or “refinance burnouts.”

As of mid-August, 30-year-fixed mortgage rates eased slightly from their peak in the mid-7% range to the mid-6% range, prompting many homeowners who borrowed at interest rate heights to consider refinancing for lower mortgage payments. According to the Mortgage Bankers Association (MBA), refinance applications in August 2024 more than doubled from last year.

Still, lenders and mortgage professionals want to know how many homeowners are likely to find meaningful reductions in their monthly mortgage payments by refinancing to rates in the lower 6% range.

CoreLogic estimates 4 million loans were originated during the period of high interest rates 2023-24.

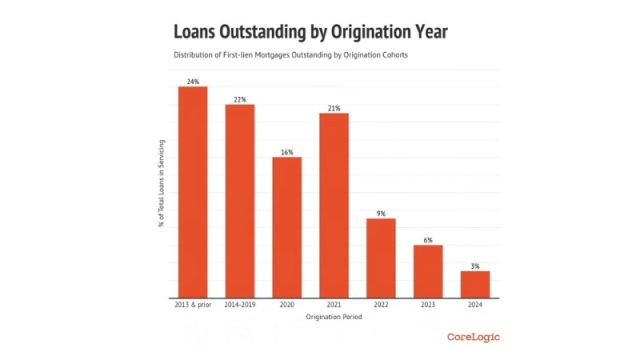

Broken down by year, 46.2% of the loans reviewed in CoreLogic's servicing sample were originated before the 2020 pandemic, making them more seasoned loans. Twenty four percent (24%) of those loans were originated in 2013 or prior, and 22.2% of loans were originated between 2014 and 2019. Because those are seasoned loans that have had plenty of opportunities for a lower rate refinance, CoreLogic calls them “refinance burnouts.”

Nearly half (46.1%) of the loans in this sample portfolio were originated between 2020 and 2022, when interest rates were at record lows. These loans are “locked-in” to their existing low and ultra-low rates.

Get the NMP Daily

Essential stories, every weekday.

Loans originated in 2023 and 2024 comprise just 7.7% of the 15.7 million loans in servicing that CoreLogic analyzed. Many of those loans are deemed already “in the money” candidates for a lower rate refinance, or will be among the first in line to apply for refinancing should interest rates drop to (or below) 6%.

As of June 2024, an estimated 4 million outstanding loans were originated during the period of high interest rates in 2023 and 2024. The total outstanding loan volume was estimated to be 51.97 million, with an average loan balance of $240,900. High-rate loans represent an estimated $1.452 trillion in outstanding unpaid mortgage balances, originated during the high interest rate period of 2023-2024.

However, with more than $12 trillion of total outstanding U.S. mortgage debt, even a small percentage of “in-the-money” loan balances can amount to hundreds of billions of dollars of originations for lenders. Average loan sizes for those with an interest rate of 6.75-7.5%, or at or above 7.5%, are $265,000 and $196,000, respectively.

As of June 2024, an estimated $579 billion in loan balances are carrying an interest rate in the 6.75% to 7.5% range, and an additional $157 billion in loan balances are at or above 7.5%. This results in a combined total of $735 billion in loans that could benefit from a refinance if rates drop further to near or below 6%, CoreLogic reports.

The technology veteran will oversee product execution, platform development, engineering, infrastructure, and cloud strategy

Informative Research (IR) has promoted Ajay Trilokeshwaran to chief technology officer, placing the longtime enterprise technology leader in charge of the company’s product and technology execution.Trilokeshwaran will oversee platform development, application engineering, in...

From buy-before-you-sell strategies to hoodies, Chick-fil-A, and AI agents, three producers revealed what is actually generating purchase business in 2026

The loan originators winning purchase business in 2026 are not waiting for the Federal Reserve to hand them a better market.They are finding homeowners who feel trapped by low mortgage rates, solving financing problems that keep offers from competing, and building relationsh...

Contract signings fell 5.4% from May as elevated borrowing costs and record home prices continued to pressure affordability, particularly for first-time buyers

A $432.4 million deal backed by over 1,000 loans shows investors are still hungry for Non-QM paper — but the real story is where the loans are coming from