Purchase locks sank 16% year over year, despite August being the most affordable month for home buying since February.

Refinance originations more than doubled on a monthly basis to account for 26% of total mortgage loan production in August, according to the latest Optimal Blue Market Advantage Mortgage Data Report. This is the result of mortgage rates falling to their lowest levels in months, providing payment relief to borrowers who have purchased homes at high rates since mid-2022.

Meanwhile, purchase-lock volume sank 16% year over year, despite August being the most affordable month for home buying since February, and for-sale inventory improving steadily over the summer. Total housing inventory was roughly 35% higher in August on an annual basis, per data from the Federal Reserve Bank of St. Louis.

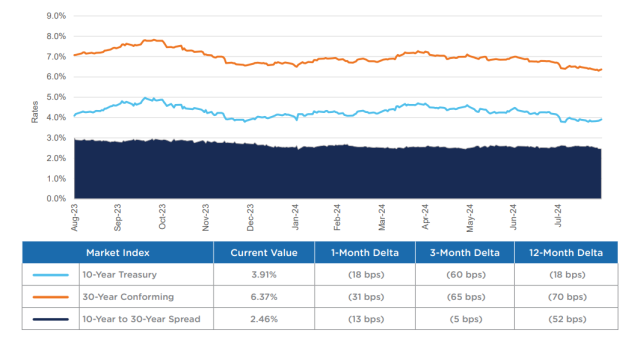

Optimal Blue Mortgage Market Indices showed the benchmark 30-year conforming rate ended August at 6.37%, down 31 basis points from July. Rates for FHA-backed mortgages receded even further, dropping 40 basis points to end the month at 6.13%.

Optimal Blue data indicate a narrowing spread between the 10-Year Treasury and the 30-year conforming mortgage rate, which has fallen by over 50 bps from the same period last year, provides more incentive for refinances.

While affordability constraints and the prospect of further rate relief has kept purchase money on the sideline in July and August, the rise in refinance volume was not unanticipated. Lenders across the mortgage industry have been preparing for a wave of refinances since the conversation around interest rates switched from hiking to cutting.

As early as February 2024, United Wholesale Mortgage (UWM) was moving to boost its refinance business with pricing incentives, and last week the company announced the launch of Refi75, which provides partners 75 basis points on any note rate for conforming conventional, FHA, and USDA rate and term refinances, including FHA Streamlines and VA IRRRLs.

Get the NMP Daily

Essential stories, every weekday.

Digital lender Better.com recently announced it now offers the FHA streamline refinance, an attempt to court the more than 1.5 million homeowners who have a mortgage rate over 7% and qualify for the product, according to Better CEO Vishal Garg. Bearish on the Federal Reserve’s ability to achieve a soft landing, Garg expects rate-and-term and cash-out refinance volume to continue growing as Americans seek to capture monthly savings or draw cash from their homes.

Among the top-20 metropolitan statistical areas (MSAs) tracked by Optimal Blue in its monthly report, refinances comprised the largest share of August lock volume in:

Los Angeles-Long Beach-Anaheim, Calif. (+38%)

San Diego-Carlsbad, Calif. (+31%)

Riverside-San Bernardino-Ontario, Calif. (+29%)

Chicago-Naperville-Eglin, Ill.-Ind.-Wis. (+29%)

Considering total outstanding U.S. mortgage debt stood at roughly $12.5 trillion as of the end of the first quarter of 2024, analysts continue to calibrate the size of this refinance opportunity. Of course, the lower rates fall, the larger the pool of borrowers who can benefit from refinancing.

MBA Vice President and Deputy Chief Economist Joel Kan said the pickup in refinance activity “remains limited to a smaller segment of homeowners with higher rates” when commenting on a two-year high in mortgage credit availability largely driven by refinances.

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro