The U.S. Department of Housing and Urban Development (HUD) terminated Equity Prime Mortgage’s (EPM) Direct Endorsement (DE) authority — its ability to independently underwrite FHA-insured single-family loans — in New York, Jacksonville, Orlando, and Louisville, effective Aug. 22, 2025. Loans already approved before that date remain eligible for FHA endorsement, and EPM will continue to service existing FHA loans in those areas.

Announced Thursday, Sept. 11, in the Federal Register, HUD took the action under its Credit Watch Termination Initiative after determining that EPM’s default and claim rates on FHA loans endorsed in the prior 24 months exceeded 200% of the local average and were also above the national average.

The agency emphasized that DE termination applies only to the listed jurisdictions and is separate from any Mortgagee Review Board action. EPM can apply for reinstatement after six months with an independent CPA analysis of the affected offices’ operations and a corrective action plan, along with evidence the plan has been implemented.

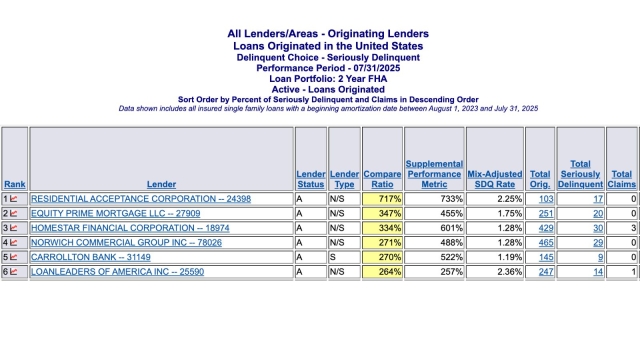

EPM Ranks #2 In Compare Ratio Nationwide

Data sourced from Neighborhood Watch, Friday, Sept. 12, 2025.

Key Takeaways

- EPM ranks #2 in Compare Ratio nationwide

- The HUD chart highlights EPM with a 347% Compare Ratio.

- This places the company second among originating lenders in the U.S. by that metric.

Compare Ratios Are A Blunt Instrument

However, Perez argues delinquency ratios are indicators, not outcomes. They may not reflect actual losses to the FHA insurance fund or EPM as he claimed families are still making payments and building stability.

In a press release sent to NMP, EPM points to potential causes such as skyrocketing property taxes and insurance premiums, rising 200–400% nationwide, have placed stress on households.

Additionally, the lender claims that rising delinquencies are a natural consequence of serving underserved communities, and notes that more than 90% of EPM’s borrowers come from minority, women, veteran, first-time buyer, or rural households. Expanding access potentially means taking on communities more exposed to inflation and cost-of-living shocks, EPM stated, which may inflates compare ratios.

EPM’s Corrective Actions

- Transitioned to new servicing partners.

- Updated overlays on gift funds and DTI.

- Retired one DPA program, launched a stronger replacement.

- Brought in Frank Razi, former HUD leader, as Chief Credit Officer.

How It Was Reported

HousingWire first reported the action Thursday, Sept. 11, with the headline "HUD terminates Equity Prime Mortgage’s FHA lending approvals," though the article states that HUD revoked EPM’s FHA loan approval authority in several regions due to elevated defaults and claims, and that pre-Aug. 22 approvals are unaffected.

The article also notes that an EPM spokesperson had no comment at the time.

How EPM Responded

EPM says the move is narrow in scope and took issue with HousingWire’s presentation of the story. “This isn’t about bad credit or poor underwriting,” claimed Eddy Perez Jr., CEO of EPM. “This was a narrow and specific action, not the sensational headline HousingWire ran with. Their approach is designed for clicks, not for truth. And when the press misleads, it doesn’t just hurt companies, it hurts the very families who rely on accurate information about access to homeownership.”

EPM argues delinquency ratios are indicators, not outcomes, pointing to property-tax spikes, insurance premiums rising 200% to 400%, and inflation as drivers of borrower stress. The company says these metrics can penalize lenders serving first-time buyers, minorities, women, veterans, and rural families.

“We respect the role of accountability, but we also know numbers alone can’t tell the story,” said Philip Mancuso, President and Partner at EPM. “Statistics don’t capture the resilience of families fighting to stay in their homes. That is what matters, and that is what we stand behind…It’s easy to lend money to people who don’t need it…”

EPM says it has changed servicing partners, added overlays and guideline adjustments (including for gift funds and DTI), retired and rebuilt its first down-payment assistance program, terminated certain broker relationships, and appointed Frank Razi as Chief Credit Officer to oversee credit policy and performance.

The company also alleged a broader pattern of sensationalism by HousingWire in past coverage. “In a time when truth is what this country needs more than ever, they chose headlines over facts," Perez claimed.

Perez Claims 'No Real Loss'

In an interview with NMP, Perez argued that HUD’s performance ratios can overstate risk because they capture late payments that never become losses. “The great thing I can say is, we’ve had very little claims compared to how many loans we’ve done,” he said. “So yes, some of the people have run late… However, if they never get foreclosed, there’s never a claim, there’s no real loss.”

Perez said macroeconomic pressures and product mix contributed to pockets of weaker performance. “Unfortunately, [down payment assistance loans] default more. Unfortunately, gift funds as well with a DTI above 48,” he said, adding that “the explosion of taxes and insurance” can push borrowers’ debt-to-income higher post-closing.”

Perez also cited pandemic-era relief habits and disaster forbearance as drivers of temporary delinquencies: “Now people just say, I’ll go down and wrap it up in the back because my friend did it… there’s actual people out there coaching them how to do it,” he claimed.

While HUD did not quantify EPM’s performance metrics in the notice, Perez said the company’s actual claims have been minimal relative to volume. “Our claims are very, very low, even though we did in the two-year period like 18,000 [to] 19,000 loans,” he said.

Yet, Perez described the operational impact of the suspension as limited. “It was only about 20 or 30 loans that we were doing in those states for FHA,” he said, noting EPM does “somewhere between 1,500 or more loans a month” across products. He added that EPM is working with partners “to deliver us more FHA business to really grow the denominator” and has “terminated four to five hundred broker relationships” that did not meet its standards.

What Originators Should Know

- EPM is still an FHA-approved lender outside the four affected jurisdictions. In New York, Jacksonville, Orlando, and Louisville, EPM cannot underwrite FHA loans on its own; another FHA-approved DE lender would need to perform underwriting for new cases.

- Borrowers with EPM loans already approved before Aug. 22 are not affected by the DE termination for endorsement purposes.

- Next steps hinge on EPM’s ability to document improvements and secure reinstatement after at least six months under HUD’s prescribed process.