We are in the process of hiring a new director for our company. He will be moving to Utah from out of state. With his six-figure salary he qualified for more than half a million-dollar loan.

Four years ago, I bought a 4,600-square-foot house on a full acre within 10 minutes of our office within his price range. When I asked what he was finding, he told me he was driven 45 minutes away to look at townhomes or 2,000-square-foot homes that were more than 50 years old on less than a quarter of an acre that needed major renovations. To say he looked miserable after his weekend of house hunting would be an understatement.

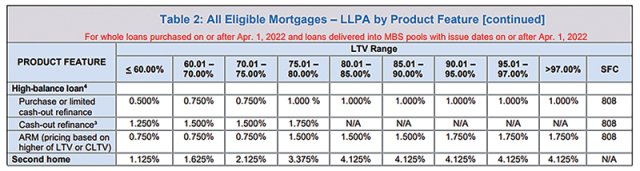

What can be done to help the situation? According to Fannie Mae and Freddie Mac, an increase on high balance loans of between 0.25% and 0.75% and a similar increase on second homes of between 1.125% and 3.875% will help to ensure that they will have the funds to better help lower-income home buyers.

On Jan. 5, 2022, Fannie Mae and Freddie Mac jointly announced their loan-level price adjustments (LLPA) for high-balance and second home loans. Unlike their March 2021 announcement for non-owner-occupied increases, they are giving lenders time to prepare to make the changes. However, as this change could result in tens of thousands of additional dollars for high-balance loans, you will likely see it appear on your pricing before the April 1 deadline.

In the press release announcing the change FNMA Acting Director Sandra L. Thompson stated the purpose of the increase would help facilitate “equitable and sustainable access to homeownership” while also increasing the GSEs' regulatory capital position.