The total number of loans now in forbearance decreased by 3 basis points last month, slipping from 0.72% of servicers’ portfolio volume in August to 0.69% as of Sept. 30, according to the Mortgage Bankers Association (MBA).

Monday afternoon, the MBA released its monthly Loan Monitoring Survey, revealing that 345,000 homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 2 basis points to 0.3%, while the forbearance share for portfolio loans and private-label securities (PLS) declined 12 basis points to 1.14%. Ginnie Mae loans in forbearance, however, ticked up 1 basis point to 1.33%.

“The overall number of loans in forbearance dropped in September, but the pace of forbearance exits slowed to a new survey low and new forbearance requests continued to come in. This dynamic in turn prevented any substantial improvement in the forbearance rate,” said Marina Walsh, MBA’s vice president of Industry Analysis. “The COVID-19 federal health emergency is still in effect and, in most cases, borrowers can still seek initial COVID-19 hardship forbearance.”

“In the near-term,” Walsh continued, “the number of loans in forbearance will likely increase for another reason — the recent devastation caused by Hurricane Ian in Florida, South Carolina, and other states.”

Walsh said the MBA’s Loan Monitoring Survey requests that servicers report all loans in forbearance “regardless of the borrower’s stated reason — whether pandemic-related, due to a natural disaster, or another cause.”

Other highlights from the report:

- Loans in forbearance as a share of servicing portfolio volume as of Sept. 30:

○ Total: 0.69% (previous month: 0.72%).

○ Independent Mortgage Banks (IMBs): 0.95% (previous month: 0.96%).

○ Depositories: 0.48% (previous month: 0.52%).

- By stage, 33.7% of total loans in forbearance are in the initial forbearance plan stage, while 53.2% are in a forbearance extension. The remaining 13.1% are forbearance re-entries, including re-entries with extensions.

- Of the cumulative forbearance exits for the period from June 1, 2020, through Sept. 30, 2022, at the time of forbearance exit:

○ 29.6% resulted in a loan deferral/partial claim.

○ 18.3% represented borrowers who continued to make their monthly payments during their forbearance period.

- ○ 17.3% represented borrowers who did not make all of their monthly payments and exited forbearance without a loss mitigation plan in place yet.

○ 16% resulted in a loan modification or trial loan modification.

○ 11% resulted in reinstatements, in which past-due amounts are paid back when exiting forbearance.

○ 6.6% resulted in loans paid off through either a refinance or by selling the home.

○ The remaining 1.2% resulted in repayment plans, short sales, deed-in-lieus, or other reasons.

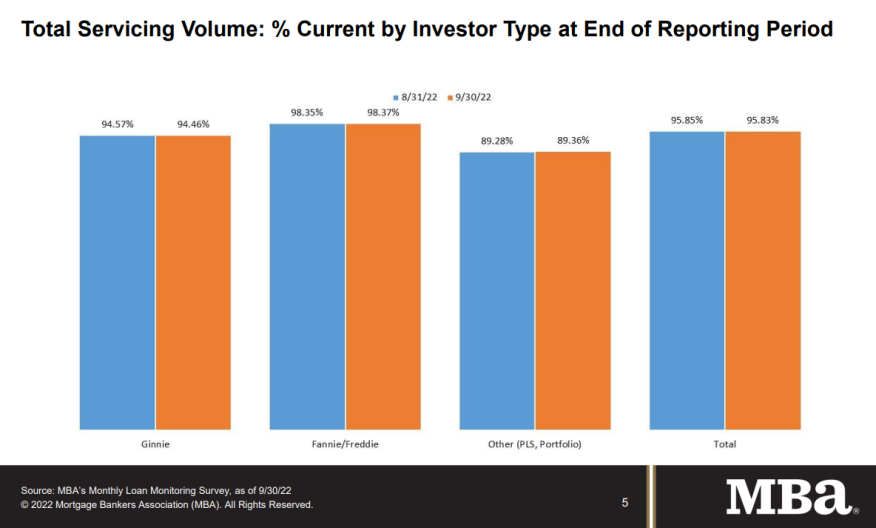

- Total loans serviced that were current (not delinquent or in foreclosure) as a percent of servicing portfolio volume decreased to 95.83% in September 2022 from 95.85% in August 2022 (on a non-seasonally adjusted basis).

○ The five states with the highest share of loans that were current as a percent of servicing portfolio: Idaho, Washington, Colorado, Utah, and Oregon.

○ The five states with the lowest share of loans that were current as a percent of servicing portfolio: Mississippi, Louisiana, New York, West Virginia, and Indiana.

- Total completed loan workouts from 2020 on (repayment plans, loan deferrals/partial claims, loan modifications) that were current as a percent of total completed workouts increased to 78.7% last month from 78.31% in August.

MBA’s monthly Loan Monitoring Survey covers the period from Sept. 1-30, 2022, and represents 65% of the first-mortgage servicing market (32.7 million loans), it said.

The MBA represents the real estate finance industry, which employs more than 400,000 people in virtually every community in the country. Its membership of more than 2,200 companies includes all elements of real estate finance: independent mortgage banks, mortgage brokers, commercial banks, thrifts, REITs, Wall Street conduits, life insurance companies, credit unions, and others in the mortgage lending field.