New data published by the Federal Reserve Bank of New York paints a bleak picture of mortgage origination in 2024, as consumers’ expectations of improving credit conditions remain subdued heading into next year.

The average rejection rate for mortgage refinance applications increased to a decade-plus high of 25.6% this year, a jump from 15.5% last year. Meanwhile, rejections for overall mortgage applications rose to 22.6% in Oct., up from 13% in Oct. 2023 and 17.4% in Oct. 2022.

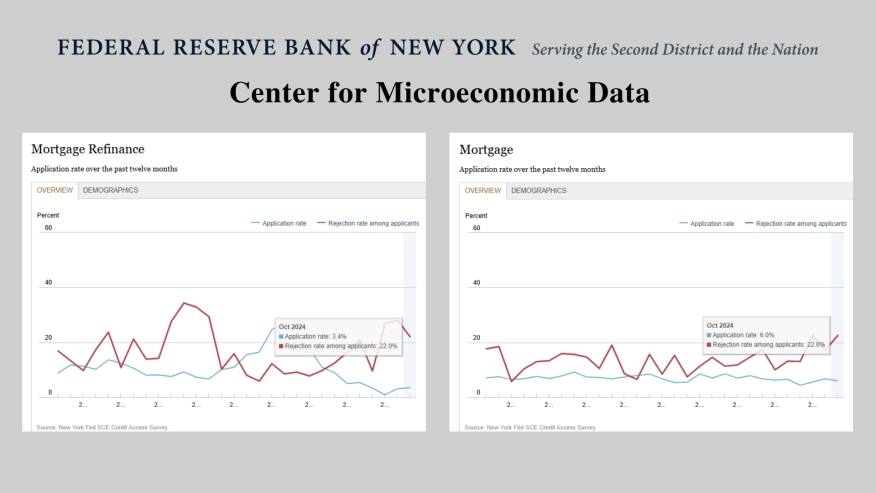

Rejections for mortgage refinance applications hit 22% in Oct. 2024, compared to 9.5% in Oct. 2023 and 12.4% in Oct. 2022.

Conducted and published by the New York Fed’s Center for Microeconomic Data, the Survey of Consumer Expectations (SCE) Credit Access Survey is fielded every four months and gauges consumers’ experiences with, and expectations about, various kinds of credit demand and credit access. The data series began in 2013.

The latest SCE Credit Access Survey reveals largely stable credit demand but increased rejection rates on credit applications in 2024, while providing an early glimpse at 2024’s mortgage market in contrast to 2023.

The application rate for credit cards reached 28.6% in Oct. 2024, slightly below its Oct. 2023 level of 29%, and above pre-pandemic readings of 27.2% in Oct. 2019. The average application rate for credit cards for 2024 overall was 27.8%, 1.8% higher than 2023’s overall rate.

After a horrendous year in 2023 for most mortgage companies, consumers’ average likelihood of applying for a mortgage decreased further in 2024 to 6.4%, from 6.7% in 2023. The average likelihood of applying for a mortgage refinance, meanwhile, rebounded from a series low of 3.5% in Oct. 2023 to 6.1% in Oct. 2024.

For the year overall, the average likelihood of applying for a mortgage refinance increased to 5.9% in 2024 from 4.7% in 2023. The average rejection rate for mortgage applications increased by 8.6 percentage points to 20.7% in 2024, well above the 2019 rate of 10.2%.

Mortgage loan application rates increased to 6% in Oct. 2024 from 4.3% in Oct. 2023. The average rate for 2024 overall was 6.1%, 0.4 percentage point above the 2023 average, but 1.8 percentage points below the 2019 average.

Application rates for mortgage refinancing declined further during 2024, falling to 2.4% in 2024 from 4.5% in 2023, a new series low.

Heading into 2025, U.S. households anticipate they will be less likely to apply for at least one type of credit over the next 12 months, with lower average likelihoods of applying for a new credit card or a mortgage, but higher likelihoods of applying for a mortgage refinance.

Fewer households are applying for auto loans as of Oct. 2024, at a rate of 11.8%, below Oct. 2023’s rate of 13.5% and Oct. 2022’s rate of 12.9%. Auto loan application rates for 2024 declined to 11.2% from 12.7% in 2023 and 13% in 2022.

While the probability of raising $2,000 should an unexpected need arise improved to 66.5% in 2024 from 65.8% in 2023, the average probability of needing $2,000 for an unexpected expense in the next month increased to 36.7% this year, from an average of 33.4% last year.

Consumers also report higher perceived likelihoods of future credit card, auto loan, and mortgage refinance applications being rejected, but lower expected rejection rates for mortgage applications and credit limit increases.