Loan Factory's leading MLOs build trust through shared identity

BY KATIE JENSEN

The swift and unlikely ascent of the nation’s second largest mortgage brokerage, Loan Factory Inc., is owed to its founder and CEO Thuan Nguyen, whose harrowing journey to America shows why the company continues to persist. But industry peers would undoubtedly like to know how Loan Factory also managed to become the nation’s fastest growing brokerage during a particularly tough time in the market. While most of the industry has been consolidating, Nguyen has been recruiting at a neck-breaking pace, hiring 100 new hiring loan officers and processors per month, prompting industry peers to say: “In this economy?!”

It’s almost as if Loan Factory is operating in an entirely different market, and in a way, it is.

Loan Factory’s mega broker status overshadows another major characteristic of the company. Ironically, its business model reflects a niche or even “micro-niche” lender, which sources about 70% of its business from Vietnamese immigrants — a demographic making up less than 1% of the US population.

Some industry veterans would believe that niche-focused lending is not conducive to scaling a mortgage company in the same way they’d believe that fishing in a smaller pond would mean you catch fewer fish. All existing evidence suggested that to be the case, until Loan Factory’s rise in 2024.

The closest comparison to Loan Factory, as a large-scale lender with a niche focus, would be New American Funding (NAF), a Latina-owned and minority-focused retail lender with more than 2,000 loan officers on staff. According to 2023 HMDA data, only 36% of NAF’s originated loans went to minority borrowers. Still, that figure is well above the industry-wide average of 16% in 2023.

Nationally, the percentage of originated loans that went to white borrowers in 2023 is 67%. Loan Factory’s lending practices invert that number, issuing 67% of their loans to minority borrowers.

Compared to the rest of the mortgage industry, which has always struggled to overcome racial disparities in lending, it’s like watching someone pull elephants from a hat. Where are these Vietnamese immigrant borrowers coming from and how is Loan Factory able to support them?

The Other Housing Market

Members of the Vietnamese community in the U.S., 60% being immigrants, are categorized as Asian borrowers, along with Asian Indian, Korean, Japanese, Chinese, Filipino, Hawaiian, and Pacific Islanders. Despite their many differences in culture and language, the industry does not look at separate trends among each group. Inevitably that leads to overgeneralizations about Asian borrowers, causing them to be misperceived.

It would seem impossible for Loan Factory to originate such high volumes when a 2021 CFPB study shows that Asian American and Pacific Islanders (AAPI) borrowers have lower incomes, credit scores, and a homeownership rate of 60% compared to 75% among whites. At first glance, Vietnamese and other Asian borrowers may be considered as “tough to qualify” by lenders, but a closer look reveals that those demographic trends are misleading. Loan Factory’s top originator (in unit volume), Suong Nguyen, says almost all of her borrowers are Vietnamese immigrants, with a few Chinese or Filipino borrowers. Out of the 153 loans she originated in the past year ($40 million in dollar volume), according to Market Mobility Intelligence (MMI), all but two were conventional loans.The “model minority” myth detailed in the 2021 CFPB study “AAPI Borrowers in the Mortgage Market,” is a stereotype that all Asians are viewed as being high-achievers which, in mortgage terms, means higher credit scores, lower debt-to-income ratios (DTIs) — all the positive attributes of an A+ borrower. But the study, using 2020 HMDA data, points out the different characteristics between subgroups.

Hawaiian or Pacific Islanders (HoPI) borrowers, for example, are more likely to be low- to middle-income (LMI) than other Asian subgroups. On the other hand, most Vietnamese borrowers display those “model” characteristics, showing 90% of their loans are conventional. The homeownership rate among Vietnamese immigrants, specifically, is 73% according to the 2023 American Community Survey — the highest among all immigrant and minority groups.

Suong Nguyen

Loan Factory’s top originator in unit volume

How do you say you’re a top producer without saying you’re a top producer? Loan Factory’s leading originator, Suong Nguyen, who closed 153 loans in 2024, says, “I don’t do cold calling.” When asked how she managed to secure so many referral connections, she adds, “I don’t look for Realtors; Realtors reach out to me.”

Image captions

“Most of my clients go with conventional because most of them have good credit,” said Suong Nguyen. “Income is not that high in Vietnamese communities, but they always have good credit and they always have support from family for the down payment.”

Even though Vietnamese borrowers have better credit profiles compared to other minority groups, they still face similar denial rates.

On average, Vietnamese borrowers have higher credit scores and incomes, as well as lower median DTIs and combined loan-to-value ratios (CLTV), than Black and Hispanic borrowers. The 2021 CFPB study shows Vietnamese borrowers’ denial rates were still similar to those for Black and Hispanic borrowers.

Loan Types By Loan Factory

Although income is not that high within the Vietnamese community, Suong Nguyen says her borrowers “always have good credit,” evidenced by the company’s lending profile on Modex, which shows about 80% of the loans originated in 2024 were conventional. Source: Loan Factory, Inc.

Although income is not that high within the Vietnamese community, Suong Nguyen says her borrowers “always have good credit,” evidenced by the company’s lending profile on Modex, which shows about 80% of the loans originated in 2024 were conventional. Source: Loan Factory, Inc.

Even among Asian subgroups, though, Vietnamese borrowers had the highest mortgage denial rate at 13%. The credit profiles of Vietnamese immigrant borrowers cannot explain their mortgage denial rates, so what does? One possible answer: a separate, more recent CFPB study suggests that Vietnamese borrowers may face a stronger language barrier when applying for mortgages, impeding their ability to submit as strong a mortgage application as possible.

The 2024 study, “Empowering Limited English Proficient (LEP) Communities,” found that Vietnamese immigrants are much more likely to have limited English proficiency compared to other immigrant groups: About 64% of Vietnamese Americans speak English less than “very well.” Among those who speak Vietnamese at home, only 55% speak English fluently. For comparison, of those who speak Spanish at home, 73% speak fluent English.

Notably, the study found Vietnamese-speaking borrowers are more likely to prefer documents in their native language, and tend to rely heavily on family members to translate documents and home loan concepts for them.

Taking Over Texas

Vietnamese immigrants, like many immigrant groups, live in concentrated regions or “enclaves” across the country, with maps by the U.S. Census Bureau showing lenders exactly where they could source such business. Modex shows that about 46% of Loan Factory’s business came from California and Texas in the past 12 months.

In the heart of Houston, is a neighborhood that holds one of the largest Vietnamese enclaves in the U.S. With an estimated Vietnamese population of 180,000, the neighborhood is nicknamed “Little Saigon,” or “Vietnam Town.” Following the end of the Vietnam War in 1975, an influx of first-generation Vietnamese immigrants emigrated from the former South Vietnam and resettled in the Houston area, naming it after their fallen capitol, Saigon. Decades later, it seems like a community wildly out of place, but Vietnamese immigrants have said they were drawn to its then-booming economy, affordable cost of living, warmer climate, and proximity to the ocean.

And yet, any lender that attempts to access the Vietnamese market in Texas will have trouble finding it, since it’s located in the palm of Suong Nguyen’s hand.

Suong sources all of her business in Texas, since it’s the only state where she’s currently licensed. Every year since Suong joined Loan Factory in 2018, she’s mainly originated purchase loans. Even during the 2020 and 2021 refinance boom, Modex shows that purchase business comprised 72% and 77% of Suong’s yearly volume, respectively. In 2022, while Loan Factory and much of the mortgage industry struggled to cope with rising rates, Suong still averaged seven loans per month, 90% of which were conventional loans.

Doing more purchase business has helped Suong develop “a good book of business” in Texas within the past seven years — so good, in fact, the business now comes to her.

“I don’t do cold calling,” Suong said. “Most of my clients are from referral sources. I do run some advertisements on Facebook and social media, but not that much.”

Rather, she claims that she knows all the Vietnamese Realtors and real estate agents in Texas, though especially around Houston or “Vietnam Town.” Modex and MMI show nearly every one of her transactions in the past 12 months was closed with a Vietnamese buy-side agent. Not just a few Vietnamese Realtors or agents, either — Suong worked with roughly 75 different Vietnamese buy-side agents in 2024.

When asked how she formed so many relationships with Vietnamese Realtors, Suong said, “I don't look for Realtors; Realtors reach out to me.”

All Or Nothing

Some lenders are more selective when recruiting loan officers; they want top producers, loan officers with specialties, or just someone with experience in the mortgage industry. But Nguyen doesn’t care about any of that, saying “We pretty much accept you as long as you work on helping the client.” Instead, he hires loan officers based on their attitude, like Anne Nguyen.

Not many people can understand Nguyen’s dangerous attempt to flee Vietnam at only 14 years old, but other Vietnamese and U.S. immigrants likely can. Similarly, not many people would understand Anne Nguyen’s decision to quit her full-time job to start originating mortgages.

Anne Nguyen, Loan Factory’s top producing originator in terms of dollar volume ($49 million in year-over-year volume per MMI) has only worked two years in the mortgage industry. She started working at Loan Factory in late 2022 when rates began to steadily rise from historic, pandemic-era lows.

Anne Nguyen

Loan Factory’s top originator in dollar volume

Anne Nguyen was warned that her job would get tough when she entered the mortgage industry in 2022, as interest rates began to rise. However, having already quit her day job, Anne told herself, “I either do this in full, or I don't do it at all.” By 2024, Anne was Loan Factory’s top-producing loan officer, raking in an annual loan volume of $49 million, according to MMI.

Image captions

“So I have never seen the good time,” Anne said. “When I first joined Loan Factory and talked to [CEO] Thuan, he said that I only need to do three files per month and I should be good. Back then it was tough. Most loan officers did not produce. So he was saying, ‘You should keep your full-time job.’”

But, apparently, Anne and her employer Nguyen were cut from the same cloth. Anne admits that she had already quit her full-time job, telling herself, “I either do this in full or I don't do it at all,” reflecting a similar audacity and fierce determination as her employer. For both, failure was never an option.

Anne’s loan volume surged in 2023 — her first full year — to just under $19 million with 46 closed loans, averaging 3 to 4 loans per month. By November 2024, she had already more than doubled her 2023 volume. Anne estimates that 98% of her borrowers are Vietnamese immigrants.

“Their English is not that good,” she explains, anecdotally confirming the CFPB’s 2021 findings.

“They cannot go through the application themselves, so I show them how.”

“They only need to upload their driver's license, their pay stub, their taxes, and everything to the portal,” Anne continues. “Then the AI [artificial intelligence] will read all of that and get that information into the application for me. So the clients don't have to struggle.”

Loan Factory’s AI Application can also reduce turnaround times, Anne says, “because half of the application is already done. I just go in and review the supporting documents on the application to make sure that it's accurate.”

When asked how she targets Vietnamese immigrant borrowers, Anne laughed, saying, “I do not choose the demographic at all. They chose me for some reason.” Then added, “Right now, I don't do any advertising or marketing. It's purely just word of mouth.”

As a Vietnamese immigrant herself, Anne attracts Vietnamese clients by nature of her proximity and knowledge of that community and their experiences. She acknowledges that having a Vietnamese immigrant CEO helps “peak curiosity from the clients so they know about the [Loan Factory] name.”

Production & Growth Strategy

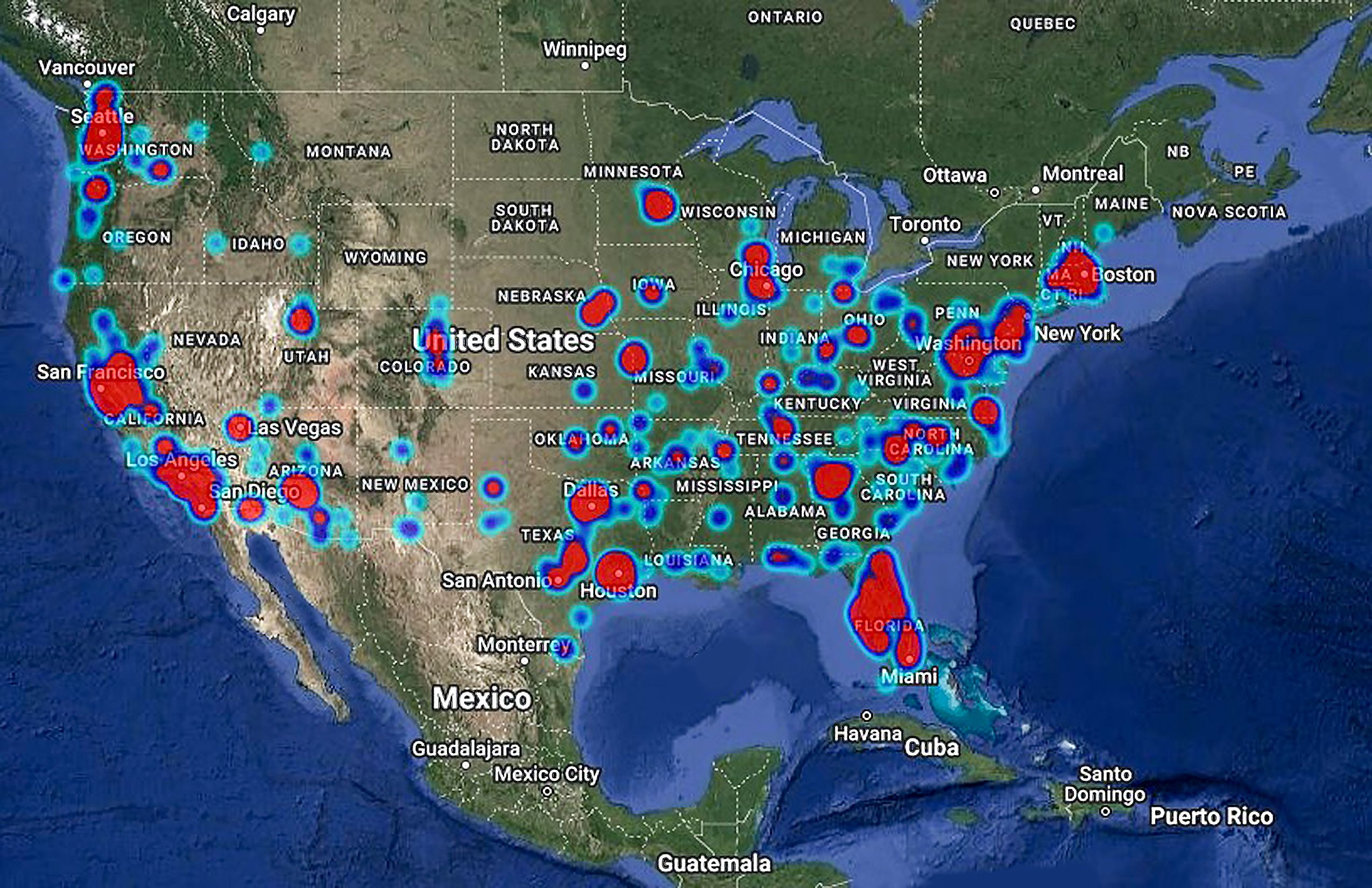

This heat map highlights where Loan Factory conducts business, with central hot spots in California, Texas, and Florida, aligning with areas of significant Vietnamese immigrant populations. Source: Loan Factory, Inc.

This heat map highlights where Loan Factory conducts business, with central hot spots in California, Texas, and Florida, aligning with areas of significant Vietnamese immigrant populations. Source: Loan Factory, Inc.

When hiring loan officers, Loan Factory CEO Nguyen said that he did not care to recruit top-performers in the industry or those with any mortgage experience. Although that allowed Nguyen to scale his company quickly, it has yet to translate to a significant increase in production.

Loan Factory produced 3,860 loans throughout 2024, according to Modex data. Among 1,500 loan officers, that would mean each loan officer produces, on average, two or three loans per year. The top five loan officers also made up about 38% of overall company production in 2024 with a combined 1,490 loans, while a third of the company’s loan officers have not produced any loans.

Then again, nearly half the company was hired less than 12 months ago.

Nguyen explains that production among his loan officers will lag as Loan Factory continues to rapidly scale. “Major change had to take place slowly,” he said. In August 2024, Nguyen reported that he was still originating loans in six states where he’s individually licensed to originate, but most of his loan officers are not. Nguyen serves those borrowers himself, saying, “It's hard to let them go.”

However, MMI data shows CEO Nguyen is still Loan Factory’s top originator with over 800 closed loans in 2024 — more than five times the number of loans that the company’s number one loan officer, Suong Nguyen, originated.

Name

14 MO $ VOL

TRANS 14 MONTH

PURCHASES %

REFI %

OTHER %

Thuan Nguyen

297,411,176

805

73.07

18.45

8.48

Suong Nguyen

39,084,561

155

74.67

14.67

10.67

Anh Nguyen

51,995,813

116

80.00

16.52

3.48

Keshav Sharma

63,248,977

113

79.65

5.31

15.04

Tien Dang

52,132,656

102

75.73

19.42

4.85

Loan Factory’s top producing loan officers in 2024, per MMI, according to the number of loans each MLO closed annually.

The faster that Loan Factory grows, the more origination work gets added to Nguyen’s plate. But, that’s where MOSO – Loan Factory’s cloud-based mortgage software – is meant to come in. “We make the loan officer’s job easy,” Nguyen said. “We use technology to cut their labor in half.”

Nguyen says that MOSO automates half of the originator’s job, which should allow them to focus more on bringing in clients. Rather than try to recruit top-notch originators, Nguyen looks for social butterflies or those who are deeply embedded in their community to capture leads.

Meanwhile, MOSO is made to reduce and expedite other clerical work that originators must get done. “We have a process so the consumer will do most of the work,” Nguyen continues. “That means the loan officers do very little and the technology helps them reduce it.”

Over the years, Loan Factory’s loan officers have contributed their ideas for updates and customizations. Suong, in particular, said she played a small hand in crafting MOSO to meet the needs of loan officers and their clients.

“Whenever we have an idea to add more to the system and customize the system, Thuan will help us to put it on,” Suong said. “I often raise my ideas with him, and he adapts with the market trends a lot.”

MOSO’s best feature, according to Suong, is the automatic interest rate update that’s sent via text or email to borrowers, allowing them to lock in a mortgage rate with the click of a button.

“Not many software can [send] automatic emails to update clients with the interest rate whenever it changes,” Suong said.

“They have to work at night. So there's a lot of logistics ... and with mortgages, nothing can stop for a second. Everything has to keep moving.”

Loan Processors & Diversification

“We also try to diversify our loan processors of different languages. So that's why we try to serve every community. No matter what language they speak, we try to have someone to help compliance,” CEO Nguyen said.

Certain states permit lenders to internationally outsource loan processors, allowing Loan Factory’s loan officers to receive additional backup from their loan processors based in Vietnam, Columbia, and the Philippines. Whenever U.S.-based loan officers are too busy or do not speak the borrower’s native language, these international loan processors can easily assist.

As a Vietnamese immigrant, Anne is capable of speaking to her clients in their native language; but when it comes to fixing an underwriting issue, the client may speak with the loan processor or loan officer. “I’m always very hands on with my file,” Anne said. “But it’s an advantage to have somebody beside me who can reach out and speak to clients in the language that they understand.”

Given Loan Factory’s success reaching the Vietnamese community, CEO Nguyen sees no reason why he can’t take the rest of the industry’s underserved markets as well. Nguyen is strategically scaling his company in a way that helps diversify his borrower base. Knowing that minorities and immigrant groups are drawn to people from their community, Nguyen is hiring loan processors from diverse backgrounds, like “the Philippines and Colombia,” he said. They can speak other languages and thereby attract diverse borrowers.

“They have to work at night. So there's a lot of logistics,” Nguyen said. “And with mortgages, nothing can stop for a second. Everything has to keep moving.”

Although Suong says she communicates with clients herself, while her processors handle the paperwork, like sending out email updates on the loan status, asking for documents, and sending out emails to title and appraisal companies. Still, she compliments Loan Factory’s Vietnam-based processors, saying they are “always available” and “very hardworking.”

As Loan Factory gears up to sweep even more borrowers that the industry has been neglecting, who is going to stop them? When asked who they consider to be top competitors in the Texas or Vietnamese market, the company’s top producers essentially responded with, ‘What competitors?’

Anne explains that, “We have other brokers that are Vietnamese speaking [in Texas],” but she doesn’t see them threatening Loan Factory dominance of the local market. “I don't think they’re specifically going after the Vietnamese immigrants.”

As Thuan Nguyen continues to recruit loan officers and loan processors from various backgrounds, he sets his sights on other underserved markets across the country.

“Of course, I want to help everyone become a homeowner,” Nguyen said. “But, if you are Vietnamese, Chinese, Indian — no matter who you are — you should always try to serve your community.”

ndustry’s biggest bottleneck is not underwriting itself — it is the uncertainty that reaches underwriting too late in the process. When validation happens upstream, speed follows naturally.

The long tail of loss mitigation is now coming into view as FHA’s post-pandemic relief tools give way to repeat defaults, exhausted options, and a swelling foreclosure pipeline