30-year FRM stays essentially flat following seven weeks of downward drift

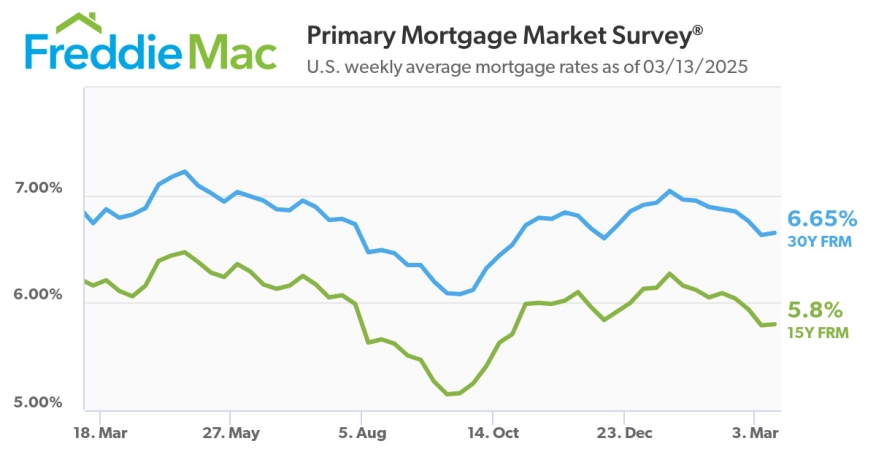

The average 30-year fixed-rate mortgage (FRM) rate rose ever so slightly to 6.65% as of the week ending March 13, an increase from 6.63% the prior week, according to Freddie Mac’s Primary Mortgage Market Survey (PMMS).

Freddie Mac Chief Economist,

Sam Khater

Sam Khater, chief economist at the company, noted the rate declines and growing stability over the last two months are beginning to jog homebuyer activity. The outlook this year is a little rosier: at this same time in 2024, the 30-year FRM averaged 6.74%, or 9 basis points higher.

Notably, from a recent peak of 7.04% on Jan. 16, 2025, the present average 30-year FRM rate is now 39 basis points, or roughly 5.5%, less.

“Despite volatility in the markets, the 30-year fixed-rate mortgage remained essentially flat from last week,” Khater stated in a release. “Mortgage rates continue to be relatively low versus the last few months, and homebuyers have responded.”

“Purchase applications are up 5% as compared to a year ago,” he noted, adding, “The combination of modestly lower mortgage rates and improving inventory is a positive sign for homebuyers in this critical spring homebuying season.”

Get the NMP Daily

Essential stories, every weekday.

For reference, here’s the 30-year FRM’s rate trend going back to late December 2024. Freddie Mac’s survey shows the 30-year FRM rate averaged:

6.65% on March 13, 2025;

6.63% on March 6, 2025;

6.76% on Feb. 27, 2025;

6.85% on Feb. 20, 2025;

6.87% on Feb. 13, 2025;

6.89% on Feb. 6, 2025;

6.95% on Jan. 30, 2025;

6.96% on Jan. 23, 2025;

7.04% on Jan. 16, 2025;

6.93% on Jan. 9, 2025;

6.91% on Jan. 2, 2025;

6.85% on Dec. 26, 2024; and

6.72% on Dec. 19, 2024.

Meanwhile, the 15-year FRM averaged 5.80% for the week ending March 13, just one basis point up from 5.79% a week ago. A year ago at this time, Freddie Mac noted, the 15-year FRM averaged 6.16%.

The 15-year MFR rate averaged:

5.80% on March 13, 2025;

5.79% on March 6, 2025;

5.94% on Feb. 27, 2025;

6.04% on Feb. 20, 2025;

6.09% on Feb. 13, 2025;

6.05% on Feb. 6, 2025;

6.12% on Jan. 30, 2025;

6.16% on Jan. 23, 2025;

6.27% on Jan. 16, 2025;

6.14% on Jan. 9, 2025;

6.13% on Jan. 2, 2025;

6.0% on Dec. 26, 2024; and

5.92% on Dec. 19, 2024.

Freddie Mac notes that the PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20% down and have excellent credit.

National Association of Realtors

Deputy Chief Economist, Dr.

Jessica Lautz

Dr. Jessica Lautz, deputy chief economist and vice president of research at the National Association of Realtors (NAR), calculated that at the current 6.65% rate for a 30-year FRM, if a buyer were to put down 20% on a home priced at $400,000, the monthly mortgage payment would be $2,054. With a 10% down payment, that monthly payment would be $2,311.

For comparison, according to Realtor.com's January 2025 Rent Report, the overall median U.S. rental unit cost just over $1,700/month, down 0.2% from January 2024. Renting the median-priced two-bedroom unit cost $1,887, also down 0.2% from a year ago.

Lautz pointed to some positive signs in the housing market that are concurrent with this latest rate report from Freddie Mac’s PMMS. “Mortgage applications continue to rise, as buyers capitalize on lower rates and increased inventory,” she wrote. And, days on market for homes have grown longer, which gives buyers time to view homes and submit competitive offers.

Also, inflation decreased this week, “possibly making it a bit easier to save for a home,” Lautz noted.

But there are certainly some less positive factors in the market as well. “It’s important to note that inventory is still historically low, so while more homes are available, there is still a considerable way to go,” wrote Lautz. “The typical seller received an average of 2.6 offers last month, so buyers must stay zealous” in their purchasing efforts.

The aggregator has advanced from planning its first securitization and courting capital partners to pursuing one of the largest shares of the growing Non-QM market

Redwood Trust is targeting approximately 10% of the Non-QM market by the end of 2026 or early 2027, accelerating an Aspire expansion plan that has progressed rapidly since the beginning of the year.The company estimates Aspire currently accounts for 5% to 6% of the market on...

The mortgage servicer can initially issue up to 1,000 eNotes and manage digital collateral for other Ginnie Mae issuers

BSI Financial Services has received Ginnie Mae approval to issue and subservice electronic promissory notes, giving mortgage companies another option for managing government-backed loans through a digital process.The Irving, Texas-based mortgage servicer was approved as both...

Truework finds 85% consider refinancing important to their financial health, revealing a highly motivated but financially vulnerable future borrower pool