Manufactured housing has long been considered an affordable alternative to site-built homes. But financing these factory-made homes has become a major roadblock for people who want to buy them, a new report notes.

The Urban Institute, a non-partisan think tank, says financing for manufactured homes continues to be a challenge because loans are denied more often and come with higher rates than mortgage for so-called “stick built” houses.

Citing loan data from the 2024 Home Mortgage Disclosure Act, the report’s authors, Daniel Pang and Sarah Gerecke, write that applications to finance factory houses are denied at a rate of nearly 60%, compared to just 10% for conventionally-built houses.

At the same time, they add, buyers who want to finance their manufactured houses as personal property – as most still do – are rejected about two-thirds of the time. Pang is a policy analyst in the Urban Institute’s Housing Finance Policy Center; Gerecke, a non-resident fellow and a principal at SSG Community Solutions.

Besides being turned down far more often for financing, buyers who do pass muster often pay a lot more for their loans, the authors also found.

“The loan terms for those who do obtain financing are often worse for MH borrowers and worsen affordability challenges,” they say.

Last year, according to their report, the median interest rate stood at 7.88% for mortgages on manufactured houses and 9.5% when the houses are financed as personal property. By comparison, the median rate on stick-built houses was 6.63%.

The lack of affordable financing is just one of four considerations policy makers need to take into account in creating more effective solutions to the “dual housing and affordability crises,” Pang and Gerecke maintain.

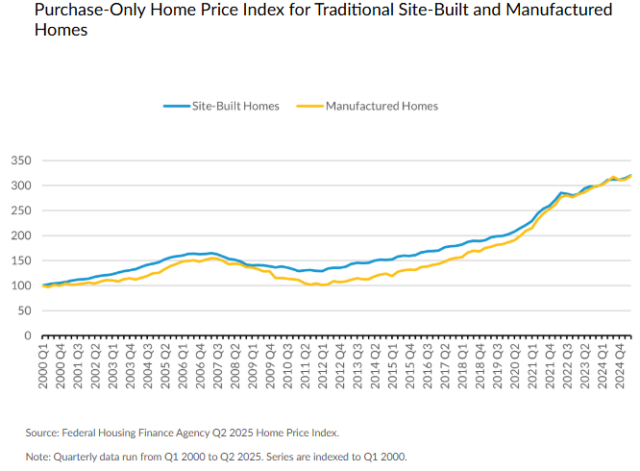

They also point out that factory-made houses appreciate at similar rates as conventional places, a fact that stands in stark contrast to the popular misconception that manufactured houses, like automobiles, depreciate as soon as they roll out of dealers’ showrooms.

“This negative perception has led some local governments to restrict manufactured housing in their communities, and have made some potential homeowners less likely to purchase manufactured homes,” they say.

In addition, the Urban Institute report calls for more standardization when it comes to defining manufactured housing and “what it encompasses.”

For example, the Census Bureau still labels factory houses as “mobile homes or trailers despite the outmoded terminology,” even though the 1980 Housing Act mandated that the term “manufactured” be used in place of “mobile” in all federal laws and literature.

This is important, the authors write, because “mobile home” often still carry the stigma surrounding quality, “as homes built in 1976 or earlier often resembled campers or trailers that could be easily moved if needed.”

Pang and Gerecke suggest policymakers look at more comprehensive data than what the federal government collects. For instance, they point out Pew Research Center’s 2022 Manufactured Housing Survey, a dataset that captured new information not typically found in publicly available data sets, including information on the titling conversion process, payment delinquencies, and living conditions.

And they say that other useful data that could contribute to policy discussions and decision-making “may include information on the homebuying process and dealer channel, loan performance and loss severity, and the ways zoning laws and regulations vary and align by locality.”