Making the numbers work still isn’t easy for most homebuyers, but they are looking better than they have in more than three years, according to the latest report from First American.

First American’s latest Real House Price Index shows that affordability has improved with widespread gains. Appreciation has slowed below the pace of income growth, and that is slowly improving monthly payments and helping more buyers qualify for financing.

“Affordability still isn’t ‘easy’ in absolute terms, but the trend line is supportive of more transactions,” commented First American Deputy Chief Economist Odeta Kushi.

Existing home sales increased in November and are expected to increase again when the December figures come out, the report said. This “modest positive momentum” suggests that the housing market is slowly thawing, although activity remains significantly below pre-pandemic levels. Several factors are working in favor of more sales, while others continue to hold it back.

On the plus side, affordability matters even more than mortgage rates, FirstAm said, and it is better than it has been in more than 36 months. Better yet, the gains are widespread, touching most markets on an annual basis. The math on monthly payments for would-be buyers is “slowly improving” and helping more households qualify at the margin.

At the same time, active inventories are running above year-ago levels, not only offering house hunters more choice but also reducing buyer fatigue and making it easier for deals to come together. First American calls this a “meaningful shift.”

Demographic trends also are playing a part in the market’s revival, the company reports.

“Many potential first-time millennial homebuyers have been waiting for conditions to improve, and even modest gains in affordability can spur that demand back into the market,” First American noted. “If inventory continues to build, buyers who were sidelined by limited options may re-engage, helping convert pent-up demand into actual transactions.”

Still, the mortgage “lock-in” effect remains an obstacle.

“The golden handcuffs” that are keeping many possible sellers in place “are loosening,” economist Kushi says, “but they’re not off.”

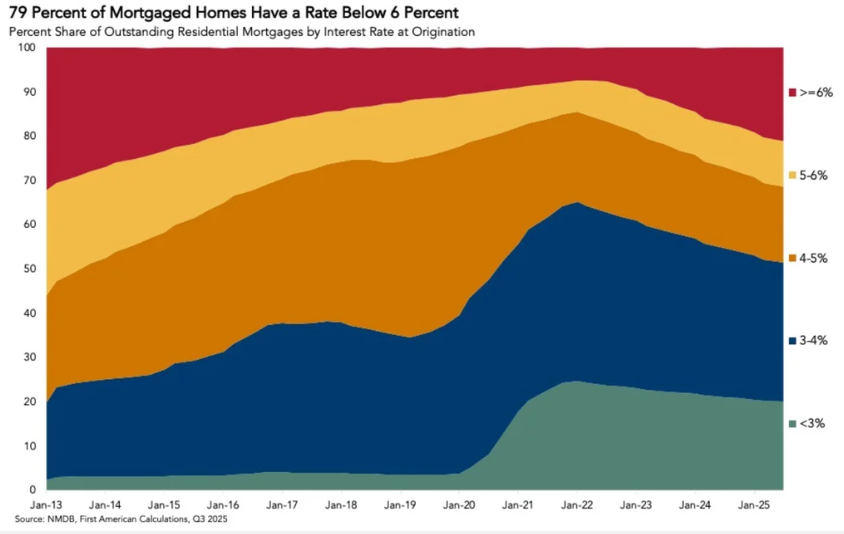

The company says roughly 79% of mortgaged homes still carry a rate below 6%. Consequently, selling often means trading a low payment for a higher one and the difference is often enough to keep many “optional” sellers on the sidelines and limit turnover.

But last year, for the first time since 2020, the share of home buyers with rates above 6% exceeded the share with rates below 3%, an indication that the lock-in effect is fading.

Uncertainty is another headwind. “Households don’t need perfect clarity to buy a home, but uncertainty around the economy, inflation, and the path of interest rates can delay big decisions,” says Kushi. “That’s why existing-home sales can look like they’re gaining traction one month and stall the next. The market responds quickly to changes in rates and sentiment, and volatility can freeze activity at the margin.”

Looking forward, First American expects “a gradual thaw” in the market as opposed to a sudden breakout. “The most realistic expectation is continued, incremental progress.”

Elevated mortgage rates are likely to “keep the market in a measured, stop-and-go recovery” pattern rather than a strong rebound, the company predicts. But its “cautious optimism” hinges on a rising tide of more homes for sale to spur the market. As Kushi noted, “you can’t buy what’s not for sale.”