Mortgage originations are expected to continue expanding through 2026, driven by improving affordability, easing mortgage rates, and sustained consumer demand, according to TransUnion’s latest credit industry forecast.

TransUnion projects purchase mortgage originations will increase 4.0% in 2026, while refinance activity is expected to rise 4.2%, extending a rebound that began after originations fell to near-record lows earlier in the decade. These gains reflect gradual normalization in housing finance conditions, as borrowers respond to more favorable rate environments and improved housing inventory.

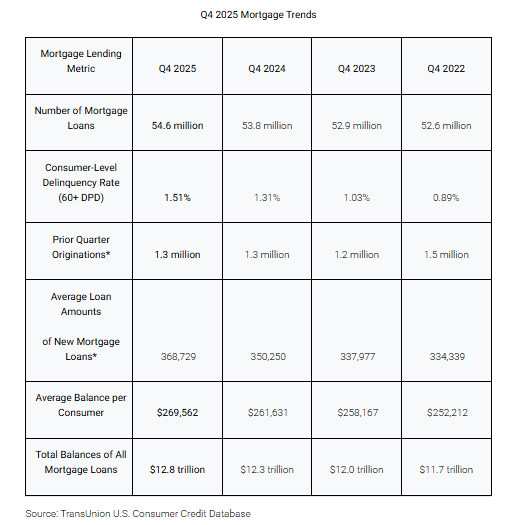

Recent performance data reinforces that upward trajectory, as mortgage originations rose 6.5% year-over-year in the third quarter of 2025, fueled by stronger purchase demand and a 25.7% increase in rate-and-term refinances, which marked the eighth consecutive quarter of refinance growth. Purchase loans accounted for approximately 80% of total originations, underscoring the continued dominance of purchase activity, even as refinance volume recovers.

“As we move through 2026, easing 30‑year mortgage rates should improve affordability for both buyers and refinancers,” said Satyan Merchant, senior vice president, automotive and mortgage business leader at TransUnion. “Homeowners are also tapping accumulated equity, with home‑equity originations posting a sixth straight quarter of growth. We’re seeing further signs of normalization as inventory reaches its most balanced levels in nearly a decade. We’re encouraged by the momentum created by falling rates, increased supply, and strong equity positions. Overall, the outlook remains positive as long as stakeholders stay focused and responsive.”

Rates Remain Key Variable Influencing Future Volume

TransUnion noted that easing rates should improve affordability for both buyers and refinancers, while increased housing supply and elevated homeowner equity positions are helping support transaction activity and lending demand.

In parallel, home-equity lending continues to expand, with originations rising 14.3% year-over-year in Q3 of 2025, as borrowers increasingly tap accumulated equity.

For mortgage originators, the outlook points to continued, but measured, growth. While overall lending expansion is expected to moderate compared with stronger gains in 2025, mortgages are projected to remain one of the primary drivers of credit growth alongside unsecured personal loans.

However, credit conditions are evolving, as mortgage delinquencies edged up to 1.51% in late 2025, highlighting the importance of disciplined underwriting and risk assessment as portfolios expand.

“After several years marked by credit behaviors influenced by stubbornly high inflation and elevated interest rates, we may be seeing signs of a return to more traditional growth,” said Michele Raneri, vice president and head of U.S. research and consulting at TransUnion. “As these more typical patterns return, it’s more important than ever for lenders to leverage advanced tools, including trended data, to more accurately assess evolving risk profiles.”