Median purchase application payments rose 3.5% from the end of 2023 — the last 'worst year in decades' for home sales

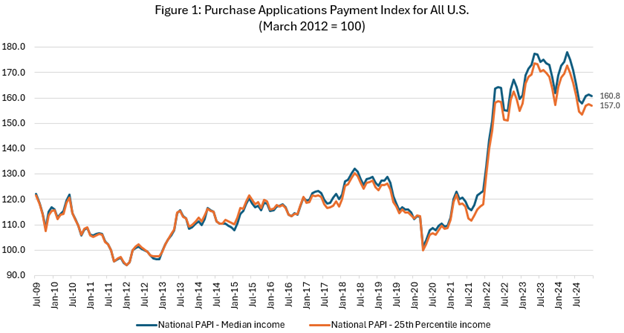

Homebuyer affordability remained flat in December as the national median mortgage payment applied for by purchase applicants declined just $6 to $2,127 — the same level they were at in October — from $2,133 in November.

That payment is $72 higher than a year earlier, however, marking a 3.5% annual increase, per the latest figures from the Mortgage Bankers Association (MBA), which tracks changes in borrowers’ payment-to-income ratios through its Purchase Applications Payment Index (PAPI).

At $1,866 last month, the national median mortgage payment for FHA loan applicants was $32 less than November's (-1.68%), but $44 higher than a year ago (+2.4%). The national median mortgage payment for conventional loan applicants was $2,128, down $5 from November (-0.23%), but up $75 from a year ago (+3.65%).

An increase in MBA’s PAPI indicates declining borrower affordability conditions, meaning that the mortgage payment to income ratio (PIR) is higher due to increasing application loan amounts, rising mortgage rates, or a decrease in earnings.

The nominal month-over-month change in December was “the result of somewhat volatile mortgage rate movements and moderating home-price growth,” said Edward Seiler, MBA’s Associate Vice President, Housing Economics, and Executive Director, Research Institute for Housing America.

Source: Mortgage Bankers Association

Typical mortgage payments, including property taxes and skyrocketing insurance costs, continue to eat up larger portions of monthly incomes, making it difficult for younger, first-time homebuyers to access the market, particularly given the lack of affordable, entry-level homes.

The MBA reports that median earnings rose 4.1% compared to one year ago, and while payments increased 3.5%, the significant earnings growth means that the PAPI is down 0.6 % on an annual basis. For borrowers applying for lower-payment mortgages (the 25th percentile), the national mortgage payment increased to $1,446 in December from $1,436 in November.

Seiler calls 2024 "a sluggish year for home sales" due to the nation's widespread affordability challenges. He adds “[The] MBA expects 2025 conditions will improve as housing supply increases, giving prospective buyers more options and putting less pressure on their budgets.”

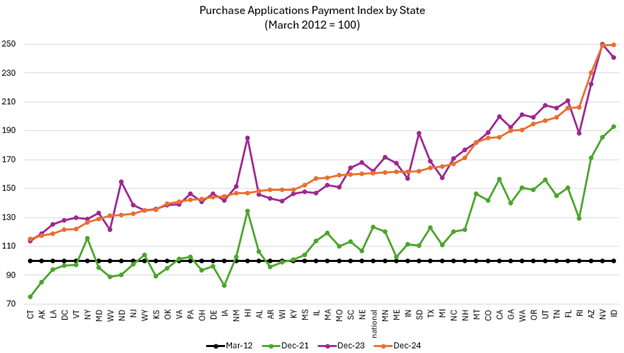

The top five states with the highest PAPI — the worst housing affordability from the perspective of payment-to-income ratios — were: Idaho (249.5), Nevada (249.0), Arizona (230.3), Rhode Island (206.3), and Florida (205.8).

Source: Mortgage Bankers Association

The top five states with the lowest PAPI — the best housing affordability from the perspective of payment-to-income ratios — were: Connecticut (115.2), Alaska (117.3), Louisiana (118.9), D.C (121.3), and Vermont (122.1).

The Builders’ Purchase Application Payment Index (BPAPI) showed that the median mortgage payment for purchase mortgages from MBA’s Builder Application Survey increased to $2,500 in December, up from $2,481 in November.

Seller/servicers using artificial intelligence in origination or servicing must have formal policies, oversight, and vendor controls in place

Fannie Mae’s artificial intelligence and machine-learning governance requirements take effect Thursday, Aug. 6, giving approved seller/servicers a final deadline to formalize how the technology is used across mortgage origination and servicing.The requirements apply when a s...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Higher mortgage rates are thinning the purchase pipeline, even as lower asking prices and reduced competition give borrowers still in the market more leverage.Seasonally adjusted U.S. pending home sales totaled 322,739 during the four weeks ending July 26, their lowest level...

Pending sales fell to their lowest level since early April, but lower asking prices and reduced competition give originators more options to structure deals for qualified borrowers

Price cuts and longer listing times are creating opportunities for loan officers to help borrowers negotiate seller concessions, but leverage varies sharply by metro