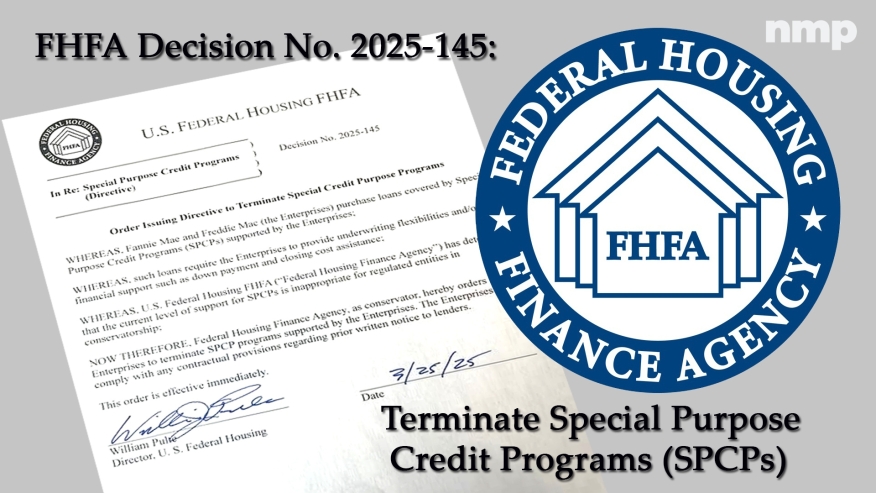

In a directive issued March 25, Decision No. 2025-145, Federal Housing Finance Agency (FHFA) Director Bill Pulte ordered Fannie Mae and Freddie Mac to terminate “Special Purpose Credit Programs,” or SPCPs, that they support.

The directive describes such programs as those that provide particular borrowers who lack adequate down payments for homes or the ability to cover mortgage closing costs assistance.

Specifically, Director Pulte spells out in his directive that:

- Fannie Mae and Freddie Mac purchase home loans covered by SPCPs,

- Those programs require the GSEs to provide underwriting flexibility and financial support such as down payment and closing cost assistance,

- The GSEs’ current support for SPCPs “is inappropriate for regulated entities in conservatorship,” FHFA believes, and therefore

- Fannie Mae and Freddie Mac must terminate the SPCPs they support, though they still “may comply with any contractual provisions regarding prior written notice to lenders.”

What Is And What Is Not Affected

According to its wording and rationale, this FHFA directive will apply to programs specifically designated as Special Purpose Credit Programs supported by Freddie Mac and Fannie Mae. A few examples of SPCPs include:

United Wholesale Mortgage has an SPCP that provides $5,000 toward homebuyers’ down payment/ closing costs and up to $1,000 toward home warranty/ appraisal costs.

Bank of America has an SPCP called the "Community Affordable Loan Solution" for first-time homebuyers that offers zero down-payment and zero closing-cost mortgages.

Guaranteed Rate offers an SPCP that provides up to $8,000 in assistance to help borrowers overcome accessibility challenges such as deposit minimums and move-in repair and maintenance costs.

Wells Fargo has what it has specifically termed a “Special Purpose Credit Program” designed to help minority homeowners who have a mortgage with the bank refinance their mortgages at a lower interest rate.

Since this FHFA directive was issued yesterday, there's been some fervent speculation among mortgage loan originators that it would dismantle Freddie Mac's Home Possible mortgage program, which offers low-income borrowers down payment assistance, and/or Fannie Mae’s HomeReady mortgage program, which lowers down-payment and credit score requirements for qualifying borrowers.

Those two GSE programs are distanced from SPCPs, and this March 25 FHFA directive does not appear to affect them. Both HomeReady and Home Possible are specifically referenced as Equitable Housing Finance Plans, or EHFPs.