Loan volumes fell, median monthly incomes rose, and alternative loan products increased market share in the second quarter's minimally affordable, sluggish home buying season, according to new data published by Maxwell, a mortgage advisory and technology solutions provider serving small and mid-size lenders.

The Q2 2024 Mortgage Lending Report was derived from more than $360 billion in loan volume transacted on the Maxwell Business Intelligence Platform by more than 300 lenders.

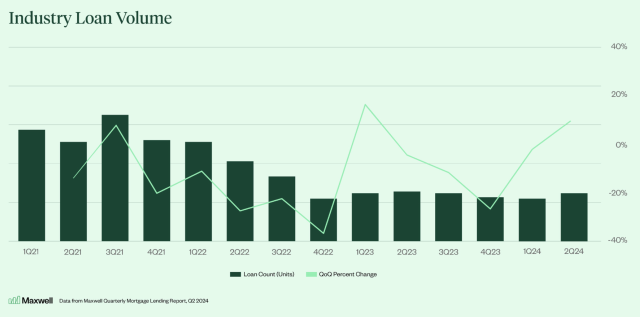

Year-over-year loan volume (units) fell in the second quarter by 4%, Maxwell found, as mortgage rates remained elevated around 7.2% — 0.2% higher on average than the first quarter and 0.5% higher than the second quarter of 2023. Despite persistently low affordability for homebuyers, however, loan volumes jumped 21% from the first quarter to the second quarter.

Home equity lines of credit (HELOCs) experienced a particularly strong quarter, driving volume for lenders, Maxwell says. The share of HELOCs rose 31% quarterly and 61% year over year to comprise 3.88% of the second-quarter market.

As affordability challenges constrained buyers’ budgets, the share of low-money-down FHA loans also rose in the second quarter, up 3% quarterly to comprise 33% of all originations, (a 1% decrease year over year). The share of VA loans rose 4% quarterly and 0.5% annually to comprise nearly 12% of the market in the second quarter.

“The ongoing popularity of alternative loan types — especially HELOCs and FHA loans — isn’t surprising given the sustained high-interest-rate environment,” commented John Paasonen, Maxwell’s co-founder and CEO. “It’s possible that the share of these products will decrease as interest rates drop, but with ongoing housing affordability issues and historically high home equity, I could see them sustaining for the long-term.”

Meanwhile, borrowers’ attributes fluctuated less in the second quarter than the loan products they sought. The median credit score was 757, up from 756 in the first quarter. The median loan-to-value (LTV) ratio was 80, matching the first quarter. The median debt-to-income ratio was 40, matching the first quarter, but 2% higher year over year.

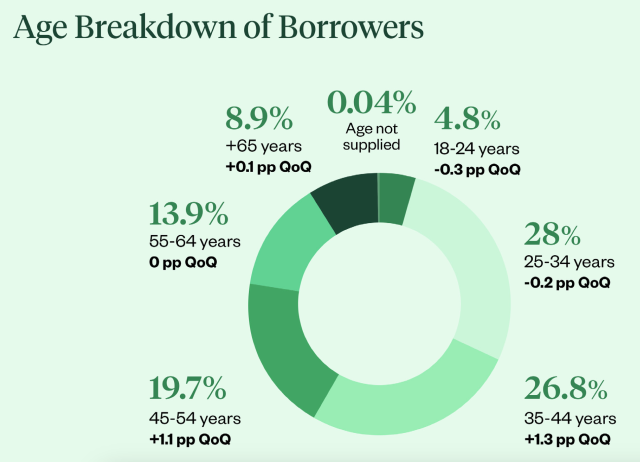

The average age of borrowers rose from 43 to 44 quarterly, reflecting the realities of a market pricing out younger buyers. Purchase volume among all ages groups 34 and below declined in the second quarter, while age groups 35 and above saw their share of the market increase.

Affordability also impacted homeownership rates along racial lines in the second quarter.

Maxwell’s report indicates that Black or African American borrowers saw their homeownership rate decline by 0.3% compared to the first quarter of 2024, Asian borrowers by 0.4%, and American Indian or Alaska Native borrowers by 0.1%. White borrowers increased their homeownership rate by 0.7% from the first quarter and multi-racial borrowers by 0.1%. Native Hawaiian or Other Pacific Islander borrowers saw no change in homeownership rates quarterly.

For all home buyers, the median loan amount increased 3% in the second quarter compared to the overall average, reaching $307,000. The median loan amount for first-time home buyers (FTHB) was $289,000. Quarterly, the median loan amount increased 3% for the general market and 2% for FTHBs. Annually, the median loan amount increased 6% for the general market and 5% for FTHBs.

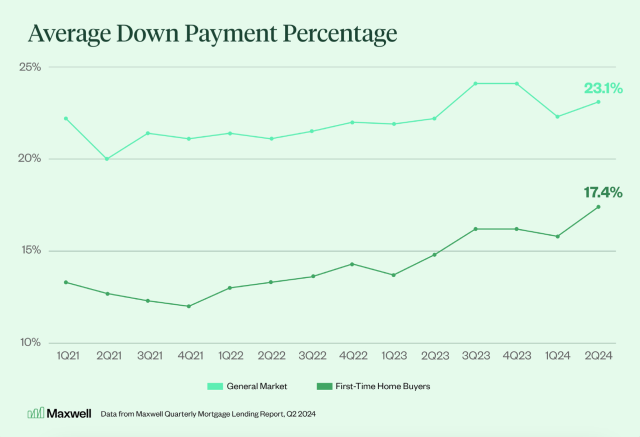

For both FTHBs and the overall market, median loan amounts reached all-time highs in the second quarter. And, as loan amounts increased, so did down payments.

The average amount home buyers put down to purchase a home in the second quarter was 25%. FTHBs put down an average of 16%. Overall home buyer down payment percentages increased 3% quarterly and 7% annually, while FTHB down payment percentages rose 8% quarterly and 20% annually.

The second quarter also saw home buyers’ median monthly incomes rise to record-high levels, with all borrowers averaging $8,000 of monthly income, an increase of 3% quarterly and 9% annually. FTHBs averaged $6,000 of monthly income, up 2% quarterly and 9% annually.

Median monthly income is a metric that has been increasing steadily in recent years, Maxwell’s report indicates, up 12% for the overall market and 11% for FTHBs since 2021.