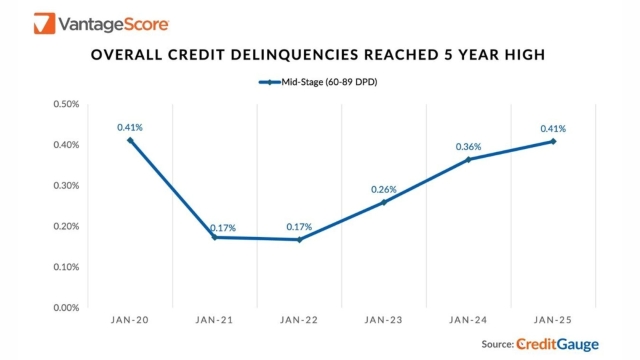

Consumer credit delinquencies have reached their highest level in five years, according to the January 2025 edition of CreditGauge from VantageScore. The report signals growing financial strain among borrowers, some of which is driven by mortgage debt.

The average VantageScore 4.0 credit score held steady at 702 in January. However, credit account balances surged by more than $1,000 compared to December 2024—the largest month-over-month increase in nearly three years --- bringing total balances to a five-year high.

"The combination of rising mid-to-late-stage credit delinquencies and rising credit balances suggests a growing debt burden that some consumers are increasingly struggling to manage," said Susan Fahy, Executive Vice President and Chief Digital Officer at VantageScore. "This is both a short- and long-term trend. Later-stage delinquencies are key because they are an indication that late payments will likely not go away anytime soon."

Auto loan delinquencies saw a notable uptick in January, likely driven by elevated borrowing costs and post-holiday spending. Overall mid- and late-term delinquencies reached their highest levels since January 2020, underscoring the financial pressures on borrowers who are already behind on payments.

Credit card originations declined 0.23% in January from the previous month, reflecting reduced consumer demand following the holiday season. On a year-over-year basis, credit card originations remained nearly flat, rising just 0.04%. This suggests that consumers may be prioritizing existing debt management over taking on new revolving credit.

Mortgage debt was the main culprit in driving up credit balances. Overall credit balances climbed to $105,700 in January, up $1,049 (+1.0%) from December 2024, marking a five-year high. Mortgages were the primary driver of this increase, as elevated home prices and high interest rates continued to weigh on consumers’ ability to pay down mortgage debt. Credit balances also rose by $1,350 (+1.3%) compared to January 2024.

Speaking on CNBC, VantageScore President and CEO Silvio Tavares pointed to rising service costs, including home and auto insurance, as a key factor impacting credit trends, particularly for higher-income consumers.

“Consumers are being cautious with credit. While credit card balances have risen about 2.9% year-over-year, this increase aligns with inflation,” Tavares noted. “Credit utilization has actually declined on an annual basis, down about a full percentage point to 51.6%. This indicates that while consumers have available credit, they are choosing to limit their usage.”

For mortgage loan originators, these credit trends highlight a shifting financial landscape. Rising delinquencies and growing debt burdens could impact borrower eligibility, while restrained credit card usage suggests a more cautious consumer approach to financial management in 2025.