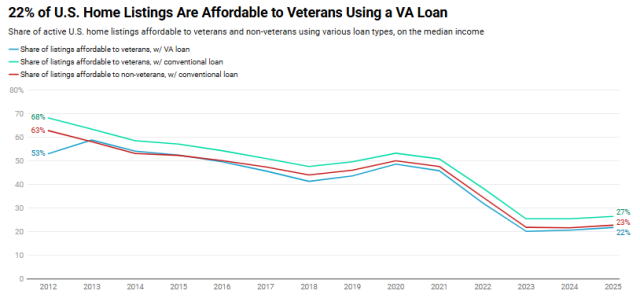

A new study reveals that 21.8% of the nation’s home listings are affordable to the typical U.S. military veteran using a VA loan, while 26.5% are affordable to the typical veteran using a conventional loan.

The analysis of home sales data by Redfin found that affordability for U.S. veterans has improved slightly over the last two years, with 20.2% of listings deemed affordable to the typical veteran using a VA loan in 2023, and 25.5% were affordable to veterans using a conventional loan, the lowest shares on record.

Redfin found a similar share (22.8%) of listings affordable to the typical U.S. non-veteran household with a conventional loan 一 a slight improvement from 2024’s low point, when 21.7% of listings were affordable for non-veterans.

A Shifting Market

Homebuying affordability has tipped marginally in favor of both veterans and non-veterans over the last two years because monthly housing payments have declined, while incomes have risen:

- The average mortgage rate was 6.81% in 2023, and it is 6.66% today. Home-sale prices have flattened; the median U.S. sale price has posted a sub-2% year-over-year increase since April. The median monthly housing payment is lower now than it was two years ago.

- The median household income for veterans is an estimated $85,955 this year, up roughly 10% since 2023. For non-veterans, it is an estimated $81,078, also up roughly 10% over that period.

Veterans using VA loans are able to afford fewer listings than homebuyers who take out conventional loans. Even though the typical veteran earns more than the typical non-veteran — and VA loans come with a slightly lower mortgage rate and no private mortgage insurance — 90% of VA loan users make no downpayment, which inflates monthly payments.

“VA loans provide a great opportunity for first-time veteran homebuyers to purchase a home without the substantial downpayment that’s required of most buyers these days,” said Redfin Economist Grishma Bhattarai. “It allows them to get their foot in the homeownership door and start building equity, but it comes with the tradeoff of a bigger loan and higher monthly costs. That tradeoff is likely the reason why some veterans choose to take out a conventional loan and make a downpayment, even if they qualify for a VA loan.”

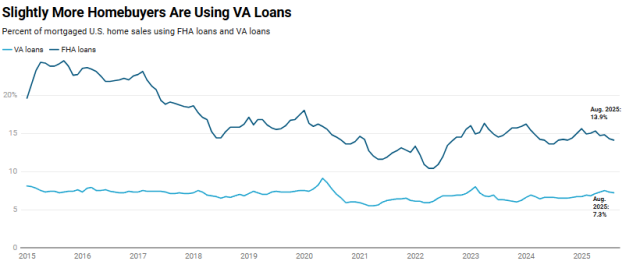

In an analysis of August home sales, 7.3% of mortgaged homebuyers used a VA loan in August, and while that may represent a small share, that total is up from 6.5% a year ago, the highest share of any August in six years. More people are taking out VA loans because in today’s buyer’s market, more sellers are open to accepting buyers coming with no downpayment.

Listings Outpacing Veteran Affordability

Both veterans and non-veterans can afford far fewer listings than they could have a decade ago. A veteran using a VA loan could afford 53% of home listings nationwide in 2015, more than double the share they can afford today. A veteran using a conventional loan could afford roughly 57% of listings in 2015, and a non-veteran using a conventional loan could afford about 52%.

It has become much more difficult to afford a home because sale prices skyrocketed during the pandemic, then rising mortgage rates pushed monthly housing payments to new heights.

The hike in housing costs has far outpaced income increases over the last 10 years. The median U.S. home-sale price has roughly doubled over that period, with the biggest jump in 2021, when record-low mortgage rates and remote work ignited a homebuying frenzy. The typical veteran’s household income has increased by 48% over that period, roughly half the rate of home prices, while the typical non-veteran’s income has increased 54%.

Even with access to financial tools like VA loans, the typical veteran is priced out of many listings. A low-downpayment loan can only do so much when home prices and mortgage rates are elevated. The bright side is that homebuying affordability has started improving in parts of the country where home prices are declining, including several Florida metros, Phoenix, and Atlanta. And mortgage rates have come down from their peak, with the average 30-year fixed rate sitting near its lowest level in a year.

Targeting Destinations For VA Borrowers

Redfin found that 60% of home listings are affordable to a veteran using a VA loan in Detroit, Michigan, more than any other major U.S. metro area. Detroit was followed by:

- San Antonio, Texas, where 53.4% of listings are affordable

- Cleveland, Ohio, where 48.3% of listings are affordable

- Pittsburgh, Pennsylvania, where 43.6% of listings are affordable

- Baltimore, Maryland, where 42.7% of listings are affordable

The ranking is the same for veterans using conventional loans, though they can afford a slightly higher share of listings. In Detroit, 64.9% of listings are affordable to those using conventional loans, followed by:

- San Antonio, Texas, where 61.1% of listings are affordable to those using conventional loans

- Cleveland, Ohio, where 53.3% of listings are affordable to those using conventional loans

- Baltimore, Maryland, where 49.9% of listings are affordable to those using conventional loans

- Pittsburgh, Pennsylvania where 49.3% of listings are affordable to those using conventional loans

On the flip side, veterans can afford nearly none of the home listings in California. In the San Jose, Los Angeles, and San Francisco markets, a veteran using a VA loan can afford less than 1% of for-sale homes, the smallest shares in the country, followed by San Diego and Anaheim, where they can afford roughly 2% of listings.

Meanwhile, those vets using a conventional loan are basically in the same boat, able to afford 1% or fewer listings in San Jose and Los Angeles, 1.3% in San Francisco, 3.6% in San Diego, and 2.9% in Anaheim.

Veterans, like other homebuyers, can afford a far higher share of homes in places where homes are relatively affordable than in places where homes are expensive. The typical Detroit home sold for $215,000 in September, while the typical San Jose home sold for $1.6 million.

What Lies Ahead for VA Buyers?

In a separate report, Redfin found that nationwide, 7.3% of mortgaged homebuyers used a VA loan in August, up from 6.5% a year earlier and the highest share for that month since 2019.

“Military members have made sacrifices to protect our home,” said Bill Banfield, chief business officer at Rocket. “VA loans are one of the most powerful benefits available to veterans and service members, opening doors to homeownership with zero down payment, no monthly mortgage insurance, and flexible credit requirements. Now is a prime time for veterans and service members to take advantage of them. VA loans have a better chance of getting accepted in today’s buyer’s market than they did several years ago, when buyers were competing against each other and sellers were calling the shots.”

The share of mortgaged homebuyers using a VA loan has increased, and so has the number of buyers taking out VA loans. Nationwide, the number of VA loans rose 3% year over year in August, while the number of conventional loans declined 9%.

“A buyer can make an offer with a VA loan, put virtually no money down, ask for $5,000 in closing credits, and get their offer accepted,” said Jim Fletcher, a Redfin Premier agent in Tampa, Florida. “The market is slow, there’s a backlog of inventory, and buyers are in the driver’s seat. Florida historically has had a lot of all-cash buyers, but recently, there are more financed buyers — and many of them are able to win homes with ultra-low down payments while also having the seller cover most closing costs.”

Gauging VA Hotbeds

In terms of targeting locations where VA loans were most prevalent, Redfin found that in August 2025, 43.2% of all mortgaged homebuyers in Virginia Beach, Virginia used a VA loan, the biggest share of any major U.S. metro. Typically, instances where a high number of VA loans are being used are located near military installations. Virginia Beach was followed by:

- Jacksonville, Florida, where 17.2% of mortgaged homebuyers used VA loans

- Washington, D.C., where 16.7% of mortgaged homebuyers used VA loans (the highest August share for D.C. in 14 years)

- San Diego, where 15.2% of mortgaged homebuyers used VA loans

- Las Vegas, where 11.9% of mortgaged homebuyers used VA loans

Virginia Beach is also where the use of VA loans increased most year-over-year, rising to 43.2% of all mortgage home sales from just under 40% a year ago. The next-biggest YoY increases were reported in:

- Orlando, Florida, at 8.2%, up from 5.3% last August

- San Diego, California, at 15.2%, up from 12.3% last August

The use of VA loans increased in 32 of the 40 metros in this analysis. In the places where they became less common, the dips were approximately one percentage point or less.