A new report from Realtor.com finds that four years of elevated mortgage rates have fundamentally reshaped the U.S. housing market, creating persistent affordability challenges, and a market defined by uneven supply and resilient prices.

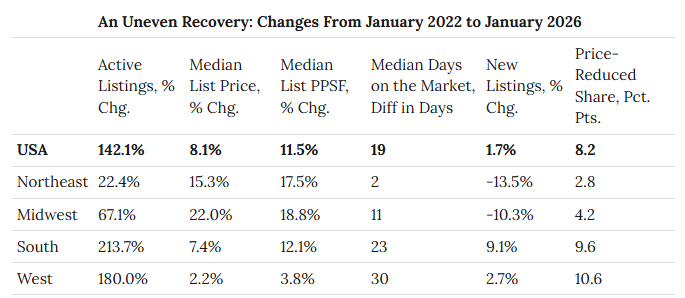

Since mortgage rates began rising in early 2022 — peaking near 7.79% and currently hovering around the 6% mark — active inventory has climbed 142.1% nationally, rebounding sharply from pandemic-era lows.

However, despite this dramatic increase in listings and higher borrowing costs designed to cool demand, home prices have continued to rise rather than fall. The national median list price grew 8.1% over the past four years, and price per square foot increased 11.4%, illustrating the unusual resilience of home values even amid tighter affordability.

Where Do We Stand?

Realtor.com Senior Economist Jake Krimmel described the market as having “recalibrated rather than reset,” noting that standard economic forces of supply and demand have not produced the broad price relief many expected.

"Four years into this higher-rate environment, it's clear that the housing market recalibrated rather than reset," said Krimmel. "Supply and demand moved in the directions economic theory would suggest, but prices proved far more resilient than many anticipated, leaving today's affordability challenges firmly in place. Looking forward, the real test is whether market activity can normalize without reigniting price pressure. That will depend on easing lock-in, stronger new listing growth, and fewer delistings."

Finding Normalization In Today’s Rate Market

A key driver of this dynamic is the “lock-in effect,” where a large share of homeowners retain historically low mortgage rates, discouraging them from selling and reducing available supply. Realtor.com data shows a substantial majority of outstanding mortgages carry rates well below current levels, limiting sellers’ willingness to list.

Measuring The Regional Impact Of Housing Inventory

The inventory recovery also displays sharp regional differences. Listings in Western and Southern metros have surged — in some markets by more than 350% — while growth in the Northeast and Midwest has been far more muted. Some major metros, including Chicago and New York, now have fewer active listings than they did four years ago.

What Lies Beyond For The Marketplace?

Looking ahead, Realtor.com suggests that potential rate declines could lessen the lock-in effect and bring more supply to market. However, lower rates might also spur renewed buyer demand, potentially limiting meaningful gains in affordability. The report underscores that sustainable improvement in affordability will likely depend on stronger, long-term supply growth rather than short-term shifts in borrowing costs.

"That's the tension in today's market," Krimmel said. "Lower rates could unlock more supply, but they could also bring buyers back faster than listings recover. The path to meaningful affordability relief depends on supply growing sustainably — not just demand returning. Lock-in removed a lot of discretionary buyers from the market, leaving a lot of people moving out of necessity who were less price sensitive. As those buyers eventually return and list their own home too, that will add some much needed liquidity to the market."