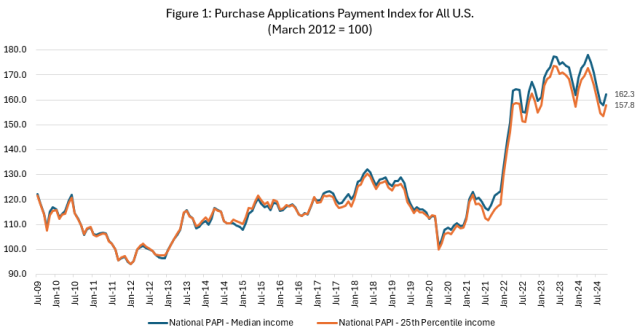

The 4.2% increase reflects a notable month-over-month increase in the MBA’s Purchase Applications Payment Index (PAPI), which tracks new monthly mortgage payments relative to income and reached its highest level since July last month.

On account of these affordability thresholds, rejections for mortgage refinance applications hit 22% in Oct. 2024, compared to 9.5% last October, show recent figures published by the Federal Reserve Bank of New York. Meanwhile, rejections for overall mortgage applications rose to 22.6% in Oct. 2024, up from 13% in Oct. 2023.

Year-over-year earnings growth shows affordability improved on an annual basis, despite the market remaining highly unaffordable. Median application payments fell by $72 from from Oct. 2023, equal to a 3.3% decrease.

Get the NMP Daily

Essential stories, every weekday.

The MBA reported that median earnings rose 3.2% in October compared to one year ago, and while monthly payments decreased 3.3%, moderate earnings growth brought the PAPI down by 6.3% on an annual basis.

Affordability improved 6.3% on an annual basis, despite the market remaining highly unaffordable, on account of an increase in median earnings (Source: MBA).

For borrowers applying for lower-payment mortgages (the 25th percentile), the national mortgage payment increased to $1,431 in October from $1,369 in September.

Reflecting rate locks from July and August, existing-home sales dipped 1% in September, then rose in October for the first time in three years as some homebuyers rushed to secure mortgage rates at their lowest level since Feb. 2023.

Meanwhile, the MBA’s national mortgage payment to rent ratio (MPRR) decreased from 1.46 at the end of the second quarter of 2024 to 1.34 at the end of the third quarter, meaning mortgage payments for home purchases have decreased relative to rents.

For the most part, no one expects years-long affordability constraints trapping prospective homebuyers on the sidelines to abate anytime soon. Nationally, home prices rose 3.8% on an annual basis in October, and mortgage rate volatility will likely continue into 2026, if recent revisions to Fannie Mae’s 2025 market forecast offers any clear indication of what’s ahead.

Economists at the government-sponsored enterprise have slashed earlier projections of existing-home sales by 340,000, from 11% to 4% growth next year, and raised their year-end 2025 mortgage rate forecast to 6.3% from 5.6%.

In October, 38% of sidelined homebuyers said they were “very prepared” to purchase a home once mortgage rates dropped to a sweet spot of 5.5%.

“We expect weaker homebuyer affordability to remain a hurdle for prospective buyers in the final months of 2024,” said Edward Seiler, the MBA’s Associate Vice President for Housing Economics, commenting on today’s report.

States with the highest PAPI, indicating those states with the highest levels of unaffordability, were: Idaho (241.9), Nevada (241.6), Arizona (217.2), Utah (205.1), and Rhode Island (205.0). States with the lowest PAPI were: Louisiana (114.8), Connecticut (115.1), Alaska (119.1), Vermont (119.6), and West Virginia (123.0).

With the outcome of November’s U.S. presidential election decided, a small increase in early-stage homebuying activity has emerged, coupled with two consecutive weeks of slightly higher purchase application volume.

The Builders’ Purchase Application Payment Index (BPAPI) showed that the median mortgage payment for purchase mortgages from MBA’s Builder Application Survey increased to $2,470 in October from $2,333 in September.

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro