“Rocket advertised in the past, ‘click-button-get-mortgage’ direct-to-consumer mortgage experience … I think that’s becoming less and less important for [Rocket],” Dahlhausen said. “We can participate in this growth if we really establish embedded finance, bypassing this referral relationship that traditional lenders have and get direct access to these real estate agents.”

Still, even small to mid-size lenders are equipped with their own unique business models structured to broaden their services and gain further control of the transaction or consumer experience.

Dahlhausen has been developing and scaling up his concept of “embedded finance” at Realfinity in which agents are trained and licensed through his company to offer mortgage service, enhancing their value proposition and service quality, while saving their clients’ costs.

The overall concept of “embedded finance” is about more than simply combining both the real estate and mortgage process; it’s about building up the services or products offered at the point-of-sales solution.

Dahlhausen offers an airline analogy, saying that while buying an airline ticket, travel insurance is offered at the point of sale, which is the core concept of embedded finance. The airline is in the business of providing flights, not a financial service provider, but still offers an insurance policy seamlessly into their transactions.

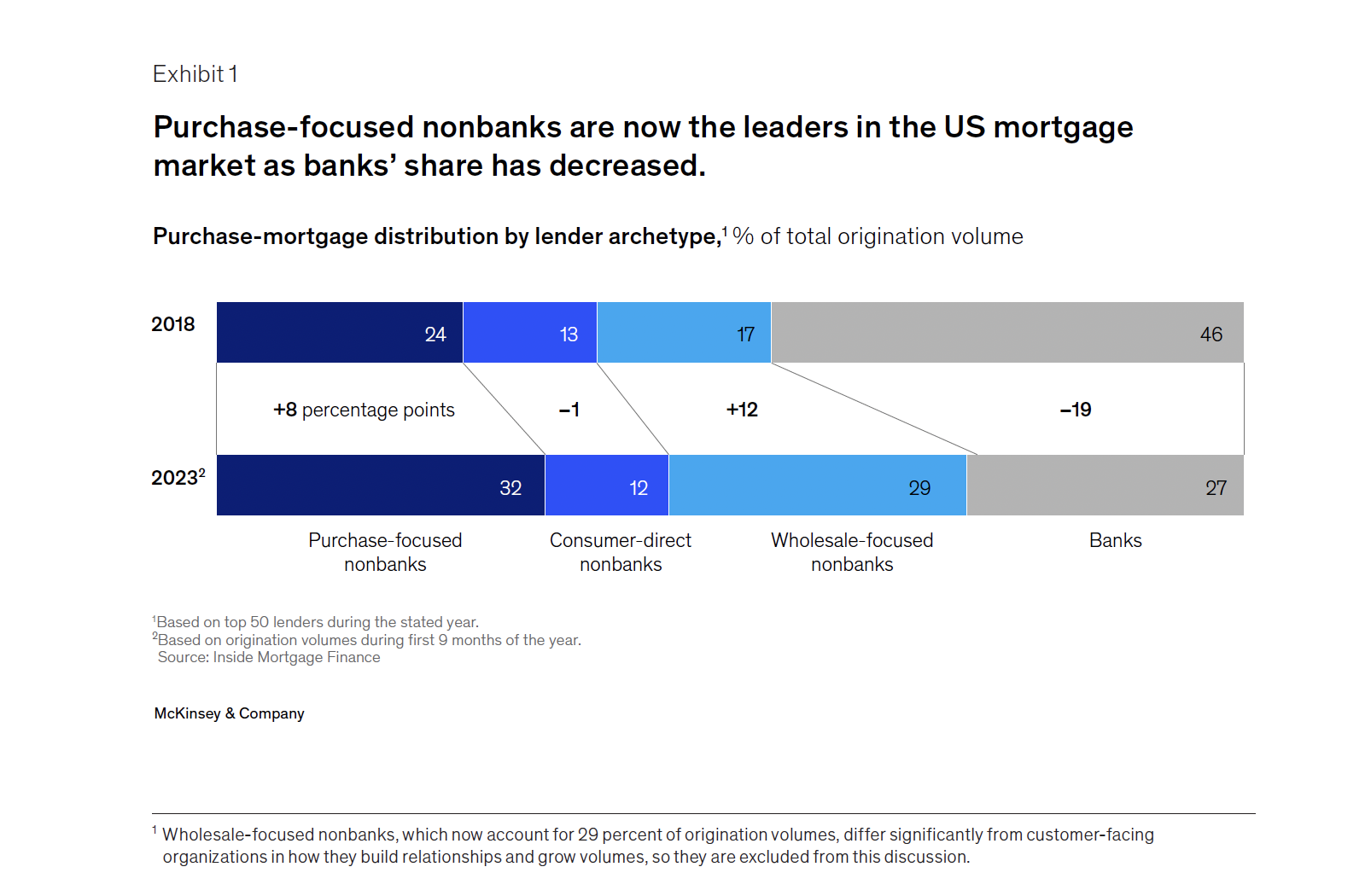

“Whoever's trying to build a successful mortgage business for the long term, they need to focus on the purchase business,” Dahlhausen recommended. “So I think allowing these referral relationships to embed finance into their existing workflows is going to be — and is continuing to be — how consumers make their decisions.”

‘Wake Up Call’ For Brokers

For larger lenders, brokers serve the vital function of developing local connections with consumers, a much cheaper strategy to expand the company’s footprint than building brick and mortar shops in every local market. The trade-off, however, is that brokers aren’t expected to send 100% of their business to one lending partner.

Rocket announced the Redfin acquisition as a strategy to boost its purchase business, leading some to believe Rocket would sacrifice its broker network for its shiny, new megarealty partner.

“If you're a broker, they're competing with you directly,” Roque said. “Or [United Wholesale Mortgage]. UWM is a true TPO platform. They're truly committed to the broker because they have no channel conflict. They have no retail loan officers.”

Yet, a few hours after the acquisition of Mr. Cooper Group was announced, Krishna told NMP that brokers and other existing Rocket partners will benefit from the integration of both companies.

“We think the broker is a huge winner in this and there's really two simple reasons. The first one is just [that] they're getting access to a bigger ecosystem, thanks to Redfin, [and] they now have a new lead generation engine to generate more demand,” Krishna said. “On the Mr. Cooper side, I would say the same. One of the biggest pain points for brokers is really being able to think about capabilities like servicing. So imagine that we were able to offer servicing capabilities to the broker where they could put their name on the mortgage statement.”

Bringing both Redfin and Mr. Cooper into the fold in the first quarter of 2025 helps clarify what Krishna was alluding to in an exclusive interview with NMP in late 2024. “In 2025, we're doubling down here on TPO,” Krishna said. “We're gonna be focused on providing even more of the human-powered, AI-boosted innovation to our broker partners.”

“A big-time value proposition for us,” Krishna continued, “is actually taking the capabilities of our mortgage platform and extending those capabilities to benefit the broker community so that we can holistically go after the broadest market possible, and we can meet our clients where they are in whatever way that they want to work with us.”

At least one of Rocket’s top broker partners, Tim Gentry, founder and CEO of Georgia-based Loan Velocity, has said that Rocket’s rebranding has helped his small brokerage obtain more recognition and credibility. Particularly, Rocket’s “Own The Dream” Super Bowl commercial was said to have resonated with his current and past clients.

“I got so many clients and friends, and my loan officers got so many texts that night from their borrowers or from agents saying, ‘Well, I loved y'all's commercial.’ They think Loan Velocity is Rocket,” Gentry said. I have to undo that sometimes. But when I call a client, and [say] ‘Yeah, I'm a Rocket broker.’ That gives me credibility right away.”