In 2022, the U.S. residential mortgage backed securities (RMBS) market came in like a lion and out like a lamb.

According to a recent report published by DBRS Morningstar, a financial services firm headquartered in Chicago, bond markets, including RMBS, saw increasing market value losses, while issuers saw deal execution costs grow much more expensive. As a result, RMBS issuance volumes contracted.

Last year started with low mortgage rates, brisk organization and securitization volume, as well as extraordinary home-price appreciation. Then, inflation began to rage, causing the Federal Reserve to tighten monetary policy in March, taking the benchmark federal funds rate from what had been several years at zero to +425 basis points (bps) within a few quarters.

Home prices are beginning to plateau or even retreat in a number of areas as home sales wane. Now that the 30-year mortgage rate is in the 6.5% to 7% range — 300 bps higher year-over-year — prepayment speeds are down by 50% to 75% or more to the low-single digits, effectively at historically low baseline turnover speeds.

However, very good credit performances — measured by delinquencies (DQs) and losses — have improved throughout 2022. Last year saw the lowest total delinquency numbers the market has seen in a long time, the report states. But, given cloudy economic conditions, delinquencies are expected to increase.

Moving into 2023, DBRS Morningstar anticipates lending volumes will be lower versus 2022, and credit performance will begin to slip. As long as there is no significant recession, credit should remain well contained, it said.

Economic conditions will play a key role in the direction of RMBS credit performance, the report said. Inflation remains abnormally high, but GDP and unemployment remain resilient. If higher employment emerges, it would have an adverse effect on credit, the report states.

DBRS Morningstar also offered its RMBS credit outlook for 2023. Some highlights:

Prime Credit: Prime RMBS issuance started very strongly in 2022, but quickly tapered off as higher rates and private-label execution costs quickly rose from the second quarter on. Prime RMBS issuance will likely be much lower in 2023 versus 2022, especially since the 2023 base-conforming jumbo loan limit will be $726,200, with certain areas being above $1 million.

Credit performance has been good, though, and it should continue into 2023. Prepayments are slowing now, in the 4% to 5% conditional prepayment rate (CPR) range, and, if this continues, it will likely result in longer average lives.

Non-QM: Non-qualified mortgage (Non-QM) RMBS loan production and RMBS issuance is expected to be lower in 2023 as origination volumes significantly fell in the second half of 2022. Adverse market conditions, with fewer lenders and available capital, will continue to be a challenge as the industry tries to right-size operations and pipelines to adjust to higher rates. The Non-QM market will continue to evolve as new entrants and well-capitalized lenders may attempt to fill the void left by weaker players exiting and curtailing lending. There should be continued stable pool performance for seasoned deals. Also, newer issuers will likely show slower deleveraging and fewer optional redemptions.

GSE CRT: CRT mortgage credit has been nominally good. This year shows a general trend of steadying to slightly better total DQs and historically low realized losses despite the pandemic aftermath. For 2023, recent credit performance trends are anticipated to continue, even with the possibility of recession. Housing technicals and mortgage fundamentals overall look to be relatively more resilient to stress than in past downturns, but there are certain vintage differences to be aware of.

Reverse Mortgage: In 2023, expect slower issuance given volume outlooks for lenders/securitizers, refinance activity waning, and higher rates resulting in lower loan amounts that could be offered to borrowers. The prior market shift to primarily floating-rate loans means much higher resets currently, which could have mixed effects on deal asset/liability coverage. Credit-wise, this may limit the size of lines of credit, especially as home values plateau and/or possibly decline. However, continued performance should remain relatively stable, absent significant declines in home price appreciation.

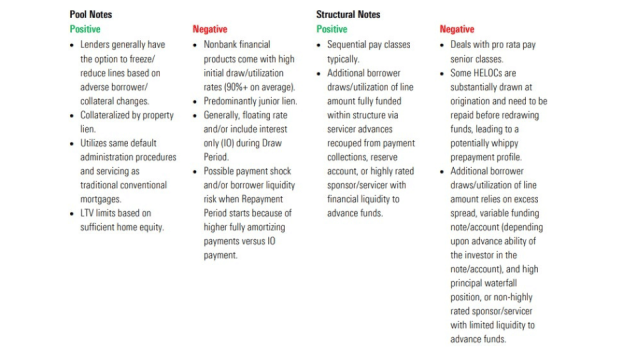

HELOC: As mortgage rates moved higher, home equity line of credit (HELOC) originations grew from previously low levels for both bank and newer-to-market nonbank financial lenders. A few home equity RMBS deals came to market this year and, for 2023, HELOC originators may see securitization as an attractive exit strategy as significant homeowner equity availability still exists, and lenders can price at current rates. Newer nonbank financial HELOC products will likely continue to see borrower uptake, with product features helping temper credit risk.