MBA RIHA updated report notes 'housing supply is being impacted by increased life expectancy'

The Mortgage Bankers Association's (MBA) Research Institute for Housing America (RIHA) released yesterday an update to its somewhat morbid research report, titled “Who Will Buy the Baby Boomers’ Homes When They Leave Them? Population Aging, Mortality, and the Future of the Housing Market.” Those prospective homebuyers who have remained on the sidelines of the housing market due to its hostility the past few years come to mind. However, they may have to bide their time a bit longer given how “supply is being impacted by increased life expectancy,” the MBA wrote in its recently revised report, in contrast to previous expectations of a sudden influx of housing supply once baby boomers downsize, move into retirement homes, or die.

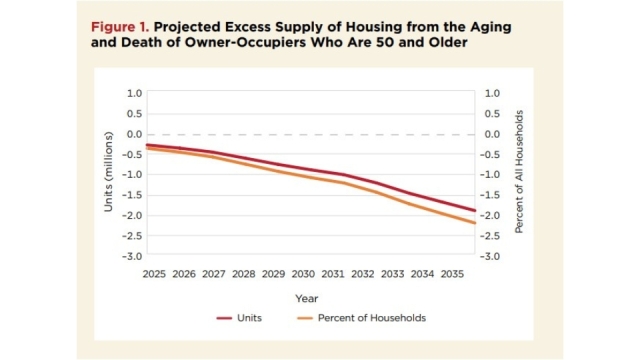

The original report, published in 2022, collected and analyzed vast research from the American Community Survey (ACS), Health and Retirement Study (HRS), American Housing Survey (AHS), and the universe of deaths from the Center for Disease Control’s Vital Statistics program, as well as projections of future population growth and mortality from the Social Security Administration (SSA) Office of the Chief Actuary. The resulting graph depicts the MBA’s original death projections for baby boomers (50+ years old) and the correlating excess supply of housing.

Graph from the MBA RIHA updated report. The dark red line shows the updated projected excess supply of homes for sale as older homeowners age and die over the next decade.

Evidently, housing supply is a function of population mortality, as well as the homeownership rate, cohort size, and how homeowners dispose of their housing assets as they age and die.

However, researchers might have been better off looking into a crystal ball or drawing tarot cards because that goldrush of housing supply is no longer in the MBA’s forecast. The report provides a detailed analysis on the rising homeownership rate for Americans over 50 years old, how the COVID-19 pandemic affected housing decisions, and how supply is being impacted by increased life expectancy.

“The findings highlight the varying patterns for older Americans as shifting demographics, the pandemic, and overall buyer attitudes have impacted buying and selling decisions,” said Edward Seiler, RIHA executive director and associate vice president of housing economics at the MBA. “It is evident that older households are aging in place, leading to updated predictions that show that there will be no excess supply of homes to the markets from older Americans moving or dying over the next decade.”

Get the NMP Daily

Essential stories, every weekday.

Essentially, older Americans are holding onto their homes longer, and there are more of them.

Since 2015, the MBA found there has been a sizable increase in the homeownership rate among seniors age 70 and older. Baby Boomers are holding onto their homes for a longer period of time. Prior to 2015, patterns in the MBA's data suggest that more of those existing homes would have been sold.

In 2022, homeownership rates among 65-plus age group were higher compared to 2015. The increase in ownership rate combined with a higher base of 65 to 70 year-olds in 2022 means that there were almost 2 million more homeowners younger than 70 than in 2015.

As the gap in ownership rates widens after age 70, the cumulative number of additional owners in rapidly increases to a peak of about 7 million more by age 85.

Projections suggest that over 8 million homes will be made available by older Americans as they age and pass away, increasing to around 9 million within the next decade. Approximately 1 million of those homes will be released due to the passing of their owners. This number is nearly double the original projection, driven by a significant rise in homeownership among older adults. On the flip side, fewer existing homes have been sold since 2015 than expected. If age-related homeownership patterns had stayed at 2014 levels, more homes would have entered the market.

Given this unmet past demand, future demand for homes supplied by older Americans is also larger and expected to grow. Overall, there will be no demographic dividend to the net supply of existing homes.

The structured-finance data provider’s first employee succeeds Rahbar following more than a decade with the company

Jonathan Warrick has been named head of dv01, succeeding founder Perry Rahbar in the top leadership role at the structured-finance data and analytics provider.Warrick, dv01’s first employee, most recently served as chief operating officer. Rahbar is transitioning to a strate...

Fitch downgraded the wholesale giant after leverage reached 6.1x, saying the preferred investment changes UWM’s funding structure but does not immediately reduce its debt burden

United Wholesale Mortgage’s $2.05 billion capital reset may strengthen its liquidity and replace secured borrowings, but Fitch Ratings does not believe the transaction immediately reduces the wholesale lender’s debt burden.Fitch downgraded the long-term issuer default rating...

Fitch downgraded the wholesale giant after leverage reached 6.1x, saying the preferred investment changes UWM’s funding structure but does not immediately reduce its debt burden

Payrolls declined in July and previous gains were revised sharply lower, giving the Fed breathing room while raising new concerns about borrower confidence and mortgage-industry employment

Home equity and purchase lending lifted production economics, while management characterized its relaunched wholesale channel as a supporting business rather than a major growth engine