Housing affordability nationwide strengthened notably through 2025, with consumer house-buying power increasing about 9.8% year-over-year in November, according to the First American Real House Price Index (RHPI). The rise marks one of the most sustained improvements in recent years, and reflects the combined effects of higher incomes and falling mortgage rates.

After nearly a decade of affordability challenges following the pandemic housing boom, the trend finally turned decidedly positive in 2025. Median household incomes climbed 3.5% year-over-year, supported by broad wage growth, while mortgage rates ended the year significantly lower than a year earlier, boosting purchasing power by a combined $36,600 compared with November 2024.

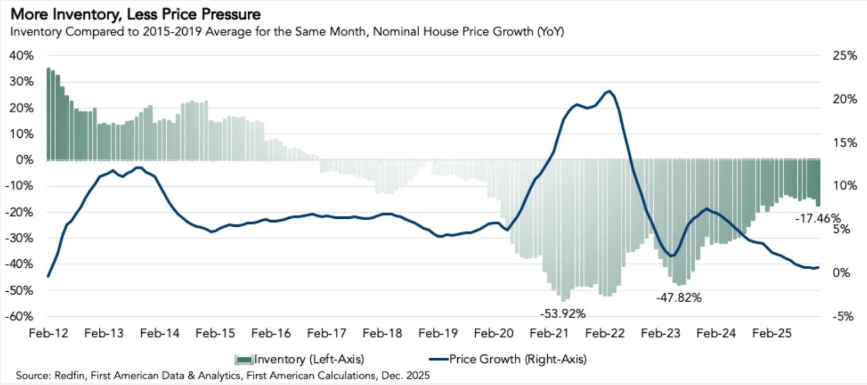

At the same time, nominal U.S. house price growth has largely stalled, rising only about 0.5% annually — the slowest pace since 2012. Because income gains are outpacing home prices, the affordability gap has continued to shrink. Forty-seven of 50 major metropolitan areas (MSAs) tracked by First American registered year-over-year affordability improvements, underscoring that gains are broad rather than regionally confined.

“In November, the labor market continued to provide critical support for housing affordability," noted First American Chief Economist Mark Fleming. "Annual private-sector hourly wage growth increased 3.6% compared with a year earlier, boosting median household income by 3.5% year-over-year. Just that income growth alone increased house-buying power by roughly $13,100.

Mortgage rates fueled another significant boost. Rates were 0.57 percentage points lower than a year earlier, lifting purchasing power by approximately $23,500. Combined, higher incomes and lower rates mean homebuyers have about $36,600 more house-buying power compared with November 2024.”

Despite these improvements, affordability still remains well below pre-pandemic norms. Consumer buying power is more than 63% below its five-year pre-pandemic average, even as real house prices have declined modestly on an annual basis.

Looking ahead, analysts stress that the key determinant of future affordability will be housing inventory. While labor market momentum and steady mortgage rates are expected to continue supporting buyers, limited supply could reignite price pressures if new listings lag behind demand. Pandemic-era scarcity saw inventory levels plunge more than 50% below historical norms, helping fuel rapid price acceleration.

Industry economists also point to renewed market engagement due to life events that could bring more sellers to market in 2026, potentially easing tight supply and reinforcing affordability improvements.

"Life events — job changes, household formation, and relocation — will continue to draw both buyers and sellers off the sidelines in 2026," added Fleming. "That gradual life-event re-engagement should support more inventory and more sales transactions. As long as inventory levels don’t deteriorate dramatically because more buyers than sellers enter the market, house price growth will remain in check, allowing affordability to continue to steadily improve.”