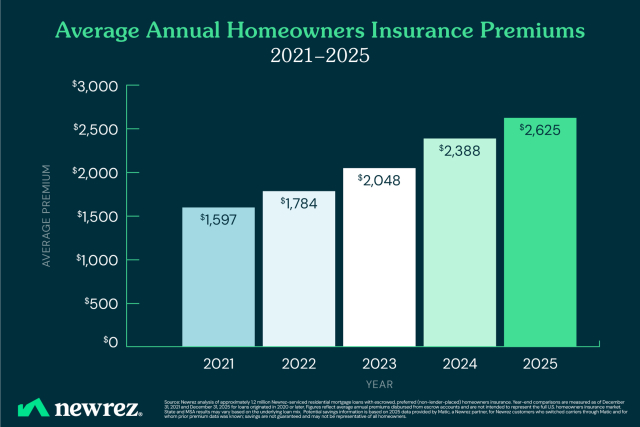

Homeowners insurance premiums have surged 64% since 2021, pushing the national average above $2,600 annually, according to a new analysis from Newrez — a cost shock that is increasingly showing up in escrow payments and tightening borrower affordability, even as the pace of increases begins to cool.

The study, based on roughly 1.2 million Newrez-serviced mortgages, found average annual premiums climbed from $1,597 at year-end 2021 to $2,625 by the end of 2025. Growth slowed to 10% in 2025, the lowest annual increase since 2021, signaling some moderation after multiple years of double-digit gains.

For mortgage professionals, the data underscores a growing pressure point: rising insurance costs are increasingly flowing through escrow accounts and into monthly payments, in some cases offsetting rate relief and complicating qualification.

Because homeowners insurance is typically paid through escrow accounts, increases in premiums can directly raise a borrower’s monthly mortgage payment. Along with property taxes, insurance costs are one of the primary drivers of escrow payment adjustments.

Costs Rise, But Borrowers Still Performing

Despite the sharp increase in premiums, borrower performance remains stable, at least for now.

Newrez found overall mortgage delinquencies are still below historical averages, even as insurance and other housing costs rise.

At the same time, home values increased by roughly $50,000 between 2021 and 2025, according to Zillow data cited in the report, helping support borrower equity positions.

That combination points to resilience, but also a narrowing margin.

“Homeowners insurance has become a much larger component of housing costs for many homeowners since 2021, as more frequent severe weather events and higher rebuilding costs are putting pressure on insurers,” said Shane Ross, head of servicing at Newrez.

For LOs, the takeaway is straightforward: borrowers may still be performing, but higher fixed costs are eating into affordability buffers.

Geography Is Driving Payment Shock

Insurance costs are not rising evenly, and in some markets, they are becoming a primary affordability constraint.

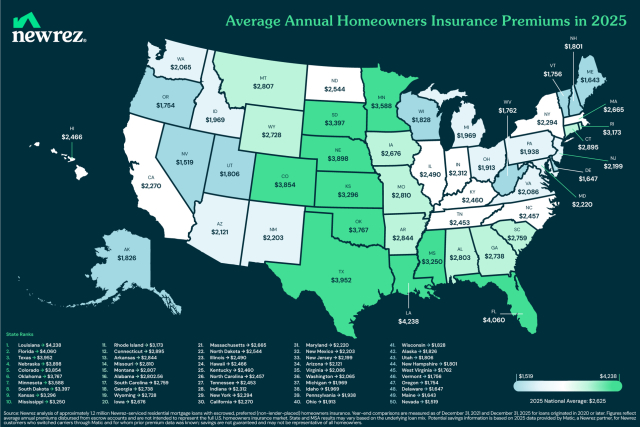

At year-end 2025, Louisiana recorded the highest average annual premium at $4,238, followed by Florida ($4,060) and Texas ($3,952).

Meanwhile, Arizona saw the largest increase from 2021 to 2025, with premiums jumping 94%, while Alaska posted the smallest increase at 27%.

At the metro level, Miami led the 20 largest MSAs with an average premium of $5,546, while Seattle came in lowest at $2,087.

Those differences are more than regional trivia. In higher-cost markets, insurance alone can add hundreds of dollars to a borrower’s monthly payment, directly impacting debt-to-income ratios and, in some cases, loan eligibility.

A Lever to Keep Deals Alive

One area where borrowers — and originators — may still have room to maneuver is insurance shopping.

According to 2025 data from insurtech platform Matic, Newrez customers who switched carriers saved an average of $928.

That creates a potential pressure-release valve for deals that are close to qualifying thresholds.

The report also notes that savings may be available through deductible adjustments, bundling policies, or making property improvements that reduce risk exposure.

The Bigger Shift: Payment Over Rate

The broader takeaway for the mortgage industry is structural.

While rate movements continue to dominate headlines, the Newrez data reinforce that insurance, along with taxes, is playing a larger role in determining the true cost of homeownership. Because these expenses are built into escrow and recalculated annually, they can drive payment volatility even after a loan closes.

And while premium growth may be slowing, it is doing so at a significantly higher baseline.

That means even smaller increases can still move the needle on affordability.