For the first time in three years, home purchase loans are considered just as risky as refinance loans, according to the third quarter (Q3) 2024 results of the Milliman Mortgage Default Index (MMDI). Global consulting and actuarial firm, Milliman Inc., reveals the latest monthly estimate of the lifetime serious delinquency (180 days or more delinquent) rates of U.S.-backed mortgages.

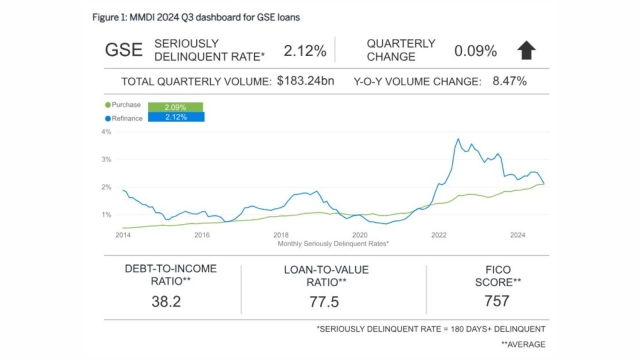

Mortgage delinquency risk increased to 2.12% for loans acquired in Q3 from 2.03% in the previous quarter, primarily due to the anticipated slowing of home price appreciation. For GSE loans, economic risk increased quarter-over-quarter, from 0.57% in Q2 to 0.67% in Q3.

The MMDI is broken down into three components that include borrower risk, underwriting risk, and economic risk. Borrower risk measures the risk of the loan becoming severely delinquent due to borrower credit quality, initial equity position, and debt-to-income (DTI) ratio. Underwriting risk is due to mortgage product features such as amortization type, occupancy status, and other factors. Economic risk is driven by historical and forecasted economic conditions.

The recent change in index value was driven by economic risk, according to Milliman’s analysis.

“For the first time in nearly three years, default risk on refinance loans is equal to or less than the default risk for purchase loans,” said Jonathan Glowacki, a principal at Milliman and co-author of the MMDI. “With the volume of rate/term refinance loans, which carry relatively lower risk, and cash-out refinance loans, which carry higher risk, equaling each other, the average default risk for these loans matched that of purchase loan originations.”

However, borrower risk for the quarter showed minimal change, moving down slightly from 1.47% to 1.46%, with less-risky purchase loans continuing to make up the bulk of originations at about 82% of overall loan volume.

Underwriting risk remains low and is negative for purchase mortgages. The volume of rate/term and cash-out refinance loans was about $16 billion each in Q3 2024, totaling $32 billion for refinance loans. Because the volume for each was similar this quarter, the weighted-average default risk for refinance loans was similar to the default risk for purchase loans.

Q3 2024 marked the first quarter since October 2021 when the default risk on refinance mortgages was equal to or less than the default risk on purchase mortgages.

The MMDI reflects a baseline forecast of future home prices. Quarter-over-quarter changes in the MMDI include restated Q2 2024 values since the previous publication.