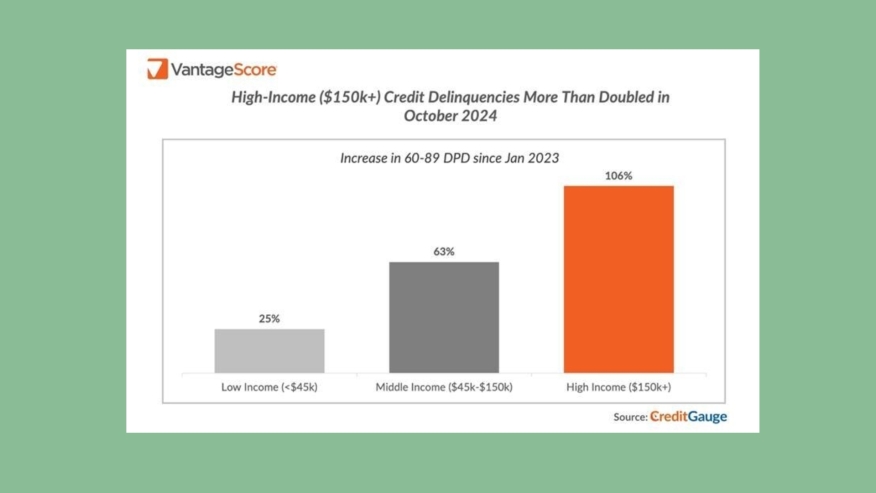

In what may signal impending strain for retailers ahead of the busiest shopping season of the year, credit delinquencies among borrowers earning $150,000 or more annually (“high-income earners”) more than doubled in Oct. 2024 as “pressure from inflation and a less healthy job market” weigh on the balanced budgets of America’s most liquid consumers.

Today’s release of VantageScore’s October 2024 CreditGauge survey, which examines monthly trends in the health of U.S. consumer credit, showed “[low]-income consumers are no longer the only group facing challenges,” said Susan Fahy, executive vice president and chief digital officer at VantageScore. “This economic reality will weigh on the holiday shopping season.”

In Oct. 2024, overall balances hit a new CreditGauge record for a fourth consecutive month, driven by mortgages. Average mortgage balances rose $6,813 (+2.6%) from last October, a result of higher interest rates and loan amounts due to elevated home prices.

Economic turbulence over the past two years have thrown the health of U.S. consumer spending into sharp focus. Consumer spending fuels the U.S. economy, and despite interest rate headwinds, strong spending throughout 2024 has alleviated some economists’ concerns about a downturn.

The health of the U.S. labor market overtook inflation as a primary concern for Federal Reserve policymakers in deciding to trim its benchmark borrowing rate by 25 basis points earlier this month, and 50 basis points in September.

Distorted by labor strikes and the fall-out from multiple natural disasters, October’s employment data clouded year-end forecasts as to the pace of future rate cuts. Markets have priced in a roughly 50% chance of an additional 25-basis-point cut in December.

The Federal Reserve Bank of New York released its quarterly Survey of Consumer Expectations (SCE) Credit Access Survey last week, painting a bleak picture of mortgage origination in 2024, as consumers’ expectations of improving credit conditions remain subdued ahead of 2025.

The Fed’s figures show mortgage application rejections hit decade highs in October, with the average rejection rate for mortgage refinance applications increasing to 25.6% this year, a jump from 15.5% last year. Rejections for overall mortgage applications rose to 22.6% in October, up from 13% in Oct. 2023 and 17.4% in Oct. 2022.

“White-collar consumers,” as VantageScore dubs high-income earners, have increasingly experienced rising credit delinquencies in the 60-89 days past due category, significantly outpacing delinquency growth among middle-income earners by 63%, and low-income earners by 25%, “underscoring that even high-income groups are feeling the effects of financial strain, compounded by the ongoing slump in white-collar employment,” the report reads.

According to its report, the average VantageScore 4.0 credit score held at 702 for the eighth consecutive month. Overall, the percentage of consumers with newly opened credit accounts dropped for the second month in a row, “and credit card balances remained flat compared to the month before.”